Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Smartphone Shipments, The Beginning of The End?

IDC MEDIA RELEASE: Smartphone Shipments, The Beginning of The End?

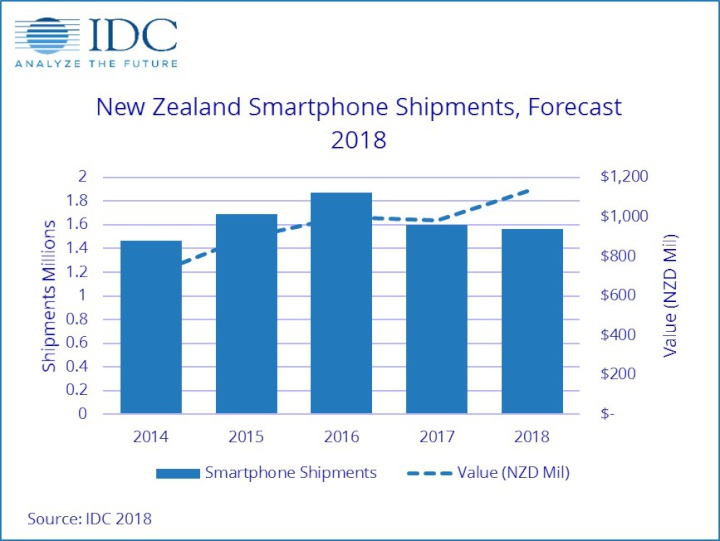

AUCKLAND, 1st March 2018: According to IDC’s recently published fourth-quarter mobile phone shipment results, tracked from October to December 2017, the New Zealand smartphone market has observed a full year on year shipment decline. This is this first time the New Zealand smartphone market has experienced a full year on year decline since IDC began tracking smartphone shipments in 2008.

1,602,000

smartphones were shipped in 2017, down 14.5% on the

1,874,000 shipped in 2016.

Chayse Gorton, Market

Analyst for IDC New Zealand, suggests "there are at least

three factors contributing to this decline: a saturated

market, a change in vendor strategy, and new features

failing to drive faster consumer upgrade cycles."

The smartphone market is saturated. IDC estimates 79% of consumers owned a smartphone in 2017, leaving a small number of consumers left to make the transition from feature phones to smartphones.

Many smartphone vendors appear to be increasing their focus on profitability, rather than chasing shipment volumes, through increasing the average selling prices of their devices. For example, the average selling price of smartphones for both Samsung and Apple, the two market leaders increased 14% YoY. Huawei, who may have been previously considered as a mid-range vendor introduced the Mate 10 Porsche edition in 2017, priced at over $2000 NZD.

IDC estimates that the average time a consumer holds on to their smartphone remains around 3 years, despite new features continuing to be introduced in the latest devices. Gorton believes, "New Zealand consumers do not refresh simply because a new feature has been introduced to a smartphone, instead they must feel that there is a significant benefit to be attained through upgrading." For example, many vendors have introduced some form of artificial intelligence, dual cameras, and reduced bezels, etc. into their devices, however, the benefits of such features do not yet appear to be adequately portrayed to consumers, and until they are, these features will drive limited upgrades.

Although IDC forecasts smartphone shipments to decline in 2018, revenue is set to increase. This will be primarily driven by an increased average selling price per device.

It is unlikely that this is the beginning of the end of smartphones, but considering the market’s many challenges, it is clear that vendors are already altering their strategies to continue to grow revenue in a saturated market.

Electricity Authority: Authority Confirms New Next-Gen Switching Service; Proposes Multiple Trading Relationships For Consumers

Electricity Authority: Authority Confirms New Next-Gen Switching Service; Proposes Multiple Trading Relationships For Consumers Mānuka Charitable Trust: Mānuka Charitable Trust Warns Global Buyers Of Misleading Australian Honey Claims

Mānuka Charitable Trust: Mānuka Charitable Trust Warns Global Buyers Of Misleading Australian Honey Claims  Engineering New Zealand: NZ Building System Needs Urgent Improvement

Engineering New Zealand: NZ Building System Needs Urgent Improvement GNS Science: Bioshields Could Help Slow Tsunami Flow

GNS Science: Bioshields Could Help Slow Tsunami Flow Transport and Infrastructure Committee: Inquiry Into Ports And The Maritime Sector Opened

Transport and Infrastructure Committee: Inquiry Into Ports And The Maritime Sector Opened Netsafe: Netsafe And Chorus Power Up Online Safety For Older Adults

Netsafe: Netsafe And Chorus Power Up Online Safety For Older Adults