Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Chris Sanders: The Ghost Of Adam Smith

Sign up for the wire at:

http://www.unansweredquestions.org/headlines.php

Unanswered Questions : Thinking for ourselves.

(Also distributed - as a special item - to the Scoop Real Deal and Eco-Economy news-by email lists)

Sanders Research Associates Ltd. provides international strategic planning and risk management services to both corporate and private clients. SRA also publishes a webzine available by subscription. Visit http://www.sandersresearch.com to get a good feel for the real deal.

SRA Commentary:

The Ghost Of Adam Smith

or why the perps of 911 are hiding in plain site

By Chris Sanders

May 24, 2004

© 2003-5. Sanders Research Associates. All

rights reserved.

FROM:

http://www.sandersresearch.com/Sanders/NewsManager/ShowNewsGen.aspx?NewsID=642

Civil government supposes a certain subordination. But as the necessity of civil government gradually grows up with the acquisition of valuable property, so the principal causes which naturally introduce subordination gradually grow up with the growth of that valuable property.

- Adam Smith (1976) An Inquiry into the Nature and Causes of the Wealth of Nations, Volume 2, Book V, Oxford, Clarendon Press, ISBN 0-19-828184-6, p. 710

A stressed network organised around a few crucial nodes is liable to collapse. What if you saw the collapse coming? Might you not try to improve your position in light of your knowledge? Might you not even try to ensure that the timing of the collapse was to your advantage even if not to the advantage of others?

Wall Street: does she or doesn’t she?

In a few short weeks Wall Street has changed its mind again. In March the Street thought that the Fed would not raise interest rates this year. Today money market forward rates are pricing two hundred basis points of tightening within a year and three hundred by the end of 2005. Bond market yields have risen to reflect these expectations, but not nearly enough if they are indeed right about where Fed funds are headed. Technical analysts are excited because bond yields have surged above their longer term averages. Currency markets have bought dollars on the assumption that higher interest rates and stronger growth in the US are good reasons to sell yen and euros. Stocks on the other hand have fallen as that market worries about the impact of higher interest rates on corporate profits. And commodities other than oil have fallen on the prospect of tighter money and a slower world economy.

This change of mind has apparently been driven by the improvement in the US employment outlook. Wage and salary accruals by American corporations have been climbing for a year, but are still being outpaced by corporate profits. Absent a collapse in demand, it is plain that the job outlook has improved. The long jobless recovery is finally producing results for the work force, at least for the non-manufacturing work force.

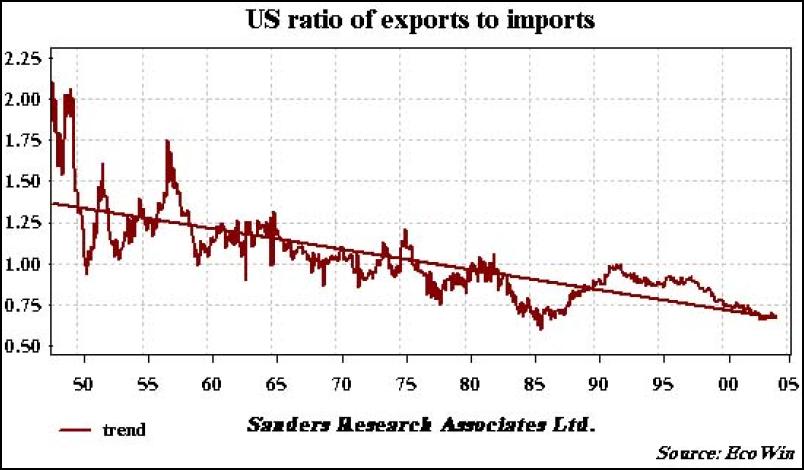

Manufacturing employment[i] stopped falling for the first time in nearly four years in February. A paltry 37,000 jobs have been created since. The lack of job creation in manufacturing is pertinent because it will only be by making things with high value added and selling them abroad that the US will be able to stabilise its massive trade deficit. The trade deficit in goods was a mind-boggling $57 billion in March, representing an annual rate of $687 billion. The ratio of exports to imports has fallen steadily for the last forty years, from 1.2 times imports to a mere 70%. As we have observed in other articles, the trade deficit and dependence on foreign finance have become systematic and structural, begging the question: can the US external account be stabilised at all?

