Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Keith Rankin: Taxes and Benefits for Individuals

Taxes and Benefits for Individuals: Current State and Reform Options

by Keith RankinOn Feb 8 Scoop published my article Personal Income Tax Reform in New Zealand, which looks at taxes for individual New Zealand wage and salary earning tax residents.

Taxes were defined in two possible ways: (i) payments levied on individuals and payable to Inland Revenue; (ii) payments net of credits, levied on individuals, and payable to (and by) Inland Revenue.

From an accounting (and policy) point of view, I will argue now that the first definition is best. Thus, philosophically, payments levied are taxes and credits paid are benefits. However, from an administrative viewpoint, the second definition is probably the best.

The difference between the two approaches depends on how we define and account for tax credits. What are tax credits, and are they benefits? I argue that all tax concessions are tax credits, and that tax credits are benefits. It makes a huge difference to how we conceive and formulate tax and welfare policies.

The administrative role of Inland Revenue (the IRD) is best defined as making levies on and paying credits to individuals. This leaves a role for the Department of Work and Income (WINZ) in paying to households benefits that require case management, realising that in many cases households are single-person entities.

By dividing administrative responsibility this way, the IRD deals in matters of horizontal equity whereby all individuals are treated equally. Further, the IRD, in only dealing with individuals, need not require any information at all about their clients' partners, children, or other personal circumstances. The IRD would only need information about any person's income, business expenses, and their bank account number. (Horizontal equity means treating equals equally.)

WINZ on the other hand should address vertical equity issues, by paying additional benefits, where appropriate, on the basis of exceptional household circumstances. (Vertical equity means treating unequals unequally.) WINZ, New Zealand's welfare agency, therefore does need the full set of household information on all members of households who apply to if for assistance. WINZ is in the business of case management, and its customers may be called "beneficiaries". Ideally, in any liberal capitalist democracy, a relatively small share of the adult population (maybe 10%, probably no more than 20%) would need to be beneficiaries.

If we go back to democratic principles, it is very hard to argue against proportionality of tax liability. Everyone pays at the same percentage rate. The principles of classical economics – which date back 200 years, emphasise private over public property, and pre-date genuine democracy – suggest that the rate of tax should be low as well as proportional. Other principles – namely those which give emphasis to democracy and recognise public property rights – suggest that both equity and efficiency might be enhanced by a higher "flat" rate of tax than advocates of classical economics would accept.

If we choose use the apparently technical language of refundable and non-refundable tax credits, a bigger picture emerges to suggest that – at the level of public accounting and policy-making – New Zealand already does have a tax-benefit system based around the "trust rate" of income tax presently set at 33% (plus 1.7% ACC levy giving 34.7%); a rate much higher than the rates (c. 25%) touted by the ACT Party and other prominent (and classically informed) advocates of flat taxes.

A non-refundable tax credit (NRTC) is any individual benefit (ie payment from government to individuals) that is paid, administratively, as a deduction from a person's tax liability. (In other words, it's a tax concession.) Thus, if a person earning $100,000 per annum has a proportional tax liability of $33,000 and is entitled to an NRTC of $8,000, then that person will pay $25,000 to the IRD. From an administrative point of view, it's a $25,000 tax. From a public accounting point of view, it's a tax of $33,000 offset by a benefit of $8,000.

By definition, a NRTC cannot exceed a person's tax liability. A refundable tax credit (RTC), on the other hand, is the same as a NRTC, except that it can exceed a person's tax liability. It is therefore more easily understood as a form of benefit. If our person earning $100,000 loses her job, she gets to keep her $8,000 tax credit if it is 'refundable', but loses it if it's 'non-refundable'.

