Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Financial Services Council – Fairer Taxes on Savings

Financial Services Council – Fairer Taxes on Savings

The Financial Services Council (FSC) is supporting a campaign for fairer taxation of savings.

Current tax laws overtax retired New Zealanders living off interest income and New Zealanders saving for retirement. Interest income is over-taxed relative to wage and salary income. This is because the government taxes the part of an interest return that merely compensates a saver for the impact of inflation. This inflation component is not income in economic terms but merely restores the value of the original deposit. Taxing this amounts to taxing of capital deposits.

Take the example of a term deposit earning 5.75% interest. If inflation is 2%, then the actual return to the saver after inflation is 3.75%. However, tax is paid on the full 5.75%. If the saver lends a bank $10,000 for 5 years, about $1,000 of the interest is merely compensation for inflation – restoring the value of the original deposit. However, under current tax laws, 33% of this is taxed as income meaning that in effect $389 of the original deposit is taken as tax.

This does not happen with wages and salaries. Wages and salaries are taxed but not the value of a person’s investment in their education. If a person invests in, say, rental properties, the rent is taxable as income but the original investment on the property is not taxed. The equivalent of the original deposit – the investment in the property – is untaxed.

To correct this penalty on retirement savings,

FSC supports making the effective tax rates on savings the

same as the marginal tax rate savers pay on their other

income. This would require:

• KiwiSaver: That KiwiSaver

fund tax rates be reduced so the effective tax rate is the

same as the saver’s marginal tax rate paid on their other

income.

• Term deposits: That only the interest

received over-and-above inflation be taxed.

This note canvasses the issues involved with limiting tax on term deposits to interest over-and-above inflation.

The

conclusions reached are that changes along these lines would

be expected to:

• Increase government tax revenue by

about $500 million per annum.

• Increase household

after-tax incomes focused on the retired and those saving

for retirement.

• Provide greater incentives for

retirement savings and a greater opportunity for New

Zealanders to save for a comfortable

retirement.

• Discourage highly leveraged investments

such as speculative investments in rental

property.

• There would be an increased incentive to

have term as opposed to call deposits reducing the

vulnerability of our financial sector.

Inflation

Proofing the Tax System

The economic case for

inflation-proofing the tax system is well accepted. There is

no economic or rational policy case for taxing people on

gains that merely reflect movements in the general price

level. There is no logical basis for taxing savers more

highly when inflation is high than when inflation is low or

non-existent. Full inflation-proofing (or indexation) of the

tax base would require the following main adjustments to how

we now calculate taxable income:

• For interest, only

the interest received over-and-above inflation should be

taxed.

• For a trading business, the rise in price of

inventory or stock that merely reflects the general rise in

prices should not be taxed.

• For a business with

capital investments, deductible depreciation should be

calculated on the basis of the inflation-indexed cost of

assets, not their cost measured in terms of nominal dollars.

The objective of inflation proofing or indexing the tax base is that tax payable per a person is in substance the same irrespective of the rate of inflation – the same as when there is no inflation at all. Inflation in other words should not determine one’s tax rate.

The arguments that have been advanced against inflation-indexing the tax system in this way are not theoretical but practical. In essence: are the costs and complexity of making the necessary calculations worth the benefits of better and more accurately measuring actual income? At relatively low rates of inflation (2% to 3% per annum) the answer from officials has been that the advantages of adjusting taxable income to counter the impact of inflation would be relatively small compared with the cost of computation. Inflation indexation of the tax base is not supported on that basis.

The Necessity of Fully Indexing Term

Deposits

However, such an analysis tends to be

focused on a one or two year horizon. The retirement savings

focus is 30 plus years. At about a 2% per annum inflation

rate, over 30 years the inflation adjusted value of the

deposit approximately halves. That halving in value is

compensated by interest but the interest is taxed. Taxing

half the original value of a savings deposit as if it were

income is a material issue. In such cases the complexity of

indexation is more clearly outweighed by the distortions

caused by taxing capital rather than income.

