Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

On Mitsui sale of Tui stake to joint venture partners

Thoughts on Mitsui sale of Tui stake to joint venture partners

On 3 October 2013 – the sale of Mitsui’s 35% stake in the Tui Area Oil Project (Tui) was announced. The Tui joint-venture (JV) partners acquired this 35% stake for US$15 million (NZ$18 million). The JV partners are AWE Limited (ASX:AWE), New Zealand Oil & Gas (NZOG) (NZX:NZO) and Pan Pacific Petroleum (NZX:PPP). Clare Capital has no active or historic mandates with any of these companies. Clare Capital has built an independent financial model of NZOG (using publically available information) – so we are going to use NZOG as the illustration for this analysis. NZOG started with 12.5% of Tui and ended with 27.5%. NZOG paid US$6.4 million for this additional 15% stake and took on additional Oi exploration well development costs. Based on our analysis this transaction should have increased the NZOG share price by $0.11. Clare Capital places a $0.97 per share intrinsic value on NZOG prior to this transaction – and a $1.08 after the transaction.

While the Tui field is declining (production is forecast to end around 2020) – $15 million seems like a really cheap price for 35% of a producing field. At 30 June 2013, the NZOG annual report had their 12.5% stake of Tui reserves (2P) being 800,000 barrels of oil and condensate (meaning 6.4 million barrels left in the whole field). NZOG generated oil sales of NZ$30.4 million from this 12.5% stake in the FY2013. We figured the sale price meant one of two things:

1. That is a really cheap price and the JV

partners just picked up a bargain and their share prices

will rise; or

2. Something is really wrong with the

figures and if US$15 million is fair-value for 35% of the

Tui oilfield then we are about to see the JV partners share

prices fall.

But the NZOG share price hasn’t moved (NZ$0.80 on 3 October – and similar today). We are surprised…

We immediately thought that the price looks cheap. The 2P reserves number isn’t ‘made-up’ – it is based on independent geological assessments/frameworks and is how the financial markets assess oil and gas reserves. The NZX Listing Rules (Section 10.11) say: “do it this way”… Clare Capital strongly believes we can rely on the NZOG 2P reserves number – meaning Tui had 2P reserves of approximately 6.4 million barrels of oil left in the field at 30 June 2013. What does that mean for the transaction price?

Implications of Tui

Transaction Notes 30

June 2013 Tui 2P Reserves 6,400,000 Barrels

of Oil Equivalent Last three months

production (see note below) 417,000 Barrels

of Oil Equivalent Clare Capital estimate at

30 Sep 2013 Tui 2P

Reserves 5,983,000 Barrels of Oil

Equivalent Mitsui stake

(35%) 2,094,050 Barrels of Oil

Equivalent Transaction purchase

price US$15

million US$ Based on this

transaction the implied per barrel purchase

price US$7.16 Calculation Average

NZOG price per barrel for Tui

sales US$108.80 NZOG Annual

Report

Quick note: the last three months production is based on the 12 months production to 30 June 2013. Because the field is declining (NZOG production dropped from 2012 to 2013 by 24.4%) this is probably a conservative number (i.e. we are probably over-stating actual production – meaning more oil remains).

The transaction allows the JV partners to buy oil reserves at US$7.16 that are being currently sold at US$108.80. That looks a good deal to the buyers. But the share price hasn’t moved…

Now Mitsui is a very large multinational with a range of asset allocation decisions to make. They may have very good reasons for wanting to exit Tui – and a quick deal with the JV partners may have been attractive. We are also not privy to the contents of the JV agreement between the partners – which may have had pre-agreed exit provisions. There are a number of additional reasons that could drive the specific price from the Mitsui end – such as movements in currencies. Mitsui also exited the drilling costs for Oi exploration well – which also potentially distorts the headline transaction number. But ultimately, from the JV partners’ perspective, the price looks very cheap.

