Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

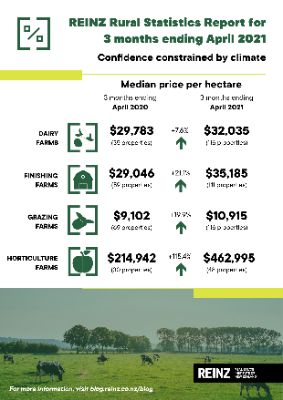

Confidence Constrained By Climate

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 220 more farm sales (+89.4%) for the three months ended April 2021 than for the three months ended April 2020. Overall, there were 466 farm sales in the three months ended April 2021, compared to 432 farm sales for the three months ended March 2021 (+7.9%), and 246 farm sales for the three months ended April 2020.

1,677 farms were sold in the year to April 2021, 45.1% more than were sold in the year to April 2020, with 120.0% more Dairy farms, 84.1% more Dairy Support, 20.8% more Grazing farms, 54.4% more Finishing farms and 11.8% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to April 2021 was $29,746 compared to $22,435 recorded for three months ended April 2020 (+32.6%). The median price per hectare increased 14.8% compared to March 2021.

The REINZ All Farm Price Index decreased 2.4% in the three months to April 2021 compared to the three months to March 2021. Compared to the three months ending April 2020 the REINZ All Farm Price Index rose 3.1%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

All 13 regions recorded an increase in the number of farm sales for the three months ended April 2021 compared to the three months ended April 2020, with the most notable being Waikato (+61) and Northland (+27). Wellington recorded the smallest increase in sales (+3). Compared to the three months ended March 2021, seven regions recorded an increase in sales, the most notable being Waikato (+13) and both Otago and Southland (+7).

Brian Peacocke, Rural Spokesman, at REINZ says: “Sales figures for the 3 month period ending 30 April continue to reflect the strength and resilience of the rural economy with the majority of categories registering significant increases in volumes for the 12 month period just ended versus the preceding 12 month period.

“Improving product prices, particularly for the dairy and horticulture sectors are part of the story but of equal significance is the fact that after several years of boardroom-induced restrictions, most banks have for the last six months been coming back into the rural market.

“The mix of this support, backed up by a low interest rate regime, has assisted in a positive way, purchasing decisions for those farmers with the necessary performance and equity credentials to expand their operations, and where the opportunity has been available, to acquire additional land.

“Equally, such increased activity, which has applied to the pastoral, horticultural and forestry sectors, has allowed a number of older landowners to either bring equity partners into their operations, or in many cases, to exit their respective sectors altogether.

“COVID-19 continues to be an issue in some parts of the supply chain, particularly at the point of cargo discharge, but the mix of careful planning and innovation has allowed most sectors to deal with such issues reasonably successfully.

“Regretfully however, some of the eastern regions of both the North and South Island have been impacted heavily by drought conditions, and whilst many other regions have enjoyed excellent spring and autumn growing conditions, the overall shortage of rain across the country has resulted in diminishing supplies of surface water as well as that in the underground aquifer.

“Labour and compliance issues aside, water in all its components, quality and quantity, is one of the major issues currently facing the rural sector, and for that matter, most of the urban centres throughout the country”, he concludes.

Points of Interest around New Zealand include:

- Northland/Auckland - Solid results in the Northland dairy and grazing sectors, as well as ongoing activity in the dairy support, finishing and horticultural sectors, with availability limiting the former and water supplies limiting the latter; the trend of lesser quality land going to forestry continues, as does the expansion of the kiwifruit and avocado industries; a distinct easing of activity across the board within the Auckland region

- Waikato/Bay of Plenty/Rotorua/King Country - A continuation of good activity in the dairy and finishing sectors throughout the Waikato, with ongoing results in the arable, dairy support and grazing categories, availability of properties and the later part of the season being the limiting factors; reports of strong forestry activity on the southwestern side of the region; quieter in the Waitomo and Taupo districts; lighter activity in the Bay of Plenty albeit very strong results on those few horticultural blocks available; generally quiet in the Rotorua, Whakatane and Opotiki districts

- Gisborne/Hawke’s Bay - Reduced activity in Gisborne and medium to light results across dairy support, finishing, grazing and horticultural properties in Hawke’s Bay where dry autumn conditions are an ongoing frustration for the farming community

- Taranaki - a shortage of property has constrained activity but good inquiry and steady results for those few farms that did venture onto the market

- Wanganui/Manawatu/Tararua - Multi-offer situations in much of the western districts were a reflection of a shortage of available property, but concerns regarding water consents is constraining activity in the dairy support sector; consistent results in the steady Tararua district where forestry interests continue to maintain a focus on the market; demand currently exceeds supply in all categories