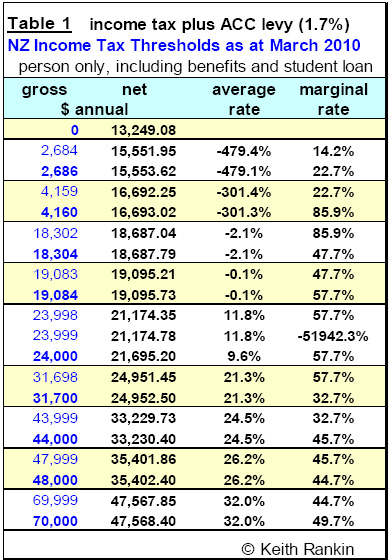

Let's consider the present and future possibilities for a hypothetical single New Zealand tax-payer. She is aged 30, her name is Cathy, and she lives in Wellington where she pays $140 per week on her rental accommodation. She is repaying a student loan. At present, if she has no employment, she is entitled to two WINZ benefits: an unemployment benefit (UB) and an accommodation supplement (AS). Her tax-benefit thresholds are given in Table 1 below, along with her effective average and marginal tax rates.

If Cathy is unemployed she receives a total annual benefit of $13,249 made up from a weekly taxable unemployment benefit (UB) of $190.39 after tax and a weekly non-taxable accommodation supplement (AS) of $64.40. If Cathy gains up to $80 per week ($4,160 per year) of work, she gets to keep her benefits, but may move into a higher tax bracket. Thus at annual earnings of $2,686 ($51.65pw) she moves to a marginal tax rate of 22.7% (21% normal tax, 1.7% ACC levy).

Once she reaches $80 per week, her benefit is abated (ie clawed back) at 70 cents per dollar of extra earnings, creating an effective marginal tax rate (EMTR) of 85.9%. As Cathy's earnings rise from $80 to $352 per week ($4,160 to $18,304 per year) she keeps only 14.1% of her additional earnings. Once her part-time wages exceed $352 per week, she becomes better off by coming off the UB while qualifying for an AS that's abated at 25 cents per extra dollar earned, giving an EMTR of 47.7%..

However, at $367 per week ($19,084) Cathy must now make payments on her student loan (SL). This raises her EMTR to 57.7%. Cathy now keeps 42.3% of her extra wages

Cathy gains some relief if she can get her annual earnings up to $24,000. She now qualifies for the $520 per annum Independent Earner Tax Credit (IETC), which brings her average tax rate down, while keeping her marginal rate at 57.7%.

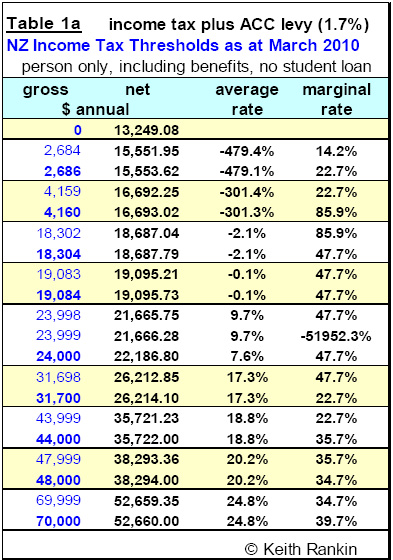

Once Cathy's earnings rise to $31,700, she no longer receives any AS, so she now pays tax at the marginal rate of 32.7% (21% ordinary tax, 1.7% ACC levy, 10% student loan repayment). At this point she ceases to be a client of Work and Income, but she continues to receive tax concessions (ie non-refundable tax credits) from IRD. If Cathy was not paying back a student loan, Table 1 would change for higher earnings, and would become Table 1a below.

Table 2 (below) shows Cathy's gross and net position, expressed in the conventional way, as in Table 1a, in the left-hand panel, and showing the full benefit breakdowns in the right-hand panel. To conform with accounting principles derived from the principle of horizontal equity, Cathy's correct post-tax private earnings are displayed as gross earnings less a flat rate tax of 34.7% (33% trust rate plus 1.7% ACC employee levy). Thus for example, if Cathy incurs an annual wage of $15,000 to her employer(s), $9,795 – $15,000 less 34.7% – represents her private share of that wage, and the remaining $5,205 represents the public share. All benefits, including tax credits, are paid out of public income, to which she has contributed $5,205 as income tax.