The FSC proposal thus focuses on relieving the tax impost on term deposits (defined as deposits with a term of 90 days or more). It is assumed that most such deposits are rolled-over so are in effect deposits for much longer terms.

FSC recognises that if the inflation component of term deposit interest income is not taxed, then the inflation component of interest expense should similarly not be deductible. The reason for this can be illustrated by a simple example. If a person on a 33% tax rate can borrow funds at a 10% per annum interest rate and invest those funds in a term deposit also at a 10% interest rate, in a tax-free world there is no profit to them. Their cost of borrowing equals their return. However, if the interest income is indexed for tax and the inflation rate is 2%, only an interest rate of 8% is taxable as income. If the funds borrowed are deductible at 10%, the transaction now produces are pure arbitrage tax profit of 2%. It is assumed that the tax base could not sustain a system where interest income is inflation-adjusted but where interest expense is fully deductible.

As a result, consequential to not taxing the inflation compensation component of term deposit, interest would be denied a deduction for the same component of interest expense. It is suggested that this could not be limited to term borrowings (to reflect the restriction of interest income indexation to term deposits) because it would seem too easy to characterise all borrowings as term borrowings.

The Fiscal Consequences of Indexing

Interest for Inflation

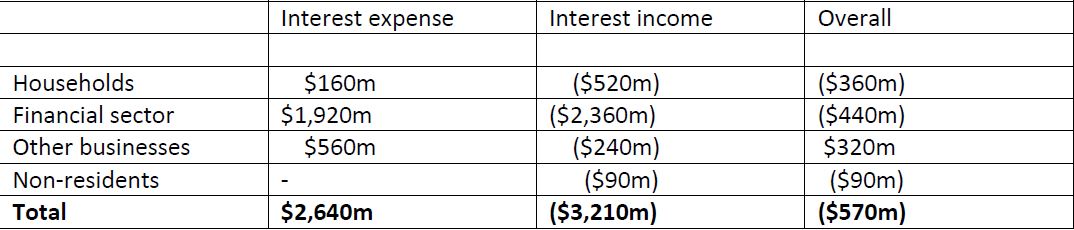

In work produced for the

2011 Savings Working Group officials estimated that the

fiscal costs of fully indexing interest income and expense

for tax purposes would be:

Click for big version.

This results in an overall fiscal cost of $570 million per annum, albeit officials note that this is a broad estimate. Under what is being proposed it would not be necessary to index for inflation the income of non-residents. Non-residents are taxed on interest under special tax rules subject to tax treaties that generally results in them paying a low level of tax. Any further reduction in New Zealand tax would simply increase the tax payable in the non-resident’s home jurisdiction so that there would not seem to be any legal or policy justification for indexing this income. This reduces the fiscal cost by almost $100million per annum.

It is also proposed that indexation of income be limited to term deposits (90 days or more). Based on Reserve Bank figures, approximately one third of deposits are at call or for a term less than 90 days. The fiscal cost of indexing term deposit income would thus be significantly (up to $1 billion) less than the above officials’ estimates.

This suggests a fiscal “saving” (increased government revenue) from the proposal.

Moreover, a significant level of term deposits is likely to be invested by KiwiSaver schemes. It is proposed that KiwiSaver schemes be compensated for the tax penalty on savings by way of a lower tax rate. KiwiSaver schemes would not also be compensated by not being taxed on the inflation component of their term deposits.

In addition, it should be expected that many non-resident and non-resident controlled companies would react to any move by New Zealand to restrict interest deductions to the non-inflation component. If they borrowed money in their home country for an investment into New Zealand they could obtain a full interest deduction. If they raised the same debt in New Zealand they would not be allowed a deduction for the inflation component. The expected reaction would be for them to increase offshore debt (interest on which is deductible in overseas jurisdictions) and to increase the extent to which their New Zealand investment is equity funded with no interest deduction against the New Zealand tax base. In effect, the tax subsidy arising from the deduction for the inflation component of interest costs would be transferred from New Zealand to the taxpayers in the home country of the foreign investor.

