Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Toughing it out in April

House sales lowest for an April month in five years,

the timing of Easter probably didn’t help.

Key points

The Housing market toughed it out in April, with sales down almost 12% compared to April last year. Sales across the country of 5,800 in April were the lowest in five years.

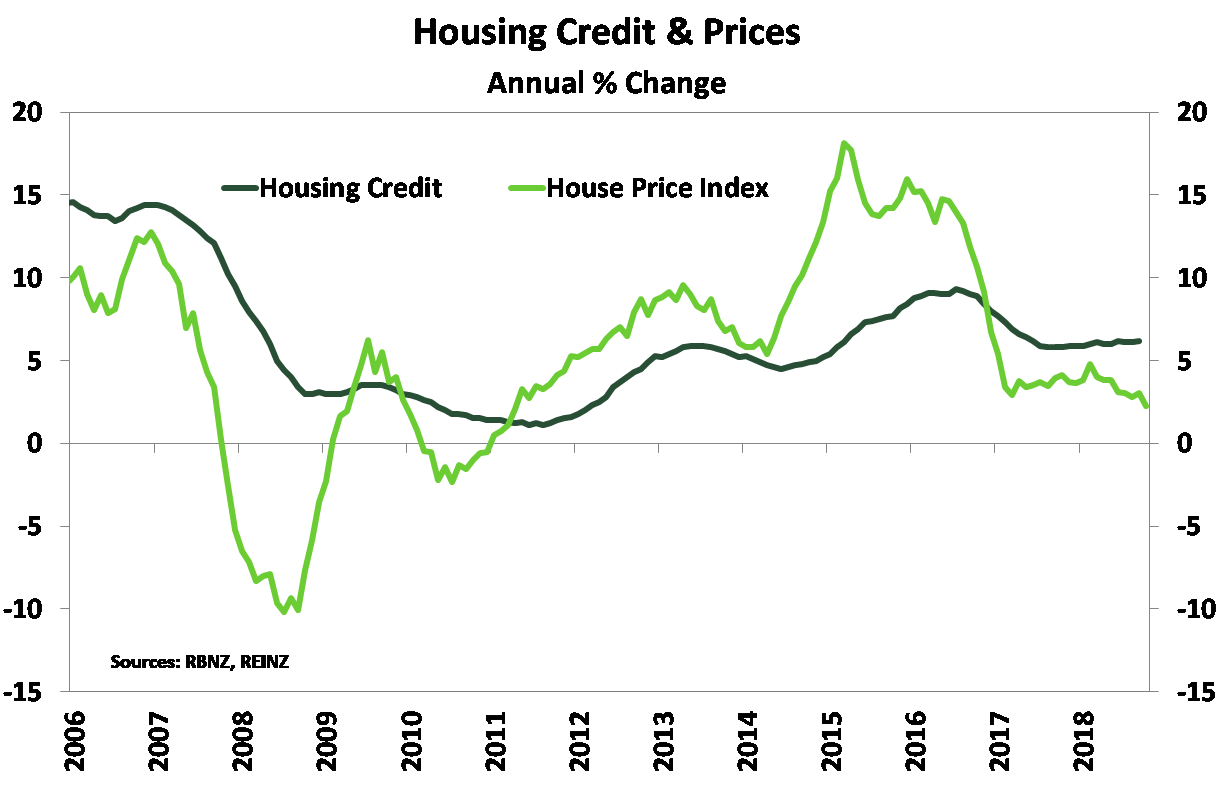

The House Price Index (HPI) was only 1.3%yoy higher, the lowest rise since August 2011. A majority of regions experienced a fall in the HPI over April, but especially those close to Auckland.

Major developments over the last month should help provide a floor under the market. These include the plug being pulled on a CGT and an interest rate cut being deliver by the RBNZ.

According to the REINZ April was another tough month in the housing market, particularly for Auckland. Sales nationally of 5,800 were down almost 12%yoy from April last year. And while Auckland sales took a tumble, outside of the City of Sails, sales also pulled back in April. The timing of Easter this year, close to ANZAC day may have played a roll, lowing the number of business days. Adding to the softness was a continued rise in the number of days to sell. Properties are taking longer to sell as buyers are under less pressure to get the deal done. National house price appreciation continued to ease, coming in at 1.3%yoy down 1%pt from March and was the lowest rate of annual price increase since late 2011.

Auckland is bearing the brunt of house price softness, down over 2%mom in April alone. Outside of Auckland the rate of annual house price rise pulled back, and a majority of regions experienced a monthly drop in prices – particularly the likes of Northland, Waikato and the Bay of Plenty being close to our largest city. Could this be a sign of contagion? It’s too early to tell, but the regions do tend to follow Auckland. Bucking the trend in prices were the Manawatū-Whanganui and Wellington regions. Supply of listed property is particularly low in the lower part of the North Island.

The current state of affairs in the housing market still does not suggest we are in for a sharp correction. Fundamentally, the economy is in reasonable health and we have a robust labour market – the unemployment rate is at 4.2%. In addition, there have been some key developments over the last month that takes away some of the pressure on the housing market and may help lift activity. First, the Government decided to abandon plans to introduce a Capital Gains Tax, this removes a key pillar of uncertainty for property investors and may encourage some to dip their toes back into the market. Last week the RBNZ cut the Official Cash Rate to a new low of 1.50%, which has seen banks respond with lower mortgage rates – although not as much as might have been expected. And we don’t think the RBNZ is done there. We expect the RBNZ will cut the OCR again this year, most likely in August. These developments may well put a floor under national house price appreciation.

Policy Implications

The degree of softness we have seen in the housing market has been somewhat surprising. If activity continues to fall, dragging prices with it, the RBNZ will likely be concerned. Last week’s OCR cut is expected to support spending in the economy, and if house prices don’t respond, household spending may suffer. Financial stability concerns have abated, with credit growth contained and this is a good thing. The RBNZ is likely to take a close look at macroprudential policy settings and potentially loosening them further. Investor-related lending is particularly soft.

ends

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change?

Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change? Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?

Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets? Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand

Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science Retail NZ: Retailers Call For Flexibility On Easter Trading Hours

Retail NZ: Retailers Call For Flexibility On Easter Trading Hours