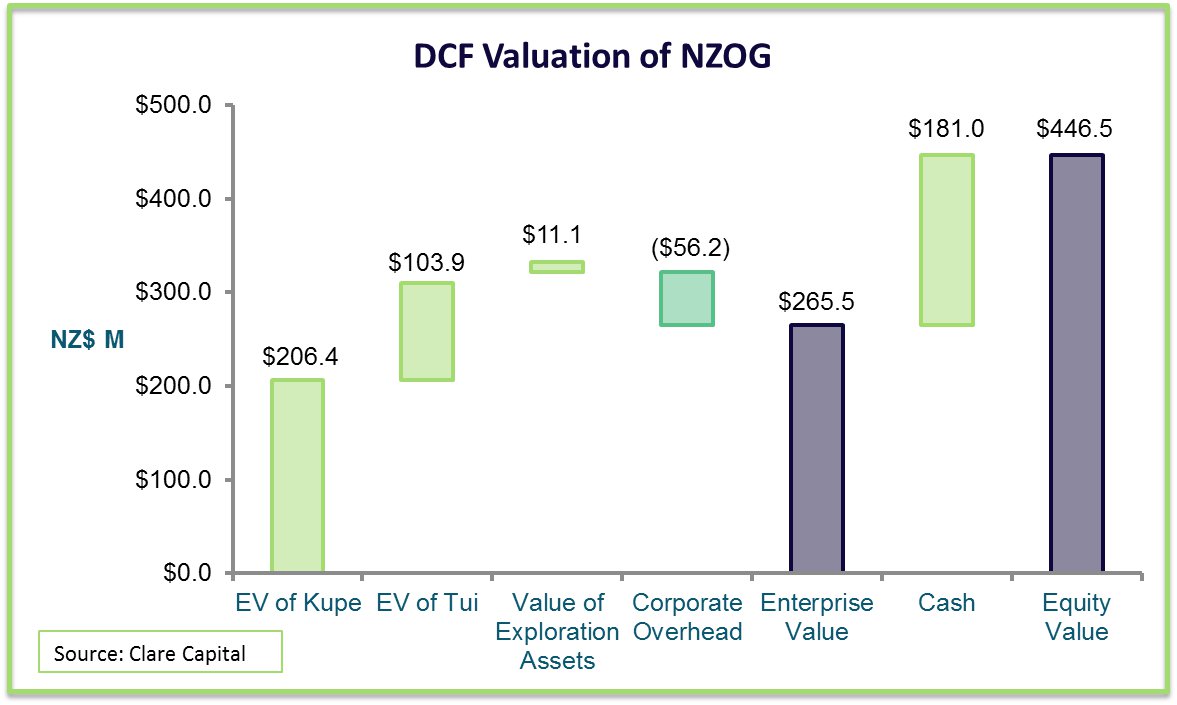

As noted, we have a financial model for NZOG – which includes valuations of the whole Tui and Kupe fields. Our valuation of the Tui field (100%) is NZ$378 million. Based on our model, Mitsui’s 35% stake is therefore worth NZ$132 million – which is a lot more than the US$15 million (NZ$18 million) transaction value.

Clare Capital valued NZOG at $0.97 per share prior to this transaction – well above the current $0.80 share price. Our valuation is broadly in-line with other analysts. In our $0.97 valuation – Tui represents $0.11 of that value. We believe that most analysts/investors are broadly valuing Tui in the same way.

DOWNSIDE SCENARIO: If Tui’s fair value is represented by the transaction – meaning 35% is ‘worth’ NZ$18 million (100% is ‘worth’ NZ$51.4 million); then 12.5% of Tui (NZOG’s stake prior to the transaction) is worth only NZ$6.4 million – or NZ$0.015 of the share price. NZOG’s share of Tui after the transaction would mean NZ$0.034 of the share price. This is well below our current $0.11 per share value of Tui to the NZOG share price. We don’t think this is the case – but it is worth noting.

