Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

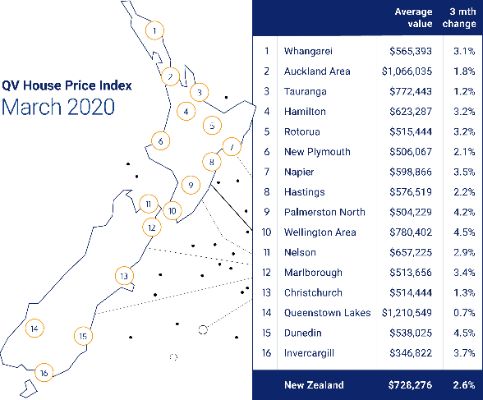

COVID-19 – Where Does The Housing Market Go From Here?

The latest QV House Price Index data for March provides us with a view of the housing market as New Zealand headed into lockdown on 25th March. But what it doesn’t tell us is what happens beyond the proverbial brick wall that the Covid-19 lockdown has created.

The data shows the property market was continuing to perform strongly throughout early-mid March with all 16 of the major cities we monitor showing quarterly value growth for the fourth consecutive month, indicating strength right across the country.

The average value nationally increased 6.1% year on year and the average value is currently sitting at $728,276. This represents an increase of 2.6% over the past three months, the same quarterly growth as last month. The average value in the Auckland Region sits at $1,066,035, up 1.8% over the last quarter, and up 2.5% year on year.

QV General Manager David Nagel said “The housing market was ticking along nicely leading up to lockdown, although in the final week we could see the impacts of uncertainty starting to have an effect. Real estate agents and developers were rushing to get homes listed in anticipation of a change in the playing field. But purchasers were less bullish and less willing to commit as the market was heading into unchartered territory. Then everything changed on 25th March”.

“Nobody knows what post-lockdown market conditions will look like. We’ve never been through anything remotely like this. We also do not know how long this will last. What we do know is there will still be a property market. There will still be sellers, although likely only a fraction of what we’re used to. And there will still be buyers that have the means and confidence to purchase property”, he says.

“What happens to house prices beyond this point will be determined by market forces and the changes in supply and demand” says Mr Nagel.

Up to this point we were seeing multiple buyers often with plentiful funds available, competing for tightly held stock. Going forward supply of houses for sale will likely be reduced. The pipeline for new builds has been impacted as has almost every other industry during lockdown. Most New Zealanders will look to consolidate their position in their current home as the country works its way out of a forecast recession. Selling an existing property and upgrading to a different home will likely be furthest from their mind. Although some may be forced to downsize or even relocate to a new city in order to gain employment.

But banks will be patient, particularly in the short term with a multitude of other, softer options available like mortgage holidays, to avoid a flood or forced sales.

Demand for buying a house will also likely be down significantly. First home buyers that were active prior to lockdown may have lost some buying power with both their investment savings and Kiwisaver accounts taking a hit. Their house deposit and employment status may look quite different after lockdown ends, delaying their entry into the market.

Others that have fared better under lockdown may see this as an opportunity, while interest rates are low, to dominate what’s left of the market. With many first home buyers no longer competing, plus a likely post-lockdown slashing of net migration numbers no longer feeding housing demand, we could see a buyers’ market develop.

“Multi-unit developments currently under construction will be completed after the lockdown ends, but contract settlements could be impacted by sunset clauses within some purchase contracts. That effectively puts a time limit on the contract's validity, which could come into play depending on the length of the lockdown. Developers will take a cautious approach to new projects and will be revisiting the viability of each development based on new selling levels”, he says.

“What’s most likely is we will see transaction volumes drop significantly from pre-lockdown levels. House listings will dry up with only those having to sell, for work or financial reasons, wanting to enter an uncertain market”, says Mr Nagel.

“Buyers that have the means will likely dominate the market, but with limited stock available buyers will probably exercise patience and this could force prices down for vendors that simply have to sell. But by how much? Nobody knows”, he says.

“The market will take considerable time to settle to a new normal after the lockdown ends. There will be pre-lockdown transaction settlements that will occur, plus a very limited number of transactions that occurred during lockdown. But with limited transactions after lockdown ends, we can expect a market filled with uncertainty at least through to the end of 2020 as the economy finds its feet again”, he says.

Auckland

The Auckland area saw values increase 2.5% year on year and 1.8% over the last quarter. The average house is valued at $1,066,035.

Within Auckland, houses in the Rodney area experienced 3.3% quarterly growth while North Shore values went up 2.6% followed by Waitakere at 2.4% and Manukau at 2.3%. Values in the Papakura area went down very slightly by 0.1% over the three month period.

Annual growth painted a different picture with Papakura leading the way at 3.5% growth, followed by Manukau at 3.4% and Waitakere at 3.2%.

Tauranga

Modest value growth was seen in Tauranga with values increasing by 5.4% over the last twelve months and 1.2% over the last quarter. The average value is now $772,443.

Hamilton

Strong value growth was seen in Hamilton with values increasing by 7.4% over the last twelve months and 3.2% over the last quarter. The average value is now $623,287.

Wellington

Strong value growth was seen in Wellington region with values increasing by 11.0% over the last twelve months and 4.5% over the last quarter. The average value is now $780,402.

Value growth within Wellington region was relatively consistent with Hutt City leading the way with 17.2% annual growth and 5.5% quarterly increase to the end of March.

Nelson

Strong value growth was seen in Nelson with values increasing by 6.6% over the last twelve months and 2.9% over the last quarter. The average value is now $657,225.

Christchurch

Modest value growth was seen in Christchurch with values increasing by 3.4% over the last twelve months and 1.3% over the last quarter. The average value is now $514,444.

Dunedin

Very strong value growth was seen in Dunedin with values increasing by 19.2% over the last twelve months and 4.5% over the last quarter. The average value is now $538,025.

Provincial centres, North Island

Gisborne and South Waikato District to lead the way in quarterly growth to the end of March, both up 11.0%, followed by Opotiki on 10.3%. In annual growth, Horowhenua increased 27.2% followed by Kawerau on 23.8% and Rangitikei on 22.9%.

Provincial centres, South Island

Gore leads the South Island in quarterly growth, up 5.5%, followed by Central Otago 4.6% and Waimate District 3.8%. Invercargill leads the way in annual growth, up 19.4%, followed by Waimate 18.1% and Gore at 16.4%.

IAG New Zealand: New Zealand’s $64 Billion Spend On Natural Hazards Heavily Skewed To Recovery Over Resilience

IAG New Zealand: New Zealand’s $64 Billion Spend On Natural Hazards Heavily Skewed To Recovery Over Resilience Rail And Maritime Transport Union: Rail Workers Celebrate Hillside Workshops Rebirth

Rail And Maritime Transport Union: Rail Workers Celebrate Hillside Workshops Rebirth NZX: NZX Welcomes Changes To Prospective Financial Information

NZX: NZX Welcomes Changes To Prospective Financial Information Commerce Commission: Possible Cartel Conduct Sparks Compliance Advice

Commerce Commission: Possible Cartel Conduct Sparks Compliance Advice Mindful Money: Finalists For 5th Annual Ethical & Impact Investment Awards

Mindful Money: Finalists For 5th Annual Ethical & Impact Investment Awards The Reserve Bank of New Zealand: Examining Māori Access To Capital - Market Failures

The Reserve Bank of New Zealand: Examining Māori Access To Capital - Market Failures