Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

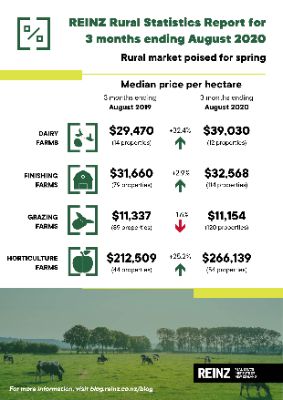

Rural Market Poised For Spring

Data released today by the Real Estate Institute of New Zealand (REINZ) shows there were 121 more farm sales (+45.7%) for the three months ended August 2020 than for the three months ended August 2019. Overall, there were 386 farm sales in the three months ended August 2020, compared to 341 farm sales for the three months ended July 2020 (+13.2%), and 265 farm sales for the three months ended August 2019. 1,252 farms were sold in the year to August 2020, 7.2% fewer than were sold in the year to August 2019, with 22.9% less Dairy farms, 14.1% less Grazing farms, 15.3% less Finishing farms and 6.1% more Arable farms sold over the same period.

The median price per hectare for all farms sold in the three months to August 2020 was $25,657 compared to $25,346 recorded for three months ended August 2019 (+1.2%). The median price per hectare increased 10.8% compared to July 2020.

The REINZ All Farm Price Index increased 2.9% in the three months to August 2020 compared to the three months to July 2020. Compared to the three months ending August 2019 the REINZ All Farm Price Index fell 4.3%. The REINZ All Farm Price Index adjusts for differences in farm size, location, and farming type, unlike the median price per hectare, which does not adjust for these factors.

Twelve of the 14 regions recorded an increase in the number of farm sales for the three months ended August 2020 compared to the three months ended August 2019, with the most notable being Canterbury (+24) and Manawatu/Wanganui (+21). Bay of Plenty recorded the most substantial decline in sales (-3) followed by Nelson (-1). Compared to the three months ended July 2020, 10 regions recorded an increase in sales with the biggest increases being in Otago (+12) and Canterbury (+11).

Brian Peacocke, Rural Spokesman, at REINZ says: “Sales data for the 3-month period ending August 2020 is positive with total farms sold (386) being at the strongest level since the equivalent period in 2016 (393).

“The charts below demonstrate interesting comparisons for both volume and price in the two periods referred to: -

| Sales Numbers | Aug 2016 | Aug 2020 |

| Dairy | 14 | 12 |

| Finishing | 75 | 114 |

| Grazing | 158 | 120 |

| Arable | 36 | 20 |

| Horticulture | 77 | 54 |

| Forestry | 18 | 17 |

| Median Prices per hectare | Aug 2016 | Aug 2020 |

| Dairy | $ 40,469 | $ 39,030 |

| Finishing | $ 27,208 | $ 32,568 |

| Grazing | $ 15,326 | $ 11,154 |

| Arable | $ 54,895 | $ 33,473 |

| Horticulture | $ 190,338 | $ 266,139 |

| Forestry | $ 9,882 | $ 7,769 |

“Seasonal issues such as weather, feed, water, compliance, product prices, availability of finance, interest rates and the health status of the nation remain constant in the rural market, while resilience remains the dominant factor,” he concludes.

Points of Interest around New Zealand include:

- Northland/Auckland - intermittent activity in the upper North covering dairy (1), strong pricing on finishing (2) and horticulture (1) units plus several grazing properties (4) at current rates; a similar smattering of results throughout the Auckland region covering finishing, grazing, horticulture and arable properties

- Waikato/King Country - good strong results on finishing properties in the Hauraki and Waikato districts, with the strength of that activity carrying on into the Waipa and South Waikato districts; very quiet in the northern King Country and Taupo

- Bay of Plenty/Rotorua - solid sales of predominantly smaller avocado orchards plus a deer unit in the wider Tauranga area with good prices paid for an arable and a finishing unit in the Whakatane district; no farm sales in the Rotorua district

- Gisborne/Hawke’s Bay - several horticulture sales in Gisborne; light activity in Hawke’s Bay apart from several finishing and grazing properties at good prices in the Hastings and the Waipawa/Waipukurau districts

- Taranaki - a flurry of sales of finishing, dairy support and grazing properties at good prices throughout the New Plymouth and Stratford localities, with one smaller dairy unit sale in South Taranaki

- Wanganui/Manawatu - a burst of activity at good solid prices for dairy, dairy support and finishing units in the central Manawatu and Feilding locations; a quiver of activity in the Ruapehu district but a spectacular array of strong results on dairy support, dairy and grazing properties in the Tararua region, particularly around Pahiatua and Dannevirke districts

