Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Keith Rankin: The Global Debt Crisis

Global Debt Crisis

by Keith Rankin20 December 2011

The global debt crisis, presently centred on Europe, has world political and intellectual leaders baffled.

The problem is a shared mindset which treats economies (buying and selling goods and services) and finance (buying and selling assets that serve as claims on goods and services) as if they are essentially the same. This confusion combines with a set of ingrained beliefs that certain values - namely "work" and "thrift" - should represent the bedrock of our behaviour. The idea that economies might be relaxed rather than stressed does not compute, given this orthodox mindset.

These confusions allow us to believe that our economies can recover by, simultaneously increasing our non-spending (ie our saving) and increasing our spending. By definition, saving is non-spending; the acquisition of financial assets. Financial assets include money, bonds, debentures and company shares. We even go as far as calling the acquisition of financial assets (non-spending by definition) "investment", when in reality investment is spending (not non-spending) on such things as infrastructure, machinery, education, computer systems and inventories.

The problem can easily be understood if, when we hear or read the words "work" (as in paid work) and "save", we substitute the words "sell" and "lend". Because that's what these words really mean.

When we use the word "work" as we do, we mean either self-employment (selling goods or services) or employment (selling labour services to employers who sell goods and services). So the amount of "work" that takes place is constrained by the amount of buying that takes place. If we buy less (ie spend less, or non-spend more) then we sell less; we "work" less.

When we use the word "save" we in reality mean we lend to a bank or other financial institution, or lend directly to a company or a government by buying bonds, or we advance part of our income to a business in return for a share of its profits. ("Advance" has a meaning equivalent to "lend".)

When we use the correct words, it becomes clear that we are exhorted to, collectively, sell more and buy less; and to lend more and borrow less. Both exhortations are logically impossible to achieve, because, by definition, the amounts of goods and services we sell are exactly equal to the amounts that we buy. And the amounts that we lend are exactly equal to the amounts that we borrow.

In our general confusion over the difference between real wealth (goods and services) and financial wealth (financial assets), we square the circle by assuming that firms, taken collectively, run permanent deficits. That is, we assume that there is an inexhaustible desire by firms (and their bankers) to add to their debts – to indefinitely borrow and spend more than they repay – thereby allowing households to continuously accumulate their credits (credits is the "plus" side of debt, as in "total credits equal total debt") in the belief that businesses will do the necessary spending (buying goods and services) that enables everyone offering labour for sale to be employed.

This orthodox (though rarely stated) belief, that businesses represent a potentially unlimited source of spending ("demand" to economists) links to assumptions around the interest rate. In neoclassical economics, the interest rate represents the cost of business borrowing; the rate of interest is expected to rise or fall so that household net lending matches business net borrowing. It is assumed that, at an interest rate of zero, business demand for borrowed funds would be infinite. So it is assumed that, if businesses are not spending enough to buy all the surplus goods and services on offer, then the interest rate must be too high. Hence the policy emphasis on lowering interest rates.

We observe that these assumptions are untrue, not least through Japan's experience in the 1990s. But we continue to assume that these assumptions are true, presumably because they act like some kind of comfort blanket to policymakers and people employed in the financial sector.

So what is true?

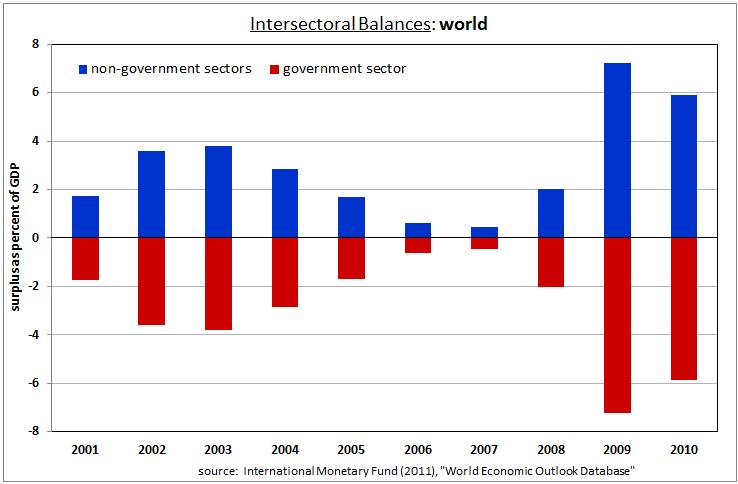

The charts presented here divide the world economy (and the Eurozone) into its government and non-government sectors; essentially public and private sectors. (In the case of the Euro economy there is also the foreign sector, which proves to be insignificant for the zone taken as a whole.) The Euro economy is essentially a microcosm of the global economy, so conclusions relating to the world as a whole relate to the Eurozone as well.

CHART 1

Click for big version.