UPSIDE SCENARIO: If the JV partners have just acquired increased stakes in Tui at a cheap price – which is our hypothesis – then we should have seen the JV partner’s share prices increase. In our model we have the value impact in the transaction for NZOG being a lift in the intrinsic value of the share price from $0.97 to $1.08. Based on our cash flow assumptions, to get to the current share price requires a 30% WACC. This seems unreasonable due to the contracted nature of NZOG’s key cash flows.

This transaction ‘should’ have meant a revision of the share prices of the JV partners – either up or down. We think it should have been up – but either way we should have seen something…

Interestingly, on the 4 October (one day after the transaction) there was a substantial shareholder notice (SSN) for Zeta Resources. Zeta Resources are the largest NZOG shareholder led by Duncan Saville and Dugald Morrison. In the SSN Zeta Resources announced that they had increased their stake in NZOG from 8.0% to 9.24%. But the share price has not moved…

CONCLUSION: Based on

this transaction, Clare Capital believes we should have seen

a lift in the NZOG share price (as well as the other JV

partners) – but we have not. So much for efficient

markets…

DISCLOSURE: No

Positions

Appendix 1: Clare Capital view of NZOG’s valuation (post-transaction)

Appendix 2:

Clare Capital oil and gas industry

valuations

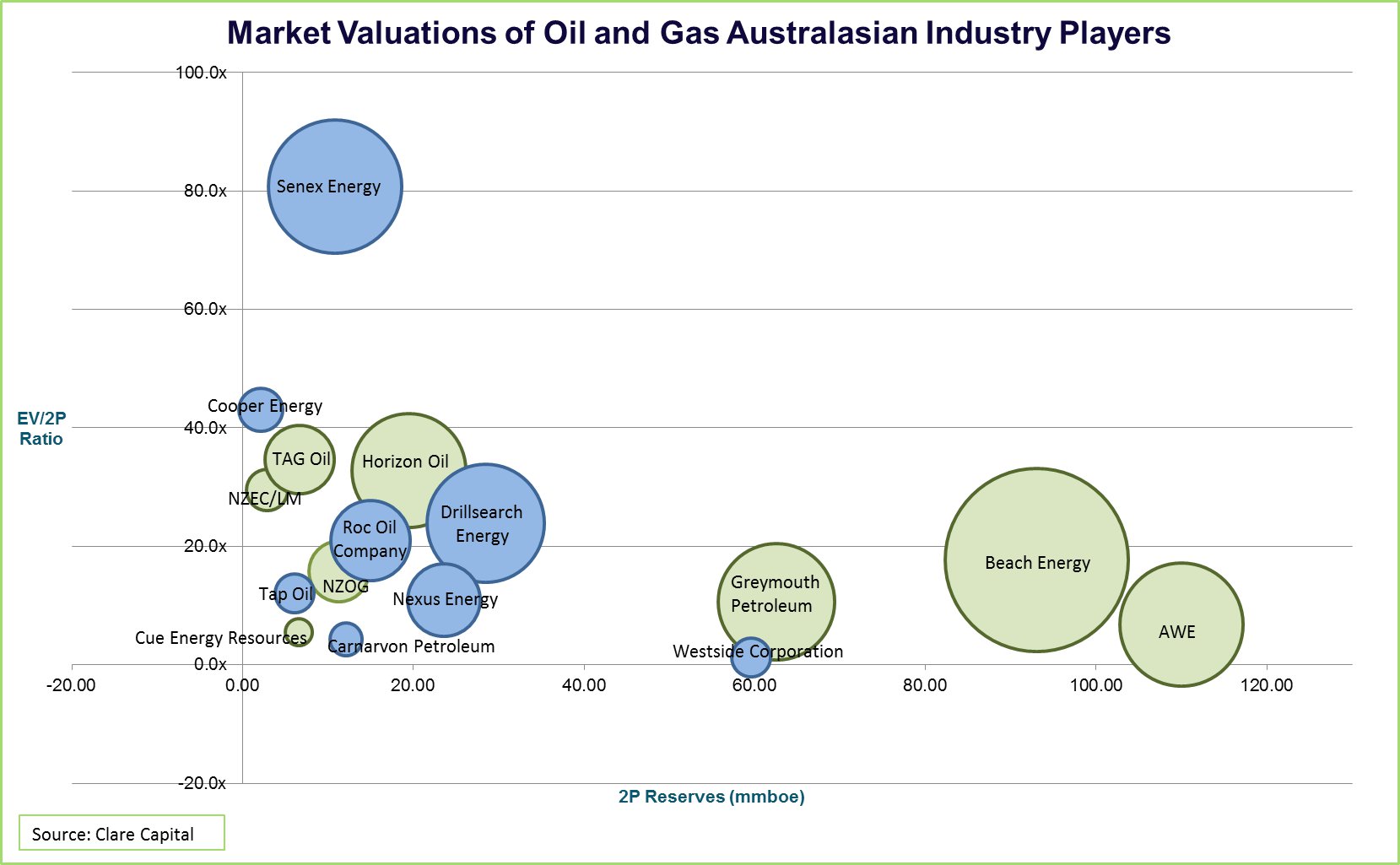

Clare Capital uses the Enterprise

Value/2P reserves ratio to give an indication of how the

market is valuing a number of New Zealand and Australian