- Wairarapa/Wellington - Minimal sales during the last month but dairy farmers are back in the market where the opportunity arises in the Wairarapa; sheep and beef farmers have begun challenging forestry interests for land purchases in the pastoral sector

- Nelson/Marlborough - Strong demand across the diverse range of land uses within the region with activity constrained by the shortage of supply; solid results on those finishing, grazing, horticulture and forestry properties which were available

- Canterbury/West Coast - Whilst the climate throughout the eastern districts has been severely dry, activity has nevertheless been solid across the arable, dairy, dairy support, finishing and grazing sectors; bank support is evident for qualified purchasers with multiple cash offers being made for a limited supply of property; the majority of the activity has centered around Ashburton, Timaru, Mackenzie and Waimate districts; good activity and results on dairy units in particular on the West Coast

- Otago - Increased interest stimulated by qualified bank involvement has resulted in a good run of sales of dairy, arable, finishing and grazing properties throughout the region, albeit a shortage of listings has been a constraint; Waitaki, Dunedin and Clutha districts have been the predominant beneficiaries of this activity

- Southland - With the benefit of one of the best autumns for years, Southland has experienced a very good run of sales across the region, with good results at increased prices for dairy units and strong activity on grazing properties in particular; evidence of forestry interests being prepared to pay more for good land then some pastoral farmers are prepared to pay; the increase in prices is being attributed in part to the shortage of supply across the province, but also to an improving degree of confidence within the rural sector.

Grazing and Dairy farms accounted for the largest number of sales, both with a 25% share of all sales over the three months to April 2021, Finishing farms accounted for 24%, and Horticulture accounted for 10% of all sales. These four property types accounted for 85% of all sales during the three months ended April 2021.

Dairy Farms

For the three months ended April 2021, the median sales price per hectare for dairy farms was $32,035 (116 properties), compared to $32,035 (104 properties) for the three months ended March 2021, and $29,783 (35 properties) for the three months ended April 2020. The median price per hectare for dairy farms has increased 7.6% over the past 12 months. The median dairy farm size for the three months ended April 2021 was 130 hectares.

On a price per kilo of milk solids basis the median sales price was $34.45 per kg of milk solids for the three months ended April 2021, compared to $34.49 per kg of milk solids for the three months ended March 2021 (-0.1%), and $32.97 per kg of milk solids for the three months ended April 2020 (+4.5%).

The REINZ Dairy Farm Price Index rose 1.2% in the three months to April 2021 compared to the three months to March 2021. Compared to April 2020, the REINZ Dairy Farm Price Index rose 13.8%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended April 2021, the median sale price per hectare for finishing farms was $35,185 (111 properties), compared to $35,185 (109 properties) for the three months ended March 2021, and $29,046 (59 properties) for the three months ended April 2020. The median price per hectare for finishing farms has increased 21.1% over the past 12 months. The median finishing farm size for the three months ended April 2021 was 38 hectares.

Grazing Farms

For the three months ended April 2021, the median sales price per hectare for grazing farms was $10,915 (116 properties), compared to $11,249 (124 properties) for the three months ended March 2021 and $9,102 (69 properties) for the three months ended April 2020. The median price per hectare for grazing farms has increased 19.9% over the past 12 months. The median grazing farm size for the three months ended April 2021 was 143 hectares.

Horticulture Farms

For the three months ended April 2021, the median sales price per hectare for horticulture farms was $462,995 (48 properties), compared to $427,218 (42 properties) for the three months ended March 2021 and $214,942 (30 properties) for the three months ended April 2020. The median price per hectare for horticulture farms has increased 115.4% over the past 12 months. The median horticulture farm size for the three months ended April 2021 was six hectares.

Raise Communications: NZ Careers Expo Kicks Off National Tour Amid Record Unemployment

Raise Communications: NZ Careers Expo Kicks Off National Tour Amid Record Unemployment Hugh Grant: How To Build Confidence In The Data You Collect

Hugh Grant: How To Build Confidence In The Data You Collect Tourism Industry Aotearoa: TRENZ 2026 Set To Rediscover Auckland As It Farewells Rotorua - The Birthplace Of Tourism

Tourism Industry Aotearoa: TRENZ 2026 Set To Rediscover Auckland As It Farewells Rotorua - The Birthplace Of Tourism NIWA: Students Representing New Zealand At The ‘Olympics Of Science Fairs’ Forging Pathway For International Recognition

NIWA: Students Representing New Zealand At The ‘Olympics Of Science Fairs’ Forging Pathway For International Recognition Coalition to End Big Dairy: Activists Protest NZ National Dairy Industry Awards Again

Coalition to End Big Dairy: Activists Protest NZ National Dairy Industry Awards Again Infoblox: Dancing With Scammers - The Telegram Tango Investigation

Infoblox: Dancing With Scammers - The Telegram Tango Investigation