Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Payment times plummet

Payment times plummet

Falling dairy prices expected to hit future cash flow

Commercial cash flow appears to be in rude

health, with analysis of invoice payments revealing that

businesses are paying each other with record speed, although

continued falls in dairy prices are expected to affect

future performance.

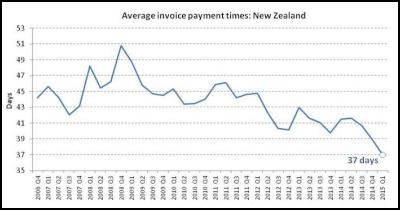

Dun & Bradstreet’s Trade Payments Analysis shows that the average time taken by businesses to pay their invoices dropped to 37 days during Q1 2015, the fastest rate on record, down from 39 days in the previous quarter and 41.5 days last year.

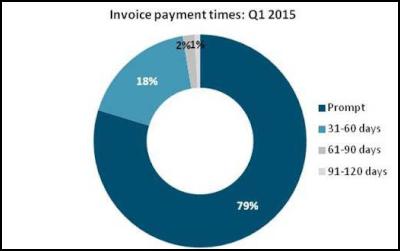

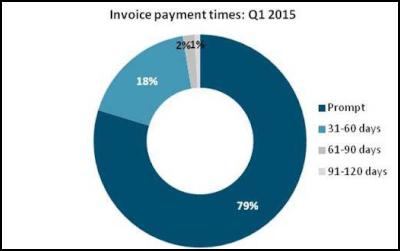

The improvement follows a jump in the proportion of accounts settled on-time (within 30 days), which reached 79 per cent in the three months to March, up from 71 per cent a year earlier.

According to Dennis Martin, Managing Director of Dun & Bradstreet in New Zealand, the latest findings reveal the cash flow benefit from the economy’s performance through 2014, although there are concerns about a slowdown in growth and the affect of falling dairy prices.

“With the Kiwi economy expanding at more than three per cent through last year and consumer spending hitting a high, businesses have been benefitting from a cash injection,” said Mr Martin.

“As the numbers show, this has helped owners to stay on top of their cash flow, settle more of their bills on time, and in turn move money back through the economy more quickly.

“There are signs, however, that the economic performance is easing, with data out this month showing first quarter GDP growth of just 0.2 per cent, and a seventh consecutive fall in dairy prices.

“Based on this, we expect to see a tightening of cash flow in the agriculture sector, which will in turn have a knock-on effect to payment times through the rest of the economy,” Mr Martin added.

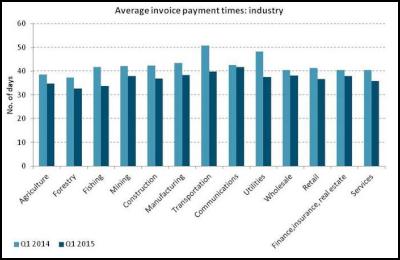

Despite these future expectations, Dun & Bradstreet’s Trade Payments Analysis shows that the agriculture industry paid its invoices in an average of 35 days during the first quarter of the year, two days ahead of the national average and down from 39 days in Q1 2014.

The biggest improvement was recorded by the transportation sector, with its payment times dropping by 11 days compared to last year, to an average of 39.9 days in Q1 2015. The utilities sector also recorded a significant fall in payment times, moving from 48 days to 38 days over 12 months, with both industries benefitting from the sharp drop in oil and fuel prices at the end of last year. The forestry sector, however, was the fastest paying in Q1 2015.

The communications sector was the slowest to pay its invoices, averaging 41.8 days in the first quarter of the year. Despite its significant year-on-year improvement, the transportation industry remained the second slowest to make payments.

Across sectors, the country’s small businesses have been the fastest to settle their accounts. Businesses with between 6–19 employees averaged 36.3 days to pay their bills, down from 40.3 days at the same time last year. Meanwhile, those with fewer than five employees averaged 37.9 days in Q1 2015, down from 40.8 days in 2014.

Big business is the slowest to pay commercial invoices. At an average of 42.5 days, companies employing more than 500 people took five days longer than the national average to pay their accounts during the first quarter of the year, while those with between 200–499 staff were the next slowest, at an average of 40.6 days.

Across the South Island, businesses paid their invoices in an average of 35.6 days, with those in Christchurch averaging 36 days. Businesses based on the North Island were marginally slower, at 37.5 days, while both Wellington and Auckland averaged higher payment times of 38.4 and 39 days respectively.

“The general strength in the

New Zealand economy over the past year has fed into a

further sharp fall in trade payment times,” said Stephen

Koukoulas, Economic Adviser to Dun & Bradstreet.

“Firms

are clearly using this positive cash flow to pay their bills

more quickly than ever before.

“While the rate of

economic growth appears to be slowing, business cash flow

will receive some support from an easing of interest

rates,” Mr Koukoulas

added.

ENDS

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science Retail NZ: Retailers Call For Flexibility On Easter Trading Hours

Retail NZ: Retailers Call For Flexibility On Easter Trading Hours WorkSafe NZ: Worker’s Six-Metre Fall Prompts Industry Call-Out

WorkSafe NZ: Worker’s Six-Metre Fall Prompts Industry Call-Out PSGR: Has MBIE Short-Circuited Good Process In Recent Government Reforms?

PSGR: Has MBIE Short-Circuited Good Process In Recent Government Reforms? The Reserve Bank of New Zealand: RBNZ’s Five Year Funding Agreement Published

The Reserve Bank of New Zealand: RBNZ’s Five Year Funding Agreement Published Lodg: Veteran Founders Disrupting Sole-Trader Accounting in NZ

Lodg: Veteran Founders Disrupting Sole-Trader Accounting in NZ