comparators in the oil and gas exploration and production

industry (as at 9 October 2013). Companies with an EV less

than NZ$20 million are excluded (such as Pan Pacific

Petroleum). Note: we have used the valuation figure which

TAG Oil reportedly offered Greymouth Petroleum in 2012 as

Greymouth is a privately-held company. Also, mmboe is the

short hand notation for a million of barrels of oil

equivalent.

Company Enterprise Value (NZD

M) 2P reserves

(mmboe) EV/2P AWE 750.86

110.00 6.8x Beach

Energy 1,646.23

93.00 17.7x Cooper

Energy 92.98

2.16 43.0x Cue Energy

Resources 36.25

6.59 5.5x Carnarvon

Petroleum 51.88

12.10 4.3x Drillsearch

Energy 681.79

28.50 23.9x Horizon

Oil 639.82

19.50 32.8x Nexus

Energy 259.01

23.56 11.0x NZEC/LM

84.25

2.85 29.5x NZOG

177.73 11.26 15.8x Roc Oil

Company 314.11

15.00 20.9x Senex

Energy 872.41

10.80 80.8x TAG

Oil 231.97

6.70 34.6x Tap

Oil 73.81

6.10 12.1x WestSide

Corporation 74.50

59.60 1.3x Greymouth

Petroleum 663.06 62.51 10.6x

The following bubble diagram illustrates the EV/2P ratios of companies with operations in Australia and New Zealand. The 2P numbers are the latest available. The area of the circles indicates enterprise value, reserves are shown along the horizontal axis and the EV/2P ratio is on the vertical axis. Green colouration denotes companies with New Zealand operations, while blue colouration represents Australian only operations. The closer a company is to the horizontal axis, the ‘cheaper’ its market valuation.

Click for big version.

