Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

What Obama Actually Said About Health Reform

What Obama Actually Said About Health Reform

by Michael Collins

1965 -

President Lyndon Johnson signs Medicare bill while President

Harry Truman looks on. Truman signed up for Medicare right

away.

President Obama closed his address to the joint session of Congress by scolding those who have raised the absurd charges regarding his health care initiative. It was well timed and diverted attention from fundamental flaws in his proposal.

This article examines the Obama plan as outlined in his speech. His goals were clear and the speech was well structured. The heart of the address provides the type of information necessary to judge the merits of the plan as presented.

Obama got serious when he said, "The plan I'm announcing tonight would meet three basic goals:

"It will provide more security and stability to those who have health insurance.

"It will provide insurance to those who don't.

"And it will slow the growth of health care costs for our families, our businesses, and our government." Pres. Barack Obama, Sept. 9

Cost and availability are the core issues in health care today. They subsume all others. What's missing here? Instead of universal coverage, the uninsured get "insurance," most likely private insurance, if they can afford it. Instead of beating back prices or bold initiatives to reduce them, we're hearing "slow the growth." Health care costs are unaffordable to many already. The promise here seems to be that they'll still be unaffordable, just less so.

"Bending the curve" may happen but it fails to address the key problem -- people can't afford insurance rates and medical bills. As a result they get sick more, suffer more, and die before their time.

"Here are the details that every American needs to know about this plan"

Obama detailed the impact of his plan on two distinct groups, those currently with insurance and those without. This is a key distinction since the public option, for example, is available to only those without insurance.

Those with Insurance

Those with insurance were promised that "nothing in our plan requires you to change what you have." That's assuring to some. But to others who lave plans that are too expensive, plans purchased directly from insurance carriers, there may be a desire or need to change to a more affordable plan. You're out of luck. Let's say that you own a small business and pay $1200 an employee a month for health insurance. The plan offers no apparent benefit other than slowing "the growth of health care costs."

The plan will offer four ways "to make the insurance you have work better for you." It will: get rid of preexisting conditions as a reason to deny coverage; bar insurance companies from dropping coverage due to a major illness; limit "out of pocket" expenses; and require coverage for preventative care. These are all positive steps.

That's it for "security and stability." You can stay in your current plan. You can go elsewhere with certain long overdue guarantees of coverage but for those insured, there's no freedom to choose a Medicare-like public option or use the insurance "exchange" There's no security that you will ever see affordable health care.

Health insurance and pharmaceutical companies who have jacked up prices at record setting rates will be unimpeded.

The health care "exchange" that was part of Obama's campaign proposal is not available to those with insurance:

"But an additional step we can take to keep insurance companies honest is by making a not-for-profit public option available in the insurance exchange. Let me be clear – it would only be an option for those who don't have insurance." Sept. 9

We're left to assume that "keeping the "insurance companies honest" is only a benefit saved for those citizens who are uninsured.

Those without Insurance

Those without insurance will be offered membership in "one big group" that will leverage their numbers to drive competition from insurance companies on a public "insurance exchange." The exchange aims to fulfill a huge promise:

"If you strike out on your own and start a small business, you will be able to get coverage. We will do this by creating a new insurance exchange – a marketplace where individuals and small businesses will be able to shop for health insurance at competitive prices." Sept. 9

What if you don't have a job? What if you have a job but can't afford the prices on the "exchange?" This was not addressed.

The president elaborated his argument for the "exchange:"

"Insurance companies will have an incentive to participate in this exchange because it lets them compete for millions of new customers." Sept. 9

Who are the members of this group that the insurance companies will so desire? They're the uninsured, the people who get sicker more frequently and have great medical needs because they're uninsured. Is that an appealing market for companies who are in the business of excluding sick people? Is there some major group of very healthy uninsured ready to balance out the generally poor, low income uninsured?

To further bolster the insurance "exchange," Obama offered this argument:

"As one big group, these customers will have greater leverage to bargain with the insurance companies for better prices and quality coverage. This is how large companies and government employees get affordable insurance." Sept. 9

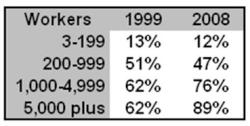

No it isn't. The largest companies have "self funded" health insurance plans. They don't buy insurance coverage from the Blue Crosses of the world. They set up a fund for benefits that pays for employee health care. They hire out the administration of benefits to private insurance companies who issue checks and reimbursements but that money is from large companies. The entire "exchange" argument is based on a factual error. Since the assumption of competition underlies the "exchange," the plan crumbles for those without insurance.