Click for big version

To globalise today means to specialise

It has become almost as fashionable to discuss and accept globalisation as it has become to change one’s economic forecasts to fit short term market price action. One problem that this raises is that globalisation does not mean the same thing to all people. In its most generic sense globalisation has been with us at least since the 17th century. But what it means today is not simply interconnectedness, but rather a particular type of interconnectedness in which the areas that we define as nation-states become more specialised economically, more hierarchical politically and dis-intermediated by networks of internationally connected interest groups.

So today we see the US becoming specialised in finance and war, China in manufacturing, India in services, and so on. The US political economy is becoming more hierarchical as a consequence with a widening gap in incomes and wealth and collapsing constitutional government. And a variety of networks have evolved with a stake in globalisation and with interests shared internationally with similar networks. One of these is what we call the International Security Complex.

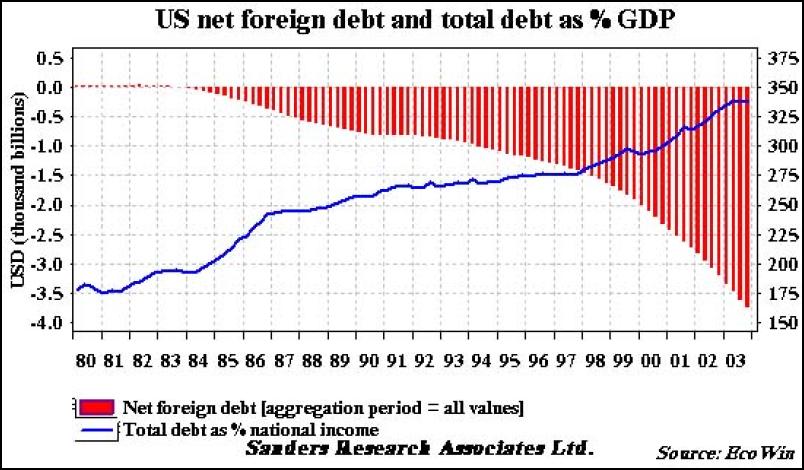

Viewed from this perspective, American deindustrialisation is the result of a sort of economic specialisation, in which high value added production is moved offshore while the onshore (American) economy concentrates in low economic value-added but high political value-added finance and “security.” This is not generally justified or analysed as such; it is rather excused on the basis that the US economy is better than others at “innovation” and “ideas.” One can measure the impact of this on the US by counting the number of lost manufacturing jobs, looking at the proportion of GDP devoted to national security and finance, noting the huge role of government in venture capital, education, research and development, and observing the balance sheet consequences. These can be summed up in a debt to GDP ratio of over 330% and a net foreign debt of 33% of GDP.

Click for big version

In the specialised, globalised world, what is national security?

This sort of “specialisation” violates the most basic assumptions underlying the concept of national security because it exports strategically vital portions of the national supply and manufacturing chain. One of the best examples of this is the fact that virtually all of the world’s semiconductor manufacturing is conducted in one industrial park on the island of Taiwan. From a national point of view this is a grave risk to American security that extends the American security frontier unnecessarily to Asia. From an International Security Complex point of view it is a perfectly rational and even desirable situation since the relationship between the military establishments of the two countries is probably closer even than that between the two militaries and their respective diplomatic establishments. The example par excellence is the relationship between the US and Japan, where the post war development of the Japanese economy owed a much to the opening of American markets and the symbiotic relationship that was built between the ruling elites in both countries.[ii]

Specialisation on this scale depends on the completely free circulation of capital and goods unchecked. There is nothing particularly new about this. Indeed, the world economy before the First World War was arguably freer than it is today. But today’s global economy is more specialised, and is becoming more so. For example, American firms increasingly contract out production to factories that may actually be located in several countries, with raw materials and parts being moved between them. What used to be the company warehouse is a container. What appears superficially to be a very flexible system is in fact very vulnerable to outside disruption and attack, because corporations organised in this way no longer maintain internally the inventories, personnel, and operating systems that would allow them to cope with a disruption to the supply chain. What applies to the corporation applies to the nation as well.

The nation is dead. Long live the network!

