Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

OECD Sees Brighter Economic Prospects But An Uneven Recovery

Prospects for the world economy have brightened but the recovery is likely to remain uneven and, crucially, dependent on the effectiveness of public health measures and policy support, according to the OECD’s latest Economic Outlook.

In many advanced economies more and more people are being vaccinated, government stimulus is helping to boost demand and businesses are adapting better to the restrictions to stop the spread of the virus. But elsewhere, including in many emerging-market economies where access to vaccines as well as the scope for government support are limited, the economic recovery will be modest.

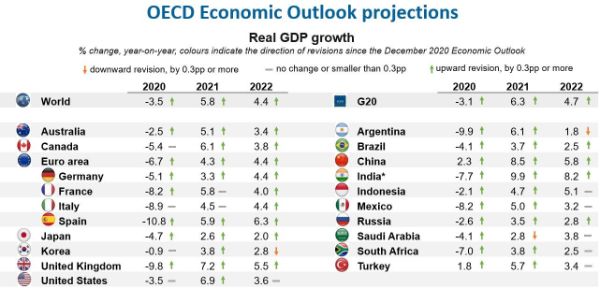

The OECD has revised up its growth projections across the world’s major economies since its last full Economic Outlook in December 2020. It now sees global GDP growth at 5.8 % this year (compared with 4.2% projected in December), helped by a government stimulus-led upturn in the United States, and at 4.4% in 2022 (3.7% in December). The world economy has now returned to pre-pandemic activity levels, but real global income will still be some USD 3 trillion less by the end of 2022 than it would have been without a crisis.

As long as a large proportion of the world’s population is not vaccinated and the risk of new outbreaks remains, the recovery will be uneven and remain vulnerable to fresh setbacks, the Outlook says. Some targeted restrictions on mobility and activity may still need to be maintained, particularly on crossborder travel. This will affect the prospects for a full recovery in all countries, even for those with a fast vaccine rollout or low infection rates.

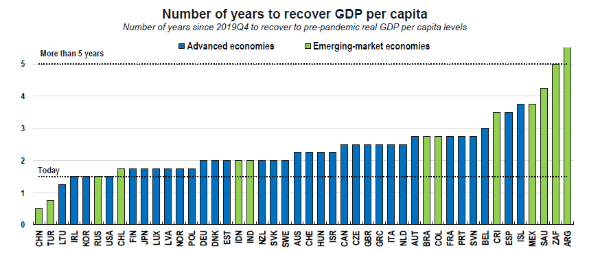

Driving the differences between countries are public health strategies, the speed of vaccine rollout, fiscal and monetary support, and the relative importance of hard hit sectors such as tourism. While Korea and the US are already back to their pre-pandemic income levels, much of Europe is expected to take an additional year for them to bounce back. In Mexico and South Africa, it could take three to five years.

Considerable uncertainty surrounds the projections, although risks have become more balanced between potential positive and negative impacts. In countries where vaccination is not widespread, the risk of further outbreaks remains very high, with the possible emergence of new vaccine-resistant variants of the virus. This could trigger further containment measures and delay the economic rebound.

On the upside, the high levels of household savings that have built up during the crisis could be unleashed as economies reopen, boosting consumption and growth to higher-than-expected levels, especially in advanced economies.

The release of pent-up demand in the advanced economies, together with disruptions to supply chains caused by COVID-19, could push up inflation and market interest rates, which in turn risks putting vulnerable emerging-market and developing countries under financial pressure. But, according to the Outlook, the jump in inflation will likely be temporary as the disruptions should start to fade by the end of the year, with production capacity normalising and consumption rebalancing from goods towards services. The OECD adds that with many people still out of work, a cycle of sharp wage rises and price increases is unlikely.

Presenting the Economic Outlook, OECD Secretary-General Angel Gurría said: “Effective vaccination programmes in many countries has meant today’s Economic Outlook is more promising than at any time since the start of this devastating pandemic. But for millions around the world getting a jab still remains a distant prospect. We urgently need to step up the production and equitable distribution of vaccines.”

OECD Chief Economist Laurence Boone said: “Our latest projections provide hope that in many countries, people hit hard by the pandemic may soon be able to return to work and start living a normal life again. But we are at a critical stage of the recovery. Vaccination production and distribution have to accelerate globally and be backed by effective public health strategies.”

“Stronger international cooperation is needed to provide low-income countries with the resources - medical and financial - required to vaccinate their populations. Trade in healthcare products must be allowed to flow free of restrictions.”

Ms Boone said income support for people and businesses should continue but evolve and adapt in line with the strength of the economy and the health situation. As containment measures are lifted, better targeting of support to where it is needed most - including through re-training and job placement - will improve prospects, particularly for the low skilled and for youth. Support also needs to focus on viable businesses, to encourage a move away from debt into equity, and to create jobs and invest in digitalisation.

Although government fiscal support throughout the pandemic has pushed up public debt in most economies, the Outlook says current low interest rates make debt servicing more manageable and should open the way for investments in areas such as healthcare, digitalisation and addressing climate change. Ms Boone “Debt sustainability should be a priority only once the recovery is well advanced, but governments should start planning for an overhaul of public finance management. This is no ordinary crisis and no ordinary recovery. Post crisis policies should be reformed in depth to address more effectively today’s challenges and those ahead.”

For the full report and more information, visit the Economic Outlook online.

World Vision: 3.5 Million Displaced Following Myanmar Earthquake And Ongoing Internal Conflict

World Vision: 3.5 Million Displaced Following Myanmar Earthquake And Ongoing Internal Conflict World Butchers Challenge: World’s Top Butchers From 14 Nations Go Knife-to-Knife In Paris

World Butchers Challenge: World’s Top Butchers From 14 Nations Go Knife-to-Knife In Paris Save The Children: ‘It Was Terrifying’ - Children Prepare To Spend Myanmar New Year Festival In Shelters Following Earthquake

Save The Children: ‘It Was Terrifying’ - Children Prepare To Spend Myanmar New Year Festival In Shelters Following Earthquake Global Forest Coalition: Global NGOs Call On International Maritime Org To Reject Biofuels And Commit To Truly Clean Energy

Global Forest Coalition: Global NGOs Call On International Maritime Org To Reject Biofuels And Commit To Truly Clean Energy Australian Catholic University: Principals Navigate Growing Challenges As Anxiety, Depression Increase And Violence, Workloads Intensify

Australian Catholic University: Principals Navigate Growing Challenges As Anxiety, Depression Increase And Violence, Workloads Intensify SNAP: Survivors Deliver Vos Estis Lux Mundi Complaints Against Six Cardinals To Vatican Secretary Of State Parolin

SNAP: Survivors Deliver Vos Estis Lux Mundi Complaints Against Six Cardinals To Vatican Secretary Of State Parolin