Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Half year financial results: Kiwibank steps up momentum

9.30am Wednesday 20 February 2019

Media release

Kiwibank half year financial results for the six months ended 31 December 2018

Kiwibank steps up momentum

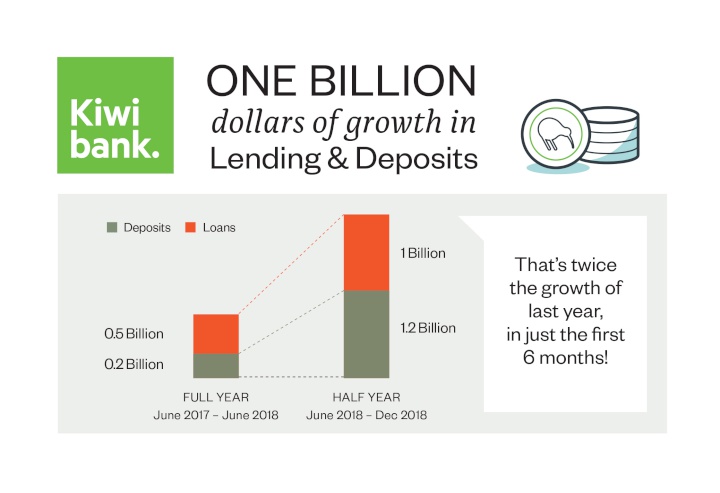

Kiwibank’s half-year results reveal the New Zealand-owned bank has hit one billion dollars in growth in both deposits and lending. In just six months it has achieved more than twice the growth for the full year prior.

“This momentum across the bank demonstrates Kiwibank’s objective to maintain a level of competition that benefits all Kiwis. New Zealanders are choosing to partner with Kiwibank and keep profits at home,” said Kiwibank CEO, Steve Jurkovich.

“We’ve helped more Kiwis into homes and have shown ourselves to be a market leader with consistent and competitive pricing.

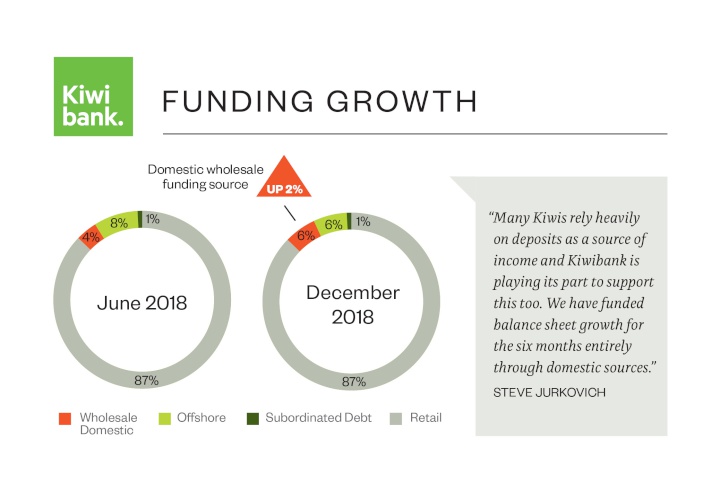

“Many Kiwis rely heavily on deposits as a source of income and Kiwibank is playing its part to support the savings and income goals of Kiwis. We have funded balance sheet growth for the six months entirely through domestic sources, providing Kiwis with competitive savings and investment opportunities,” Mr Jurkovich said.

“Kiwibank has a strong culture and high expectations of its people to do the right thing by customers. The current banking market is seeing unprecedented scrutiny around culture and conduct. We know that trust is central to customer relationships. We are crystal clear that conduct and compliance is not a project, a one-off initiative, or a static standard that is reached - it is about continual improvement and an unwavering attention to great customer outcomes over time. This determined focus on our customers will deliver a stronger and even more resilient Kiwibank for New Zealand,” Mr Jurkovich said.

For the half year ending 31 December 2018 the Kiwibank Banking Group, delivered a net profit after tax (NPAT) of $62 million up from $42 million for the six months ending 31 December 2017.

“Kiwibank is back to the performance levels it enjoyed before the Kaikoura earthquake and the abandoned technology project CoreMod,” Mr Jurkovich said.

“Kiwibank’s profits have always been modest in comparison to our Australian-owned competitors. We make an impact by returning profit to, and reinvesting in New Zealand. To maintain this momentum, we’ll continue to chip away at market share,” he promised.

“Our customers are getting a better deal than ever before. We have worked hard to simplify transactional fees and this value is illustrated in our results with net fees and other income down 20 percent year-on-year.”

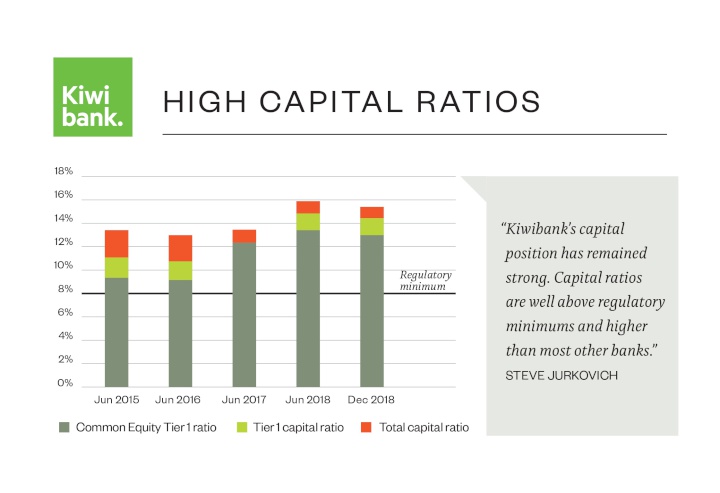

Kiwibank’s capital position has remained strong. Capital ratios are well above regulatory minima and higher than most other banks. During the six-month period, rating agency Standard & Poor’s moved Kiwibank credit rating outlook from ‘stable’ to ‘positive’.