Cathy's total benefits are the difference in her actual disposable (ie net) income and her private post tax earnings. Thus for gross earnings of $15,000, she receives $18,221 which exceeds her $9,795 private earnings by $8,426. Her total benefit of $8,426 – paid out of public funds – is broken down into three components: unemployment benefit (UB) of $2,312; accommodation supplement (AS) of $3,349; tax credit of $2,765.

If we glance down the "total benefits" column, we see that the minimum benefit payable is over $5,500. Every individual (except some on very high incomes not shown) qualifies for and receives a benefit. Most people currently receive total cash benefits above $6,000. We can see that the present system conforms quite well to the principles of horizontal equity – treating equals equally – once we account for it in this way. Tax is incurred at 34.7%, benefits approaching $7,000 are paid. In addition, principles of vertical equity are applied to individuals with earnings below $18,000 who most likely face some special circumstance that prevents them from having adequate private earnings. The tax system is far from broke. However it is clear that workers on below-average wages are receiving too little in the way of tax credits.

The tax scales can easily be improved, enhancing efficiency and equity. Use of an appropriate tax-benefit accounting system – as I have done in Table 2 – suggests ways we can make improvements. (Readers should be reminded that no issues relating to children are addressed here. The findings shown here will be applied to families with children later this month.)

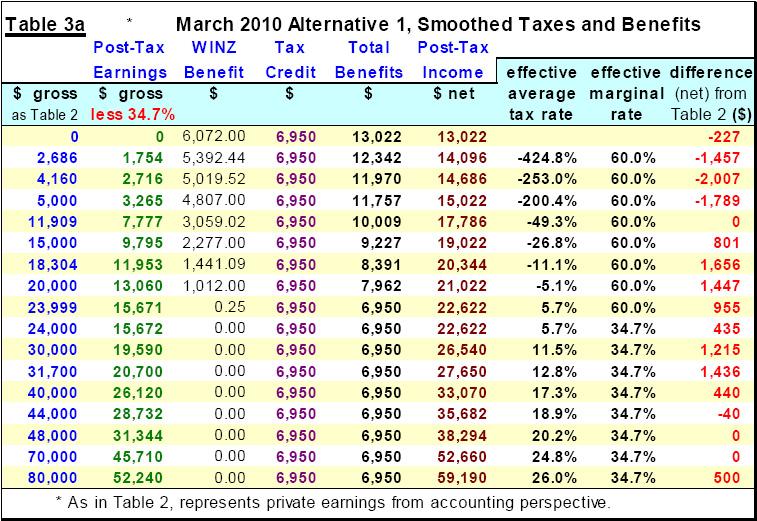

The most obvious question is: Why should a person on $44,000 get a benefit – in the form of a tax credit – of nearly $7,000 whereas someone on $31,000 gets a benefit close to $5,500? There is no answer based on principle. It's simply a result of the ad hoc nature of our tax scales. Tables 3a and 3b show ways that we can iron out these benefit-wrinkles, through a full application of the principle of horizontal equity, combined with a lesser application of the principle of vertical equity. The final columns of Tables 3 show the variations in post-tax income that would arise.

Click to enlarge

Horizontal equity works in Table 3a simply by applying a flat-rate tax of 34.7% – the current trust rate plusaaaa ACC levy applied to employee earnings – and paying an equal tax credit of $6,950. Negative equity is applied to persons grossing less than $24,000 through a WINZ benefit that serves as a combination of unemployment compensation and accommodation assistance.

The result is that individuals earning over $24,000 would generally pay a tax of 34.7% on all additional dollars earned, while people with similar circumstances to Cathy would effectively pay 60 cents in the additional dollar due to a combination of taxes at 34.7 cents and their WINZ benefit eroding at 25.3 cents.

Many will object because moving to such a tax scale represents a tax cut for persons earning over $70,000 per year, and because people on very low incomes appear to lose out. Certainly it has been widely argued that both persons on the current top tax rate of 39.7% (with ACC) and workers on below average wages need a tax break. Adapting the current system to equity principles achieves that for both groups.

