Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Sludge Report #183: Sunshine On A Cloudy Day

Sludge Report #183: Sunshine On A Cloudy Day

Five Years To The Day Since It Last Happened - NZ Interest Rates Are Cut

By Alastair Thompson in the Reserve Bank Lockup

The Reserve Bank has this morning cut interest rates for the first time since July 2003, and alongside recent petrol price falls, brought some much needed good news to NZ household bank accounts .

The issue which will immediately arise will be how soon will Banks follow the Reserve Banks lead. (Sludge report prediction - watch for Kiwibank to lead the charge to lower rates.)

On 24 July 2003 the interest rate fell from 5.25% to 5%. Mortgage interest rates at the time were around 6.5-7% compared to 9-11% now. (Note: In the previous interest rate cycle rates peaked at 6.5% in May 2000 and stayed there for six months. This time the story is much to same with a lengthy period of no change at the highpoint of 8.25%. The peak in this cycle was reached in June 2007 - 13 months ago. )

This morning the bank announced a rate cut in the OCR of the same size - 25 basis points or 1/4 of a percent - to 8%.

Following this the OCR - cash rate that banks borrow from each other at - is now at 8% indicating floating rates in the 9.5% zone. After the cuts interest rates remain a full 3% higher than they were at the end of July 2003 and 1.5 points higher than they were at the height of the previous cycle..

Déjà vu All Over Again - First Interest Rate Cut in 5 Years Falls On Exact Same day.

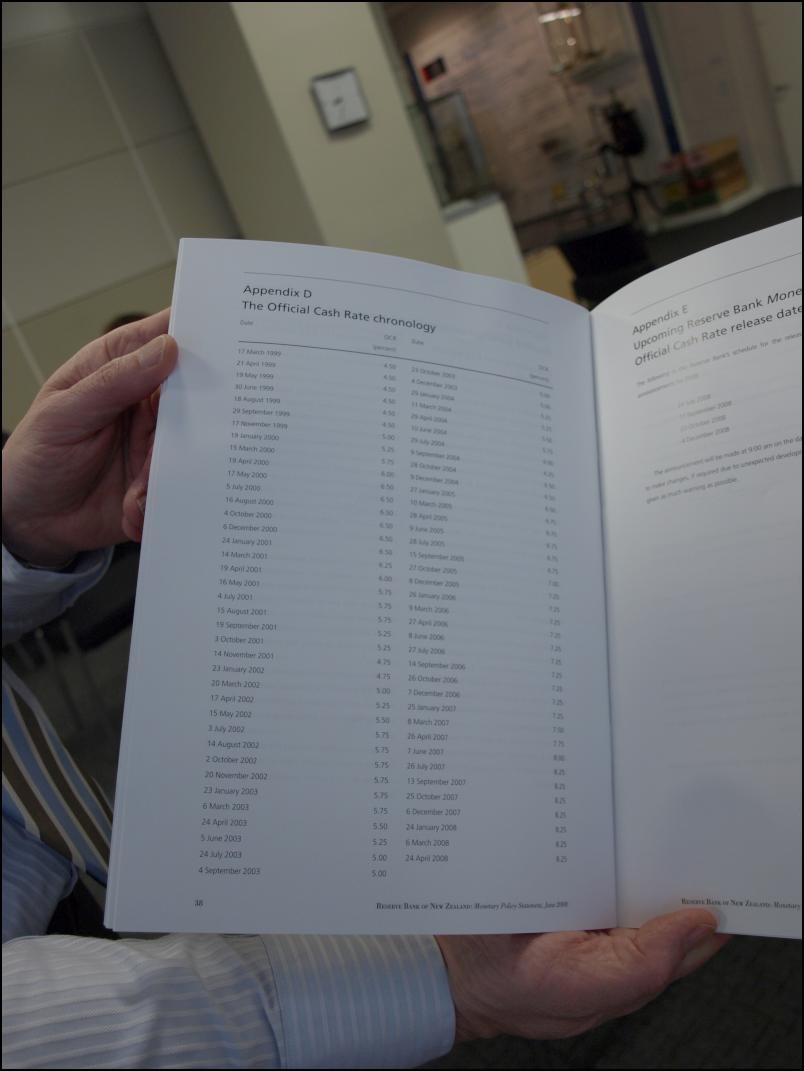

Image shows "The Official Cash Rate Chronology" from a recent copy of the Reserve Banks MPS.

Click for big version

Today’s is a modest response to what Alan Bollard described in his unusually long commentary as "more unpleasant international news" and "risk that the domestic economy will slow further" this is countered by "an expectation that CPI inflation will peak at 5% in the September quarter."