“Capital adequacy is an area we need to consider when planning. We have now had time to digest the Reserve Bank’s capital review proposal. It creates more of an even playing field in several areas, like how capital requirements are calculated, but it is not without implications. We understand and support the Reserve Bank’s philosophy. It is in everyone’s interest to have a strong local banking system that is deeply invested in New Zealand and supports great customer outcomes. Kiwibank’s capital levels are currently significantly above regulatory requirements but we’ll need to continue to review this position over the transition period proposed.

“Another area of focus is our cost-to-income ratio. While an eight percent improvement is pleasing, looking forward, operating expenditure sitting at 67 percent of income is unsustainable. We are finding ways to improve efficiency and work smarter while better serving our customers.

“Kiwibank is ambitious by nature and heritage and we are committed to raising the impact we have for Kiwibank customers and New Zealand. The next stage in our evolution lies in technology transformation. It’s no longer about once-and-done or big-bang projects. Technology needs investment and Kiwibank will invest significantly in this critical capability.

“Changes to the branch network is another example of how we are adjusting to the impact technology is having on our lives, including customer preference. We acknowledge, and respect change is difficult for some customers and we that need to make sure we stay relevant by investing in the biggest positive impact for the most customers.

“While we are already overwhelmingly a digital bank, the face-to-face interactions we have with our customers are critical and at the heart of who we are. Kiwibank-only branches are all about delivering a better, dedicated and more relevant customer experience.

“Kiwibank is ideally positioned to be the SME bank for New Zealand. With increased investment in capability, we will deliver to the small and medium sized enterprises that make up the backbone of the New Zealand economy.

“Our size, ambition, and passion for New Zealand makes us the right partner and we are determined to support New Zealand customers more than ever before,” Mr Jurkovich concluded.

Other financial highlights:

• Net interest income (NII) is up 13 percent following strong lending growth and a recovery in net interest margin versus the corresponding prior year period.

• Net Interest Margin (NIM) 2.15 percent versus 2.00 percent for the corresponding prior year period.

• Asset quality remains high with impaired assets remaining low.

• Net loans and advances to customers up 7.2 percent on the prior comparative period.

• Customer deposits up 9.2 percent on the prior comparative period.

Notes to editors

Kiwibank Limited and subsidiaries (The Banking Group) is the major subsidiary of Kiwi Group Holdings Ltd, which in turn is owned by State Owned Enterprise New Zealand Post (53%), and Crown Entities New Zealand Super Fund (25%), and ACC (22%).

Kiwibank Banking Group financials for the

half-year ended 31 December 2018

| $m | 6 months to

31-Dec-18* | 6 months to

31-Dec-17* | 12 months to

30-Jun-18 |

| Interest income | 462 | 438 | 879 |

| Interest expense | (239) | (240) | (468) |

| Net interest income | 223 | 198 | 411 |

| Gains on financial instruments at fair value | 2 | 5 | 9 |

| Net fee & other income | 48 | 60 | 119 |

| Operating expenses | (183) | (197) | (373) |

| Impairment (losses)/reversals | (4) | (1) | (1) |

| Other impairment losses | - | (11) | (11) |

| Net profit before taxation | 86 | 54 | 154 |

| Income tax expense | (24) | (12) | (39) |

| Net profit after tax | 62 | 42 | 115 |

| Reconciliation of net profit after tax to underlying profit | |||

| Net profit after tax | 62 | 42 | 115 |

| Reconciling items (net of tax): | |||

| Other impairment losses1 | - | 8 | 8 |

| Operating costs incurred to wind down CoreMod2 | - | 7 | 7 |

| Net earthquake (recoveries)/costs3 | - | 1 | (4) |

| Underlying profit | 62 | 58 | 126 |

| Cost-to-income ratio | 67% | 75% | 69% |

| $m | As at

31-Dec 2018* | As at 31-Dec 2017* | As at 30 June 2018 |

| Assets | |||

| Loans and advances | 19,316 | 18,027 | 18,304 |

| Other assets | 2,724 | 2,354 | 2,411 |

| Total Assets | 22,040 | 20,381 | 20,715 |

| Liabilities | |||

| Deposits and other borrowings | 17,430 | 15,960 | 16,173 |

| Debt securities issued | 2,253 | 2,170 | 2,265 |

| Other liabilities | 829 | 831 | 790 |

| Total Liabilities | 20,512 | 18,961 | 19,228 |

| Equity | |||

| Share capital | 737 | 737 | 737 |

| Reserves | 791 | 683 | 750 |

| Total shareholder's equity | 1,528 | 1,420 | 1,487 |

| Total liabilities and shareholder's equity | 22,040 | 20,381 | 20,715 |

*Unaudited

1. Other impairment losses: Impairment loss recognised in relation to computer software (the CoreMod IT project)

2. Operating costs incurred to wind down CoreMod: Operating costs incurred in relation to the CoreMod IT project subsequent to the Board decision to close the project.

3. Net earthquake (recoveries)/costs: Earthquake costs are operating expenses incurred by the Group as a result of the November 2016 Kaikoura earthquake net of insurance receipts recognised to date.

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change?

Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change? Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?

Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets? Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand

Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science Retail NZ: Retailers Call For Flexibility On Easter Trading Hours

Retail NZ: Retailers Call For Flexibility On Easter Trading Hours