One way to make the point more clear is to approach it in terms of a network. A global system based on nations that internalise as much as possible of the production process is closer to a distributed network with many powerful nodes and hence more resilient to outside shocks. However, evolving globalisation is an excellent example of a system conforming to a power law distribution in which only a few nodes are really powerful. Indeed, the system seems to tend towards a system in which only one node has real power. The problem is that such a system is stable until something disrupts the centre causing it to become highly unstable and vulnerable to complete collapse.[iii]

This has enormous implications for investors. The models that most of them (at least the ones that are not insiders) are using are based on explicit or implicit risk calculations that assume a distributed and hence more stable world. As the world transitions towards a less distributed topology, characteristics that used to limit systemic risk are lost.

Consider the evolution of pension fund management. Originally pension funds adopted relative performance benchmarks as opposed to absolute return objectives because of the demonstrable fact that most fund managers could not beat market indices. This logic was always in our view a bit of a red herring because a benchmark is just another portfolio and an arbitrary one at that. But once most pension funds moved to benchmarking performance, the entire industry gravitated toward the same portfolio. This inevitably reduced the diversification benefits inherent in stock diversification in the first place with the result that the benchmark became the security. The S&P 500 is now the stock. This has happened to one degree or another in every market that the pensions are invested in, since anyone who wants to bid for their business has to adopt their methodology. This inbuilt bias has a powerful leavening effect on market practice. Recognising this, the pension funds have cast their nets wider and wider for non-correlated style and performance, with the ultimate effect that every area that they move into eventually loses that attraction. The end result is the same. Diversification benefits are attenuated and risk rises.

Click for big version

The rich are getting richer

There are parallels in the political system, and for related causes. Rising risk means rising volatility, and rising volatility has an interesting by product: the rich get richer and the poor get poorer. The dynamic behind this is various and compelling. To begin with, it is only the rich that can exploit the significant market mispricing that greater volatility brings because they are the only ones with the cash to take advantage of it or sufficient assets to secure the credit lines necessary to short the markets. At the same time, the finance sector which intermediates the flow of cash and securities has emerged from each business cycle since the Second World War bigger than the last. We have noted in other articles the extraordinary degree to which even the industrial sector owes its profitability to finance. If you doubt this, think of GE Capital, GMAC, Boeing aircraft leasing and so on. Taken together, it represents more than a quarter of GDP. But even this understates the size of the sector. Given that the Fed is a private monopoly owned by the sector it supervises, monetary policy is necessarily biased towards financial goals as opposed to production goals.

It is therefore no wonder that labour is viewed solely as a factor of production the money cost of which must be minimised. The benefits and risk-reducing characteristics of community equity, a stable work force, quality output and so on take second seat in a system that values earnings per share more highly and where industrial output is chiefly valuable as collateral for a leasing or insurance transaction rather than for dependability and longevity. Place becomes unimportant, and it matters not where the collateral is produced as long as it is produced cheaply.[iv] The self-reinforcing and self-organising aspects of the system are evident and have resulted in a natural bias to politics, where the disinterest displayed by finance to workers is mimicked by the disdain with which the politicians view the voters, since it is less votes than money that makes possible the acquisition of the valuable franchises that are represented by seats in Parliament or Congress. How else is one to understand the purchase of a mayoralty in New York by a billionaire whose fortune came from the marketing of a mediocre market information system or a Senator’s seat by an executive from Goldman Sachs? This is not an electoral system so much as a system for marketing tax farms to the highest bidder.

911

Indeed, wherever one looks, one finds systems that are increasingly dominated by fewer and fewer major nodes. The consequence of the failure of one or more of those nodes would be a massive increase in volatility. It is no wonder that Wall Street economists don’t know which end is up; they are trying to do the impossible, predicting short term outcomes against a backdrop of massive uncertainty and a vested interest in the status quo.

The truth of the matter is that “globalisation” has brought us to a point where almost any event could initiate a cascade of consequences beyond the control of even the legendary Greenspan and the Exchange Stabilisation Fund. 911 may well have been that event. Economically, it wrecked the attempts that were underway at the time to investigate and control the rampant fraud and abuse that had resulted in the collapse of the government’s accounting and financial control systems and it has resulted in a runaway spending spree and balance of payments catastrophe. Politically, it wrecked any serious attempt to negotiate a viable compromise in the Middle East. Militarily it has exposed grave weakness at the heart of the American war machine. Morally, its consequences have revealed the absence of any ethical foundation to the so-called New World Order and the absence of a framework of law to order it.