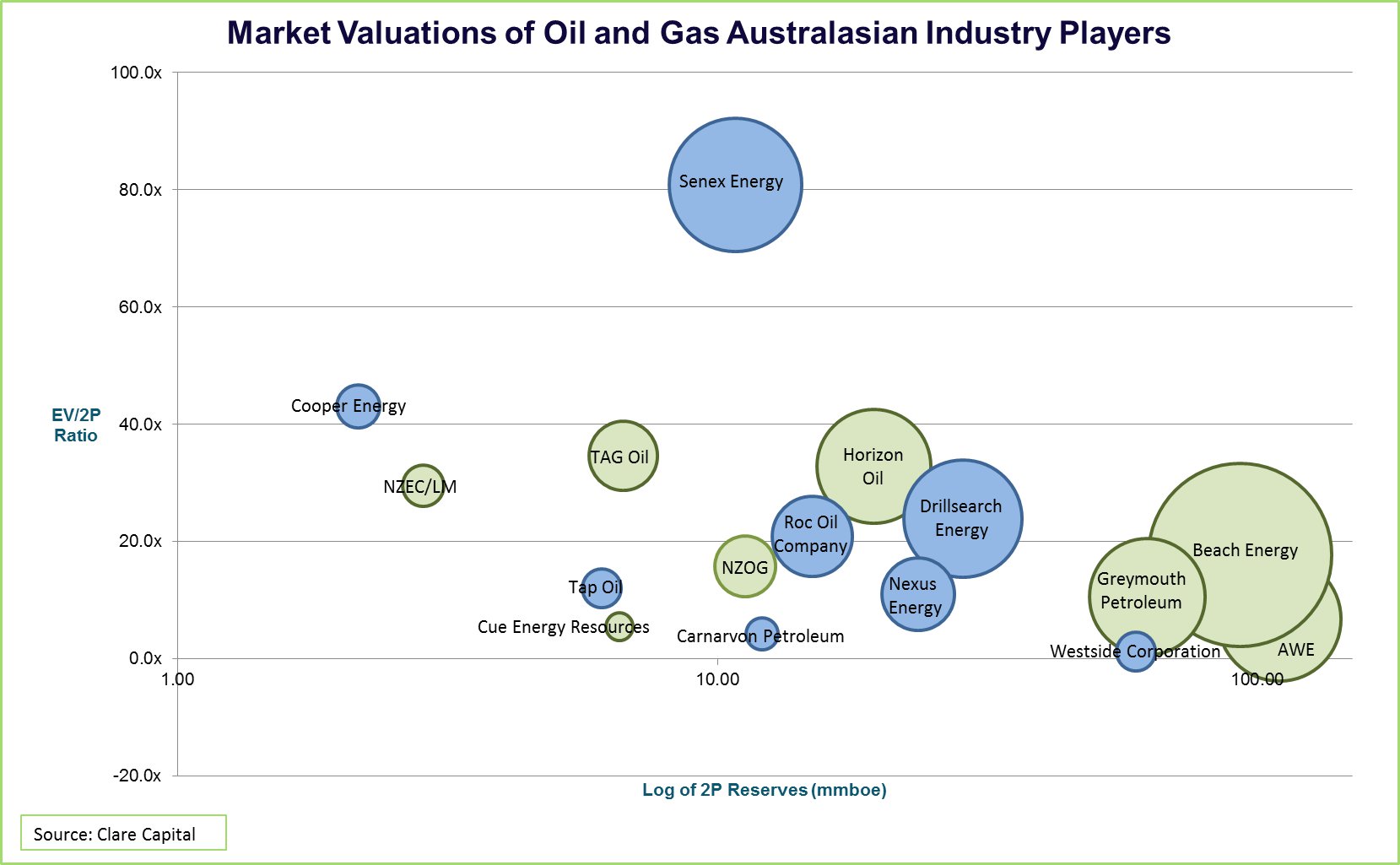

The same information presented utilising a log-scale of the 2P Reserves (mmboe) on the horizontal axis.

Click for big version.

ENDS

Gordon Campbell: On The Government’s Latest Ferries Scam

Gordon Campbell: On The Government’s Latest Ferries Scam Peter Dunne: Dunne's Weekly - While We're Breaking Up Monoliths, What About MBIE?

Peter Dunne: Dunne's Weekly - While We're Breaking Up Monoliths, What About MBIE? Adrian Maidment: Supermarket Signs

Adrian Maidment: Supermarket Signs Ian Powell: Revisiting Universalism

Ian Powell: Revisiting Universalism Martin LeFevre - Meditations: In A Global Society, There Is No Such Thing As “National Security”

Martin LeFevre - Meditations: In A Global Society, There Is No Such Thing As “National Security” Binoy Kampmark: Secrecy And Virtue Signalling - Another View Of Signalgate

Binoy Kampmark: Secrecy And Virtue Signalling - Another View Of Signalgate