Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Falling inventory creates struggle for stock as sellers wait

NEWS RELEASE 14 September 2016

Falling inventory creates struggle for stock as sellers wait for Spring

Data released by REINZ for August 2016 shows that housing inventory available for sale is continuing to rapidly fall nationwide, with an 18% decline in properties available for sale year-on-year and five regions with less than 12 weeks of supply, representing almost 70% of sales volumes.

According to the latest figures released today by REINZ, source of the most recent, complete and accurate real estate data in New Zealand, Wellington has the fewest properties for sale with just seven weeks of supply, closely followed by Otago with 10 weeks of supply and Auckland, Waikato/Bay of Plenty and Hawke’s Bay with 12 weeks of supply.

The number of unconditional residential sales in August was 7,527, up 3% on July this year but down 3% compared to August 2015. On a seasonally adjusted basis, the number of sales fell 0.2% from July to August. Sales in Auckland were down 20% compared to August last year.

KEY DATA SUMMARY:

| Median house price year-on-year | National National ex Auckland Auckland | $492,000 - up from $465,000

+5.8% year-on-year $387,250 - up from $348,500 +11.1% year-on-year $842,500 - up from $740,000 +13.9% year-on-year |

| Seasonally adjusted median house price | National Auckland | Down 2% on

July 2016 and up 6% year-on-year

Advertisement - scroll to continue reading

Up 2% on July 2016 and up 13% year-on-year |

| Month-on-month median house price | National National ex-Auckland Auckland | $492,000 – down 3% on July

($505,000) $387,250 - down 1% on July ($390,000) $842,500 - up 2% on July ($825,000) |

| Median days to sell | National Auckland | 30 –

down 1 day year-on-year 30 – up 1 day year-on-year |

Real Estate Institute of New Zealand (REINZ) spokesperson Bryan Thomson says, “The underlying trends indicate that the struggle for stock is the single biggest factor driving market behaviour and price expectations across the country, as we await Spring listings.

“We have been highlighting the lack of inventory for some time, and it continues to be a major contributing factor in the volume of sales across all regions. This is particularly so in Auckland, where inventory levels are at historic lows.”

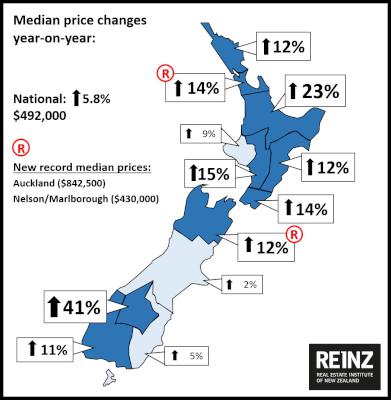

Median prices

The national median price rose 5.8% year-on-year to $492,000, but slipped back 3% ($13,000) from its record high of $505,000 last month.

Two regions hit new record high median sale prices in August:

- Auckland reached $842,500 (up 14% year-on-year, or $102,500)

- Nelson/Marlborough hit $430,000 (up 12% year-on-year, or $45,000).

Excluding Auckland, median prices fell 1%, or $2,780. Central Otago Lakes recorded the largest percentage increase in median price compared to August 2015, at 41%, followed by Waikato/Bay of Plenty at 23% and Manawatu/Wanganui at 15%.

Section sales

Section sales, which are exempt from the new LVR ratios, jumped 37% across the country year-on-year, with Auckland showing an increase of 19%. The strongest growth in section sale numbers in the 12 months to August 2016 occurred in Hawke’s Bay (81%), Southland (74%) and Central Otago Lakes (71%).

Bryan Thomson says that although on the face of it these numbers might look that there is a direct link between LVR changes and a jump in section sales, the rise could have been caused by unrelated releases of sections for sale.

“It remains to be seen over time as to whether there is a link between LVR changes and section sales. However, the increase in the number of section sales is a good indicator of new building consents, with a gap of about four months between a section sale and a building consent being issued. And, although the rate of increase in section sales in Auckland lags behind the national growth rate, the trend bodes well for continued growth in housing supply across the country.”

Days to sell

The number of days to sell has only improved by one day at the national level over the past 12 months, although the regions have seen some significant improvements. Six regions have seen a decrease of 20% or more in the number of days to sell.

Auckland is the only region to see a lengthening of the number of days to sell over the past 12 months, up 1 day to 31 days.

Auction sales

There were 1,799 dwellings sold by auction nationally in August, representing 24% of all sales and a decrease of 117 (-6%) on the number of auctions in August 2015.

Transactions in Auckland represented 60% of national auction sales, a drop from the 72% of national auction sales in August 2015. The number of auctions in Waikato/Bay of Plenty has increased by 40% compared to August 2015, while the number of auctions has increased by 113% in Wellington, albeit off a small base, and by 69% across the rest of New Zealand.

Further data

Across New Zealand the total value of residential sales, including sections, was $4.481 billion in August, compared to $4.650 billion in August 2015 and $4.824 billion in July. For the 12 months ended August 2016 the total value of residential sales was $58.487 billion. The breakdown of the value of properties sold in August 2016 compared to August 2015 is:

| August 2016 | August 2015 | |||

| $1 million plus | 987 | 13.1% | 848 | 10.9% |

| $600,000 to $999,999 | 1,915 | 25.4% | 1,834 | 23.6% |

| $400,000 to $599,999 | 1,819 | 24.2% | 1,995 | 24.9% |

| Under $400,000 | 2,806 | 37.3% | 3,150 | 40.6% |

| All Properties Sold | 7,527 | 100.0% | 7,766 | 100.0% |

For further data, tables and charts on prices, volumes, inventory, days to sell, auctions – and regional commentary and tables – please see the accompanying report.

- ENDS -

Note to Editors:

The monthly REINZ residential sales reports remain the most recent, complete and accurate statistics on house prices and sales in New Zealand. They are based on actual sales reported by real estate agents. These sales are taken as of the date that a transaction becomes unconditional, up to 5:00pm on the last business day of the month. Other surveys of the residential property market are based on information from Territorial Authorities regarding settlement and the receipt of documents by the relevant Territorial Authority from a solicitor. As such, this information involves a lag of four to six weeks before the sale is recorded.

*Seasonal adjustment is a statistical technique that attempts to measure and remove the influences of predictable seasonal patterns to reveal how the market changes over time.

Attachments:

REINZ_Residential_Regional_Commentary__August_2016.pdf

REINZ_Residential_Data_Tables__August_2016.pdf

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts 2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change?

Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change? Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?

Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?