The fiscal impact of non-residents reallocating interest expense deductions from the New Zealand to overseas tax bases could be significant. In work produced in 2009 for the Victoria University of Wellington Tax Working Group, officials estimated that every 1 percentage point reduction in non-resident and non-resident controlled company debt levels increase New Zealand tax revenue by over $10 million per annum.

On the basis of the above, it seems clear that indexing term deposits would increase, not decrease, overall government tax revenue by something in the order of $500 million per annum. This revenue could be used to fund a reduction in the tax rate on KiwiSaver (without reducing existing KiwiSaver incentives) and/or other rate reductions.

The Economic

Consequences

Removing tax on the inflation

component of term deposit interest and restricting interest

deductions to the non-inflation component of interest should

have no effect on New Zealand’s general interest rates.

This is on the basis that these are set by the marginal debt

investor who is likely to be a non-resident debt investor

into New Zealand. In substance such a person will be taxed

in their home jurisdiction on their full interest return and

this will continue to be the case.

The economic consequences of any such change will therefore seem to be largely distributional with important and positive incentive effects.

• Households would receive a substantial increase in after-tax income. Based on official estimates this would be up to about $400 million per annum. This tax relief would be focused on those saving for retirement and those in retirement living on investment income. This simply reverses the tax penalty that is currently imposed on this group.

• Non-financial business would have a higher tax cost as a result of restrictions on interest deductions. This sector is a net borrower. Current tax rules provide them with a deduction for the reduction in the principal of a loan as a result of the effect of inflation. This could be offset to some extent by lower business borrowing. The government could consider further tax reductions for the business sector if it considered this to be warranted.

• There would be a reduced incentive in general to borrow funds. For example a person buying a rental property under current rules receives a deduction for interest payments that merely reflect the declining real value of the loan while receiving a tax free capital gain return on the rental property. This asymmetry would be removed.

• There would be an incentive for households to move from call deposits (that would not benefit from an inflation tax adjustment) to term deposits (that would benefit from an inflation tax adjustment). This would reduce the vulnerability of New Zealand’s financial sector to liquidity shortages.

• Foreign investors into New Zealand would be encouraged to equity fund rather than debt fund their New Zealand investments and re-allocate interest costs offshore. This would not only have fiscal savings for New Zealand (reduced interest deductions) but it would also reduce New Zealand’s overall overseas debt reducing the vulnerability of the economy to global financial disruptions. If Australian firms increased their Australian debt (increasing Australian interest deductions) so as to fund New Zealand equity investment, it is likely to be more to Australia’s advantage to look at better integrating our tax systems through mechanisms such as trans-Tasman mutual recognition of imputation credits.

ENDS

Science Media Centre: Cyclone Gabrielle's Impacts On NZ's Ecosystems - Expert Reaction

Science Media Centre: Cyclone Gabrielle's Impacts On NZ's Ecosystems - Expert Reaction RNZ: Parts Of Power System Could Be Out For 36 Hours In Event Of Extreme Solar Storm

RNZ: Parts Of Power System Could Be Out For 36 Hours In Event Of Extreme Solar Storm NZAS: New Zealand Association Of Scientists Awards Celebrate The Achievements Of Scientists And Our Science System

NZAS: New Zealand Association Of Scientists Awards Celebrate The Achievements Of Scientists And Our Science System Stats NZ: Retail Spending Flat In The September 2024 Quarter

Stats NZ: Retail Spending Flat In The September 2024 Quarter Antarctica New Zealand: International Team Launch Second Attempt To Drill Deep For Antarctic Climate Clues

Antarctica New Zealand: International Team Launch Second Attempt To Drill Deep For Antarctic Climate Clues Vegetables New Zealand: Asparagus Season In Full Flight: Get It While You Still Can

Vegetables New Zealand: Asparagus Season In Full Flight: Get It While You Still Can