For those on lower earnings – essentially beneficiaries – there are two major gains. First, for beneficiaries earning more than $4,160 (80 per week), there are reduced penalties on additional part time work. They get to keep 40% rather than 14.1% of additional earnings. Second, for all beneficiaries, the major part of their benefit is payable as of right (as a tax credit) without having to have any contact with WINZ, the government welfare agency. Third, the WINZ benefit given here for zero earnings ($6,072) represents a simple example; that of a 30 year-old single person (Cathy) in the event of her unemployment. The case management process at WINZ would be able to set higher benefit levels for persons of greater need; that's the principle of vertical equity.

The tax-benefit scales in Table 3a can be represented by just three parameters: (1) $6,950 refundable tax credit amount; (2) 34.7% income tax rate, and (3) 60% beneficiary marginal rate. If the reforms suggested by this equity accounting approach were to be implemented, the focus of debate would change. Persons on the political left might advocate a rise in parameters 1 and 2. Persons on the political right might favour a reduction in all three parameters. There would always be a way through which people at the bottom, middle or top of the income scale could be made better off. Debates about taxes and benefits would become much less arcane, much easier for voters and tax-payers to understand, and apply their own values to.

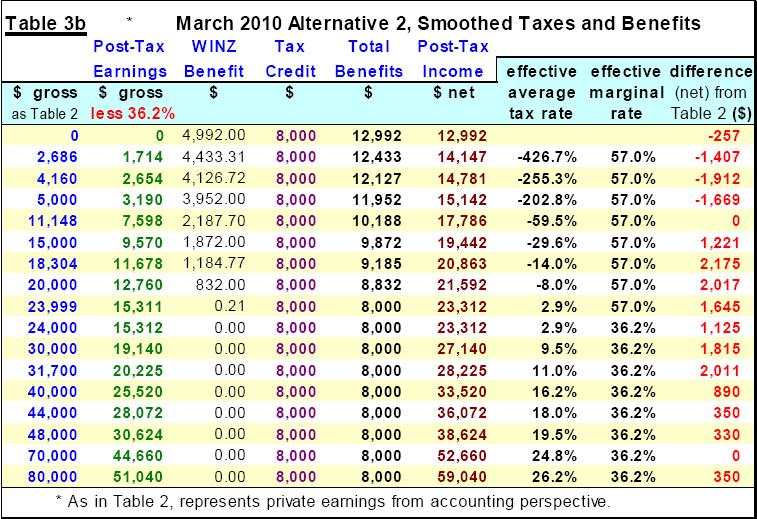

In Table 3b I show an alternative set of tax-benefit scales, based on the same principles as Table 3a. The refundable tax credit is raised from $6,950 to $8,000 per year, about $5 per week below the present unemployment benefit for young adults. The tax rate is raised 1½ percentage points, from 34.7% to 36.2%. And the beneficiary marginal rate is reduced from 60% to 57%. By making this change, persons grossing $70,000 per year remain unaffected.

Click to enlarge

The alternative scale gives lesser tax reductions to persons grossing over $70,000. It gives greater gains for low-wage workers. And it gives greater incentives for beneficiaries to increase their hours of work. Perhaps most importantly, it sets the refundable tax credit at a level of $8,000 ($154 per week) that would ensure that many people who might be entitled to a small WINZ benefit to not bother to subject themselves to case management. In other words, on its own it would just suffice, for many people, as a short-term benefit to tide them over through a period of unemployment, sickness, or full-time study.

With a single personal tax rate, set at the trust rate, opportunities for tax avoidance are reduced. Likewise, the resources required by WINZ (and other, eg Ministry of Education) bureaucracies would be markedly fewer. Principled simplicity can be as good for efficiency as for equity.

Two questions arise: Does some unconditional income create "slackers", who choose to live off the efforts of others without contributing themselves? And is the tax-benefit system affordable at the illustrated rates? As a species concerned about equity, humans worry about non-contributors.

My answer to the first question is a qualified "no". Some people of working age may be able to live on $8,000 per year. They would impose a very low ecological footprint, and would for the most part be contributing to society in ways other than through paid work. More importantly, for those who worry about the indolence of others, reduced effective marginal tax rates and reduced conditionality of basic of benefit – now, after reform, paid by IRD rather than WINZ – frees up the supply side of the labour market, rewarding effort and enterprise across all income ranges.

