Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

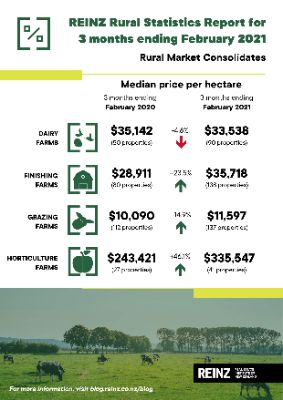

Rural Market Consolidates

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 129 more farm sales (+39.2%) for the three months ended February 2021 than for the three months ended February 2020. Overall, there were 458 farm sales in the three months ended February 2021, compared to 517 farm sales for the three months ended January 2021 (-11.4%), and 329 farm sales for the three months ended February 2020.

1,542 farms were sold in the year to February 2021, 23.1% more than were sold in the year to February 2020, with 51.3% more Dairy farms, 3.1% more Grazing farms, 42.9% more Finishing farms and 30.1% less Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to February 2021 was $25,665 compared to $20,569 recorded for three months ended February 2020 (+24.8%). The median price per hectare decreased 0.8% compared to January 2021.

The REINZ All Farm Price Index decreased 1.0% in the three months to February 2021 compared to the three months to January 2021. Compared to the three months ending February 2020 the REINZ All Farm Price Index rose 7.4%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Ten of the 14 regions recorded an increase in the number of farm sales for the three months ended February 2021 compared to the three months ended February 2020, with the most notable being Waikato (+27) and Auckland (+24). Gisborne and Wellington recorded the most notable decline in sales (-5). Compared to the three months ended January 2021, two regions recorded an increase in sales, namely Southland and Waikato ( +1).

Brian Peacocke, Rural Spokesman, at REINZ says: “Sales figures for the 3-month period ending February 2021 confirm the rural market is in good shape with dairy farm sales holding well followed closely by those in the finishing and grazing sectors.

“Of particular note are the encouraging signals emerging from the world marketplace for dairy produce which in turn is being translated into an increasing payout to the dairy farmers. The increased cashflow from this sector alone will have significant benefits for the New Zealand economy.

“Sales of finishing and grazing properties reflect the commitment from those sectors to explore every possibility in the marketplace in spite of serious supply chain issues, with the resultant increasing demand and sustainability of land values of properties within those sectors reflecting an underlying and seemingly sustainable degree of confidence.

“Activity is gearing up within the horticulture sector as the kiwifruit industry prepares for a bumper harvest, with the availability of reefer shipping helping to overcome the difficulties of transportation to the market due to the extreme shortage of containers.

“Regrettably, with the impact of COVID-19 restricting the availability of labour from off-shore under the Regional Seasonal Employer (RSE) Scheme, the shortage of labour is having a dramatic impact across the horticultural sector with considerable amounts of export potential produce not being able to be harvested, the pip fruit industry being a particular, albeit not isolated, case in point,” he concludes.

Activity within the rural market around New Zealand includes the following: -

- Northland/Auckland - an improved number of dairy farm sales in the Far North District, albeit lower priced, with a steady sprinkling of finishing and grazing farm sales stretching down into the Whangarei and Kaipara Districts; a healthy number of finishing farm transactions at strong prices in the lower North particularly in the Rodney District

- Waikato/King Country - a resurgence in dairy farm sales, predominantly in the Waikato and Waipa districts, backed up by a strong level of finishing property sales at healthy prices; lighter activity on grazing units throughout the region but dairy support and finishing units gained solid traction in the Waitomo and Taupo districts

- Bay of Plenty/Rotorua - a good cross-section of sales in most categories with horticultural properties dominating the Western Bay of Plenty; Whakatane and Opotiki districts experienced reasonable results compared to a quieter time in the Rotorua district which had only one finishing block sale

- Gisborne/Hawke’s Bay - strong prices albeit reduced numbers with one smaller finishing block being the feature in the Gisborne district; acceptable results in the Hawke’s Bay where sales of grazing units dominated

- Taranaki - solid prices achieved for dairy and finishing properties in the New Plymouth and South Taranaki districts

- Wanganui/Manawatu/Tararua - quiet in the northern localities with steady prices paid for a range of finishing and grazing properties in the Manawatu, Tararua and Horowhenua districts

- Wairarapa/Wellington - calm conditions prevailed over much of the southern sector with registrable activity only in the grazing and dairy categories

- Nelson/Marlborough - encouraging results in the northern segment of the South Island with finishing properties at steady prices dominating the other forms of land use

- Canterbury/West Coast - a good level of activity on finishing and grazing units at solid prices in the Hurunui and Waimakariri districts; similar results in the Selwyn and Timaru regions but quiet in the Ashburton locality; reasonable activity across the board on grazing, finishing and dairy support properties on the West Coast

- Otago - well spread activity in all districts with current prices holding for dairy, finishing and grazing properties; one standout transaction involved a small pinot noir vineyard at Bannockburn in Central Otago

- Southland - strong activity within the Southland district specifically with healthy prices being paid for a good range of dairy, finishing and grazing properties.

Finishing farms accounted for the largest number of sales with a 30% share of all sales over the three months to February 2021, Grazing farms accounted for 30%, Dairy accounted for 20% and Horticulture accounted for 9% of all sales. These four property types accounted for 89% of all sales during the three months ended February 2021.

Dairy Farms

For the three months ended February 2021, the median sales price per hectare for dairy farms was $33,538 (90 properties), compared to $33,444 (91 properties) for the three months ended January 2021, and $35,142 (50 properties) for the three months ended February 2020. The median price per hectare for dairy farms has decreased 4.6% over the past 12 months. The median dairy farm size for the three months ended February 2021 was 132 hectares.

On a price per kilo of milk solids basis the median sales price was $35.48 per kg of milk solids for the three months ended February 2021, compared to $34.78 per kg of milk solids for the three months ended January 2021 (+2.0%), and $35.29 per kg of milk solids for the three months ended February 2020 (+0.5%).

The REINZ Dairy Farm Price Index rose 1.1% in the three months to February 2021 compared to the three months to January 2021. Compared to February 2020, the REINZ Dairy Farm Price Index rose 5.9%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended February 2021, the median sale price per hectare for finishing farms was $35,718 (138 properties), compared to $34,699 (156 properties) for the three months ended January 2021, and $28,911 (80 properties) for the three months ended February 2020. The median price per hectare for finishing farms has increased 23.5% over the past 12 months. The median finishing farm size for the three months ended February 2021 was 37 hectares.

Grazing Farms

For the three months ended February 2021, the median sales price per hectare for grazing farms was $11,597 (137 properties), compared to $11,472 (146 properties) for the three months ended January 2021 and $10,090 (112 properties) for the three months ended February 2020. The median price per hectare for grazing farms has increased 14.9% over the past 12 months. The median grazing farm size for the three months ended February 2021 was 127 hectares.

Horticulture Farms

For the three months ended February 2021, the median sales price per hectare for horticulture farms was $355,547 (41 properties), compared to $308,960 (53 properties) for the three months ended January 2021 and $243,421 (27 properties) for the three months ended February 2020. The median price per hectare for horticulture farms has increased 46.1% over the past 12 months. The median horticulture farm size for the three months ended February 2021 was 6 hectares.

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts 2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change?

Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change? Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?

Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?