CHART 2

Click for big version.

These charts show, for every year from 2001 to 2010, private sector surpluses matched by public sector deficits. This means the private sector (firms and households together) are net savers (ie net lenders), meaning they attempt fewer goods and services than their incomes entitle them to. (These private surpluses accumulate to create a "global savings glut".) For the private sector to succeed in its attempts to run large surpluses, the public sector must comply by running large deficits. By definition, the combined surpluses of the private sector must equal the combined deficits of the world's governments. The reality is that, in most years, households and businesses lend to governments because there are limited "investment opportunities" in the private sector.

(The period 2006-07, which shows small private-public imbalances, is not a period that conforms to the orthodox account of household lending balanced by business borrowing. Rather, as British data clearly reveals [http://www.economist.com/node/18713516 ], it was a period of business saving, which means businesses were lending to households as well as to governments. For at least a decade, the business sector has been a lender rather than a borrower.)

If governments do not want to incur deficits as large as the surpluses that the private sector wishes to achieve, then a recession occurs. Government deficits will become larger than governments wish them to be, and, with incomes falling, private surpluses will be smaller than desired. Actual (as opposed to desired) global private surpluses must exactly equal the combined deficits of all governments.

Under the confused orthodox story, the private sector should be in balance (desired and actual) albeit with households in permanent surpluses and firms in permanent deficits. This would, by definition, place the global public sector also in balance.

The reality is that the private sector (as a whole) "saves" by lending to the public sector. Governments are net spenders because the private sector, globally, is a net non-spender. In 2010 the actual global private-public imbalance was about six percent of global GDP. Given the high levels of unemployment globally, the private sectors' desired surpluses are substantially greater than this. Equally clearly, governments, taken together, desire annual deficits substantially less than 6% of GDP.

By following austerity measures, governments increase the gap between the size of the desired private surplus and the size of the desired public deficit. Government spokespeople and assorted financial experts make matters worse by exhorting the private sector to increase its surpluses by paying down debt and by saving (ie lending) more.

The economic crisis will come to an end when private firms and households act to bring their net surpluses down towards zero.

It is unrealistic to expect highly indebted firms and households to take on more debt. Therefore the sovereign debt crisis can only be resolved by those firms and households that are not indebted to spend more. Thus, in a European context, the crisis can only be resolved by those many private Germans, Belgians, Dutch, and indeed Italians (and others from all nationalities) who do not have a debt problem to buy more goods and services from those who do have a debt problem. This is how debts are discharged; by creditors buying from their debtors. In a world of financial imbalance, correction takes place through debtors running surpluses while creditors run deficits.

As incomes increase, a result of more consumption and investment spending by those households and firms who are currently hoarding financial assets, tax revenues increase. In particular, as firms in places like Italy and Greece and Spain (and New Zealand) sell more to dis-hoarding buyers across the world, then government revenues pick up substantially in the countries in which governments are running the biggest deficits.

Alternatively, if the world's private creditors, by continuing to save more, do not allow the world's public and private debtors to discharge their debts, then, one way or another those debts (and credits) must eventually be written off, with much gnashing of teeth from the creditor and financial communities.

The future of the world economy in the next 40 years is entirely up to the households and firms for whom the debts of governments (and other debtor parties) represent their present financial wealth. As time passes, private creditors' claims on future tax revenues become increasingly untenable.

Keith

Rankin teaches economics in Unitec's Department of

Accounting and

Finance.

Keith Rankin

Political Economist, Scoop Columnist

Keith Rankin taught economics at Unitec in Mt Albert since 1999. An economic historian by training, his research has included an analysis of labour supply in the Great Depression of the 1930s, and has included estimates of New Zealand's GNP going back to the 1850s.

Keith believes that many of the economic issues that beguile us cannot be understood by relying on the orthodox interpretations of our social science disciplines. Keith favours a critical approach that emphasises new perspectives rather than simply opposing those practices and policies that we don't like.

Keith retired in 2020 and lives with his family in Glen Eden, Auckland.

Eugene Doyle: Writing In The Time Of Genocide

Eugene Doyle: Writing In The Time Of Genocide Gordon Campbell: On Wealth Taxes And Capital Flight

Gordon Campbell: On Wealth Taxes And Capital Flight Ian Powell: Why New Zealand Should Recognise Palestine

Ian Powell: Why New Zealand Should Recognise Palestine Binoy Kampmark: Squabbling Siblings - India, Pakistan And Operation Sindoor

Binoy Kampmark: Squabbling Siblings - India, Pakistan And Operation Sindoor Gordon Campbell: On Budget 2025

Gordon Campbell: On Budget 2025 Keith Rankin: Using Cuba 1962 To Explain Trump's Brinkmanship

Keith Rankin: Using Cuba 1962 To Explain Trump's Brinkmanship