With the rates suggested, overworked people would be encouraged to work a bit less, because they would not lose any tax credits as a result of such a decision. On balance, by rewarding more people more for extra work, the labour supply effect is likely to be positive. Economic efficiency improves if people work less when the marginal cost of paid work exceeds the marginal benefit.

Is the tax-benefit system affordable at these suggested rates? I believe that both the Table 3a and Table 3b options are fiscally viable. First, the net payments are for the most part quite similar to present net payments. Second, fewer people will rely on WINZ benefits for the majority of their disposable income. Third, the biggest breaks will go to people in work in the middle quartiles of the income distribution. They will be able to service their debts more easily, and save more readily, while continuing to spend, giving the country's economy the impetus it needs to grow.

Fourth, in periods of recession or slow recovery, with relatively high unemployment, cyclical deficits in the public sector accounts are inevitable. Tax-benefit parameters based on horizontal equity contain inbuilt fiscal stabilisers that allow economies to tick over during downturns, reducing the duration or recessions; also generating fiscal surpluses during expansions.

If under some criteria the parameters suggested prove fiscally unsustainable, then the remedy is simply to adjust one, two or all three parameters. For example, reducing the refundable tax credit, raising the trust tax rate, or raising the beneficiary marginal rate could all help to reduce a structural budget deficit, were such a deficit to exist. (Other measures to balance the books, if such a balancing were deemed necessary, might be to make adjustments to areas of the tax system other than personal income taxes; for example a reintroduction of death duties.)

My hunch is that the increased economic freedom – made possible by transparent, efficient and equitable tax-benefit parameters – would in fact soon create pressures to reduce budget surpluses by paying out increased growth dividends in the form of increased tax credits.

We can raise the standard of debate about taxes and benefits by improving the clarity of the public accounts, by showing rather than hiding the benefits that are currently counted as tax offsets. While effective debate about taxes and benefits always involves some degree of numeracy among our citizenry, nobody should have to be a maths genius to be able to evaluate the fairness or otherwise of the payments we make to and draw from the public accounts.

It remains appropriate that, however transparent or opaque the presentation of the public accounts is, the IRD continues to be the agency that pays benefits that come in the form of individual tax credits – applying horizontal equity (Tables 3) or revealing horizontal inequity (Table 2) – while another agency (WINZ) pays all benefits that require case management (applying vertical equity).

krankin @ unitec.ac.nz; keith @ pol-econ.com

Keith Rankin

Political Economist, Scoop Columnist

Keith Rankin taught economics at Unitec in Mt Albert since 1999. An economic historian by training, his research has included an analysis of labour supply in the Great Depression of the 1930s, and has included estimates of New Zealand's GNP going back to the 1850s.

Keith believes that many of the economic issues that beguile us cannot be understood by relying on the orthodox interpretations of our social science disciplines. Keith favours a critical approach that emphasises new perspectives rather than simply opposing those practices and policies that we don't like.

Keith retired in 2020 and lives with his family in Glen Eden, Auckland.

Binoy Kampmark: Bratty Royal - Prince Harry And Bespoke Security Protection

Binoy Kampmark: Bratty Royal - Prince Harry And Bespoke Security Protection Keith Rankin: Make Deficits Great Again - Maintaining A Pragmatic Balance

Keith Rankin: Make Deficits Great Again - Maintaining A Pragmatic Balance Richard S. Ehrlich: China's Great Wall & Egypt's Pyramids

Richard S. Ehrlich: China's Great Wall & Egypt's Pyramids Gordon Campbell: On Surviving Trump’s Trip To La La Land

Gordon Campbell: On Surviving Trump’s Trip To La La Land Ramzy Baroud: Famine In Gaza - Will We Continue To Watch As Gaza Starves To Death?

Ramzy Baroud: Famine In Gaza - Will We Continue To Watch As Gaza Starves To Death? Peter Dunne: Dunne's Weekly - A Government Backbencher's Lot Not Always A Happy One

Peter Dunne: Dunne's Weekly - A Government Backbencher's Lot Not Always A Happy One