From Exhibit 10.1 Kaiser Family Foundation 2008 (p. 162)

Why would companies do this? Because self funded plans save money by cutting out insurance company profits as an operating cost. Self funded plans also provide more control of expenditures. There are no $800,000 a day salaries for plan employees as we've seen at insurance companies.

The underlying premise for the insurance exchange for the uninsured is flawed operationally and factually. So how will people pay for this coverage?

Tax credits! We're told that, "For those individuals and small businesses who still cannot afford the lower-priced insurance available in the exchange, we will provide tax credits, the size of which will be based on your need."

Who will be in the exchange and what can they afford with or without tax credits?

72% of the uninsured are below the income level required to afford

employer health insurance. Based on U.S. Census Bureau data, 2005 Link

This augmented chart shows an estimate of the income level required for the uninsured to afford a "company insurance plan." Self funded plans covered 54% of those insured (p. 162) at the time this data was collected. According to the study, an individual needs income of 300% of the federal poverty level, $27,000 to afford "employer insurance." A family of four needs an income of 300% of the federal poverty level for families or $57,000 for "employer" insurance. This study didn't presume an insurance "exchange" but the analysis is applicable as a model for answers we need to determine the ability of people to purchase insurance under the president's proposal.

Even if everything worked perfectly for the uninsured, the president said, "This exchange will take effect in four years, which will give us time to do it right." If that's the criterion, do it right, it will take a lot longer than four more years before the uninsured benefit.

With a flawed basis for the exchange, no mandatory participation by insurance companies, no price controls, and a poorer, less healthy "big group," what chance is there that the very limited public option proposed will be "be self-sufficient and rely on the premiums it collects" as Obama requires? What chance is there that private insurance companies will be more inclined than they are today to insure those that they don't want to insure?

What about Medicare?

Medicare is a well liked plan with lower administrative costs, and no requirements for shareholder returns. It's also much less intrusive in care decisions than private insurance plans. But that's not in the cards. The president said:

"Since health care represents one-sixth of our economy, I believe it makes more sense to build on what works and fix what doesn't, rather than try to build an entirely new system from scratch." Sept. 9

Medicare is a national program in operation since 1965. It provides universal health care for those 65 and older. It faces challenges from the bulge in beneficiaries that don't negate its lower unit costs, lower administrative fees, and high satisfaction rate. Medicare would be even more effective in delivering improved health if seniors were it able to negotiate discounted drug rates with the major drug companies. But Congress outlawed that in 2004. That wasn't mentioned as part of the plan. Why?

In his apparent attempt to preserve the private health insurance industry and to appease the major pharmaceutical companies, the president missed a key lesson from the market place.

When large companies want to save money on employee health costs, they get rid of the private insurance companies. As a result, they save money and often offer more coverage. They save even more money bypassing the built in cost of insurance company profits and excessive CEO compensation.

Medicare is the big company self funded plans writ large. In fact, you could argue that the Medicare approach of direct funding for "the big group" of seniors was the model for self funded big company health plans.

Isn't it time to stand back and reevaluate the entire process?

Isn't it time to say no to more corporate welfare?

How many more bailouts can we take?

This article may be reproduced in whole or in part with attribution of authorship and a link to the source of this article: http://agonist.org/michael_collins/20090910/what_obama_actually_said_about_health_reform

Binoy Kampmark: Last Acts -Time For Biden To Pardon Assange

Binoy Kampmark: Last Acts -Time For Biden To Pardon Assange Binoy Kampmark: Foiling Rupert Murdoch - Project Harmony Misfires

Binoy Kampmark: Foiling Rupert Murdoch - Project Harmony Misfires Ian Powell: Commissioner’s Approach To Healthcare Provision - ‘Slash And Burn’

Ian Powell: Commissioner’s Approach To Healthcare Provision - ‘Slash And Burn’ Jack Yan: The Case For Brand Aotearoa

Jack Yan: The Case For Brand Aotearoa Ramzy Baroud: Unity Above Else - The Only Road to the Liberation of Palestine

Ramzy Baroud: Unity Above Else - The Only Road to the Liberation of Palestine Binoy Kampmark: Finding The Unmentionable - Amnesty International, Israel And Genocide

Binoy Kampmark: Finding The Unmentionable - Amnesty International, Israel And Genocide