About the only thing that doesn’t seem widely exposed is exactly who was responsible for 911 itself.[v] But the answer to that question is hiding in plain sight. When a few more people see it, we expect the cascade to begin in earnest. Revolutions have started from much less.

Chris

Sanders

csanders@sandersresearch.com

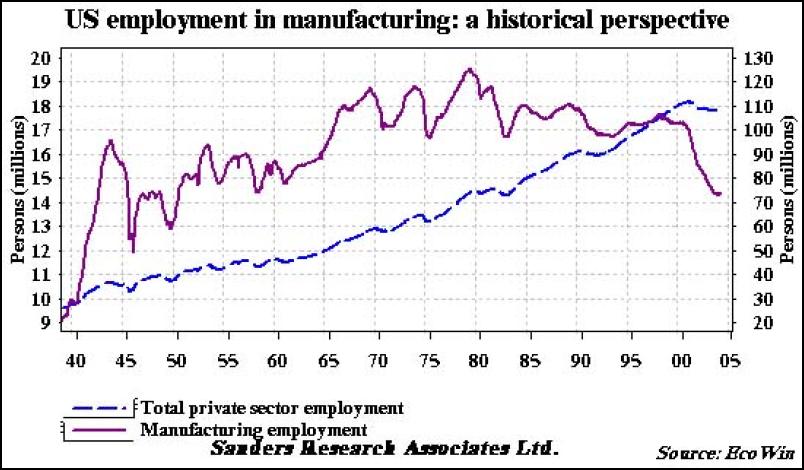

[i] The decline in manufacturing jobs has been precipitous in the last four years. This is not business as usual; it represents a major change in the structure of the US economy, and can be traced to 1970, the defeat in Vietnam, and the collapse of the Bretton Woods system. The ascendancy of the finance sector in the US can be traced to the latter development, as increased volatility in interest rates and foreign exchange markets disrupted the production sector.

Click for big version

[ii] It is important to note that specialisation such as this has nothing whatsoever to do with competitive advantage in the sense that the term was used by Adam Smith. Taiwan has no special endowment that makes it a better place to manufacture semiconductors. The competitive “advantage” that such countries display is a desirable labour force; desirable because it is cheaper than comparable labour at home.

[iii] See Albert- László Barabási (2002) Linked, Cambridge Massachusetts, Perseus Publishing ISBN 0-7832-0667-9 for an excellent discussion of ordered versus random networks.

[iv] For a detailed case study of the consequences of a systemic bias in favour of finance over production see Sanders Research Associates Ltd. Piracy on the Delaware by Paul Atkinson. It is the story of the dismemberment of Sun Shipbuilding, one of America’s premier industrial companies.

[v] Read Blowback from the blowhards (2), Sanders Research Associates, Not important? Think again, May 22, 2004.

STANDARD

DISCLAIMER FROM UQ.ORG: UnansweredQuestions.org does not

necessarily endorse the views expressed in the above

article. We present this in the interests of research -for

the relevant information we believe it contains. We hope

that the reader finds in it inspiration to work with us

further, in helping to build bridges between our various

investigative communities, towards a greater, common

understanding of the unanswered questions which now lie

before us.

Richard S. Ehrlich: Deadly Border Feud Between Thailand & Cambodia

Richard S. Ehrlich: Deadly Border Feud Between Thailand & Cambodia Gordon Campbell: On Free Speech And Anti-Semitism

Gordon Campbell: On Free Speech And Anti-Semitism Ian Powell: The Disgrace Of The Hospice Care Funding Scandal

Ian Powell: The Disgrace Of The Hospice Care Funding Scandal Binoy Kampmark: Catching Israel Out - Gaza And The Madleen “Selfie” Protest

Binoy Kampmark: Catching Israel Out - Gaza And The Madleen “Selfie” Protest Ramzy Baroud: Gaza's 'Humanitarian' Façade - A Deceptive Ploy Unravels

Ramzy Baroud: Gaza's 'Humanitarian' Façade - A Deceptive Ploy Unravels Keith Rankin: Remembering New Zealand's Missing Tragedy

Keith Rankin: Remembering New Zealand's Missing Tragedy{kind=link}