- Wairarapa/Wellington - an interesting spread of sales covering arable, dairy support and finishing properties at good prices predominantly in the South Wairarapa, with Upper Hutt gaining a solitary mention with one grazing unit sale

- Nelson/Marlborough - no farm sales recorded in the Tasman region but an excellent explosion of sales of mainly sauvignon blanc vineyards in the Marlborough district

- Canterbury/West Coast - good results recorded across Canterbury with a cluster of grazing sales in the Hurunui district; a dairy unit and several finishing units in the Waimakariri region backed up by similar results in the Selwyn district; a cluster of strongly priced finishing and arable properties within reasonable proximity to Ashburton backed up by reasonable activity in the Timaru district; West Coast raised the flag with activity in the grazing and forestry sectors

- Otago - great results across the board for finishing and grazing properties at good strong prices throughout the Waitaki and Central Otago districts with a similar pattern of activity on finishing, dairy support and grazing properties in the Dunedin and Clutha locations

- Southland - flying the flag again with a good range of results at steady prices for dairy, arable, finishing and grazing properties centered around the Southland and Gore districts; quiet in the deep south around Invercargill.

Grazing farms accounted for the largest number of sales with a 31% share of all sales over the three months to August 2020, Finishing farms accounted for 30%, Dairy accounted for 3% and Horticulture accounted for 14% of all sales. These four property types accounted for 78% of all sales during the three months ended August 2020.

Dairy Farms

For the three months ended August 2020, the median sales price per hectare for dairy farms was $39,030 (12 properties), compared to $23,193 (18 properties) for the three months ended July 2020, and $29,470 (14 properties) for the three months ended August 2019. The median price per hectare for dairy farms has increased 32.4% over the past 12 months. The median dairy farm size for the three months ended August 2020 was 113 hectares.

On a price per kilo of milk solids basis the median sales price was $31.60 per kg of milk solids for the three months ended August 2020, compared to $32.50 per kg of milk solids for the three months ended July 2020 (-2.8%), and $31.11 per kg of milk solids for the three months ended August 2019 (+1.6%).

The REINZ Dairy Farm Price Index rose 8.5% in the three months to August 2020 compared to the three months to July 2020. Compared to August 2019, the REINZ Dairy Farm Price Index fell 8.7%. The REINZ Dairy Farm Price Index adjusts for differences in farm size and location compared to the median price per hectare, which does not adjust for these factors.

Finishing Farms

For the three months ended August 2020, the median sale price per hectare for finishing farms was $32,568 (114 properties), compared to $31,049 (101 properties) for the three months ended July 2020, and $31,660 (79 properties) for the three months ended August 2019. The median price per hectare for finishing farms has risen 2.9% over the past 12 months. The median finishing farm size for the three months ended August 2020 was 33 hectares.

Grazing Farms

For the three months ended August 2020, the median sales price per hectare for grazing farms was $11,154 (120 properties), compared to $10,194 (105 properties) for the three months ended July 2020 and $11,337 (89 properties) for the three months ended August 2019. The median price per hectare for grazing farms has fallen 1.6% over the past 12 months. The median grazing farm size for the three months ended August 2020 was 113 hectares.

Horticulture Farms

For the three months ended August 2020, the median sales price per hectare for horticulture farms was $266,139 (54 properties), compared to $289,632 (46 properties) for the three months ended July 2020 and $212,509 (44 properties) for the three months ended August 2019. The median price per hectare for horticulture farms has risen 25.2% over the past 12 months. The median horticulture farm size for the three months ended August 2020 was 8 hectares.

Parrot Analytics: A Very Parrot Analytics Christmas, 2024 Edition

Parrot Analytics: A Very Parrot Analytics Christmas, 2024 Edition Financial Markets Authority: Individual Pleads Guilty To Insider Trading Charges

Financial Markets Authority: Individual Pleads Guilty To Insider Trading Charges Great Journeys New Zealand: Travel Down Memory Lane With The Return Of The Southerner

Great Journeys New Zealand: Travel Down Memory Lane With The Return Of The Southerner WorkSafe NZ: Overhead Power Lines Spark Safety Call

WorkSafe NZ: Overhead Power Lines Spark Safety Call Transpower: Transpower Seeks Feedback On Electricity Investment Short-list For Upper South Island

Transpower: Transpower Seeks Feedback On Electricity Investment Short-list For Upper South Island Commerce Commission: “Cheating The System” – Sentencing In Country’s First Criminal Cartel Case

Commerce Commission: “Cheating The System” – Sentencing In Country’s First Criminal Cartel Case