However notwithstanding the generally negative sentiment in the business community at large today's statement is actually fairly bullish about NZ's economic prospects.

The bank is forecasting that "high export prices and an expansion in fiscal policy [i.e. Tax Cuts] are expected to contribute to a gradual pickup in activity in 2009."

In other words the bank is expecting NZ to experience at worst a brief recession at this time. Notwithstanding the oil shock, food price explosion and the global financial crisis.

Which while not altogether comforting puts New Zealand in a very unusual position in global terms.

Recessions in the EU, UK and US for example are deepening and their central banks have considerably less room to cut interest rates than ours has.

And Dr Bollard ends his statement today with words which will be music to the ears of NZ households.

"Provided that the outlook for inflation continues to improve and there is no excessive exchange rate depreciation, we would expect to lower the OCR further."

Meaning further rate cuts can be expected. Which of course is what everybody, including the Government, would like to hear.

That said there is considerable irony in the details of this closing remark - particularly in the "provided… there is no excessive exchange rate depreciation" part of it. (Note: this is really addressed at the money market traders requesting that they not take too knee-jerk an approach to the announcement and take the dollar down too fast. )

The irony is that for most of the last several years the bank has been complaining about the exchange rate being excessively high and done its best to talk it down at every opportunity.

NZ's high dollar effect in recent years has been exacerbated by the carry trade - where foreign borrowers invest in Kiwi Dollars to earn what they hope will be both exchange rate rises and a huge margin between their domestic interest rates and our stratospheric ones. Much of this trade has recently unwound but this may be a temporary phenomena given how things are shaping up in the NZ Dollar prospects equation.

An example of how hot NZ currency has been can be seen in the fact that last year NZ Govt. treasury bonds - already in short supply due to chronic fiscal surpluses - became so hard to get a hold of that the Reserve Bank changed the rules on what it would allow banks to use as security for repo-market transactions.

However recent events have changed much of this.

Over the past six months the NZ Dollar has fallen - especially on a TWI basis (against the Australian Dollar, Yen, Pound and Euro) and NZ is running some mild risk of importing some inflation if it keeps falling.

However even that cloud has a silver lining. NZ tends to export more to these countries than it imports and so the downside inflationary risk here is not intense.

Exiting the Reserve Bank this morning Scoop ran into Business New Zealand's Phil O'Reilly who was clearly cheered by the announcement noting that it was good news for producers.

The bottom line from today's statement is that in the current international investment environment NZ is offering a quintuple bonus of 1) high interest rates 2) exchange rate upside [from low recessionary risk] 3) negligible unemployment 4) secure mortgage markets and 5) a rock solid government fiscal position.

The only dark cloud we have is our persistent current account deficit - but even that is unlikely to mount any serious impediment to NZ remaining a hot incoming international investment destination - not in the least because it means that finding investment opportunities here is not overly onerous.

POSTSCRIPT: In the immediate aftermath of the somewhat unexpected rate cut decision - economists were divided on the probabilities before today - the NZ Dollar has fallen 75 basis points.

Links to

sites to view exchange rate reaction.

http://www.forexdirectory.net/nzd.html

http://www.dailyfx.com/charts/ChartStation.html

Anti©opyright Sludge 2008

Alastair Thompson

Scoop Publisher

Alastair Thompson is the co-founder of Scoop. He is of Scottish and Irish extraction and from Wellington, New Zealand. Alastair has 24 years experience in the media, at the Dominion, National Business Review, North & South magazine, Straight Furrow newspaper and online since 1997. He is the winner of several journalism awards for business and investigative work.

Richard S. Ehrlich: Deadly Border Feud Between Thailand & Cambodia

Richard S. Ehrlich: Deadly Border Feud Between Thailand & Cambodia Gordon Campbell: On Free Speech And Anti-Semitism

Gordon Campbell: On Free Speech And Anti-Semitism Ian Powell: The Disgrace Of The Hospice Care Funding Scandal

Ian Powell: The Disgrace Of The Hospice Care Funding Scandal Binoy Kampmark: Catching Israel Out - Gaza And The Madleen “Selfie” Protest

Binoy Kampmark: Catching Israel Out - Gaza And The Madleen “Selfie” Protest Ramzy Baroud: Gaza's 'Humanitarian' Façade - A Deceptive Ploy Unravels

Ramzy Baroud: Gaza's 'Humanitarian' Façade - A Deceptive Ploy Unravels Keith Rankin: Remembering New Zealand's Missing Tragedy

Keith Rankin: Remembering New Zealand's Missing Tragedy