Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Consumer Stress Drops to Two Year Low

Consumer Stress Drops to Two Year Low

Kiwis’ financial position strengthens despite rate hikes

Consumer stress in New Zealand has fallen to its lowest level since the beginning of 2012 as the economy’s ongoing expansion continues to boost the financial position of Kiwis and strengthen their capacity to borrow and spend.

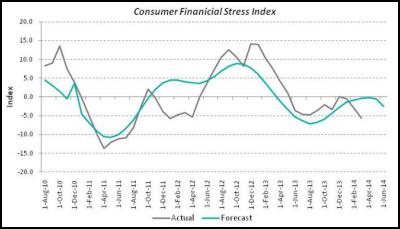

Despite interest rates rising, Dun & Bradstreet’s Consumer Financial Stress Index has found that stress levels improved during the first quarter of the year to reach -5.6 points in March, down from 7.5 points a year earlier. An index reading below zero indicates that lower financial stress exists among consumers.

Increasingly healthy economic conditions in New Zealand have seen the stress index, which reflects consumer credit activity, demand, capacity and confidence, fall ahead of its mid-year forecast, suggesting that Kiwis will continue to see their financial position strengthen throughout 2014.

Last year’s

breakout economic performance in New Zealand saw the

Consumer Financial Stress Index fall from 13.9 points

to zero across the year. According to D&B’s country

analysis, this performance will continue through 2014, with

real GDP growth in New Zealand forecast to lift to 3.4 per

cent on the back of strong trade, bustling business

confidence, population growth and consumer spending.

While further interest rate increases have the potential to temper consumers’ willingness to borrow and spend on credit, D&B expects the economy’s underlying momentum and a healthy jobs market to drive a further reduction in financial stress levels.

“With good news on the economy continuing to circulate during the first quarter of the year we’re seeing consumer optimism consolidate and financial stress ease,“ said Dennis Martin, Managing Director of Dun & Bradstreet New Zealand.

“Falling unemployment and

confidence in jobs growth are supporting consumers’

willingness and ability to spend, while the booming property

and share markets are lifting household wealth.

“While consumers appear set to face additional interest rate increases this year, which will place some strain on their debt repayments, we forecast that stress levels will continue to ease through to the middle of this year,” Mr Martin added.

Fundamental to the positive trend in consumer stress has been the falling unemployment rate, which has declined for consecutive quarters, most recently reaching six per cent in Q4 2013. Job security and employment opportunities are essential to financial comfort and confidence, and have been evident in D&B’s analysis of stress levels.

Reflecting the relatively healthy financial position of Kiwis, the country’s Consumer Financial Stress Index is more than 20 points below the measure in Australia. Although Australia’s economic fundamentals remain sound, its rising level of unemployment in particular has been reflected by deterioration in D&B’s measure of financial stress this year, which reached 18.6 points in March.

“Consumers are in an increasingly sound position, which reflects the solid and now sustained lift in economic activity over the past year and the sharp fall in the unemployment rate,” said Stephen Koukoulas, Economic Advisor to Dun & Bradstreet.

“The strength in the New Zealand economy is apparent in the fact that consumers are spending and borrowing with confidence,” Mr Koukoulas added.

“While the present situation is strong, the start of the interest rate hiking cycle from the RBNZ may pose some challenges over the more medium term as borrowing costs increase, although the risk of a severe deterioration in consumer financial stress remains low,” Mr Koukoulas added.

About the index

Dun & Bradstreet's Consumer Financial Stress Index is an indicative measure of consumer financial stress in New Zealand.

First published in New Zealand in May 2013, the index uses information contained on D&B's extensive credit databases to measure consumer activity, demand, capacity and confidence.

Consumer stress and capacity for financial credit are highly correlated to the broader performance of national economies; with consumer confidence and spending a key driver for small and medium businesses.

The index score is an indicator of other external data trends including personal credit growth and employment rates, and will provide new insight to the consumer side of the economy. The index is bound by -100 – +100, with a score above 0 indicating increased stress, while a score below zero indicates lower stress.

Methodology

The index score is calculated each month from a series of data variables which are derived from information held on D&B's database of New Zealand consumers and companies. These variables are representative of consumer and business themes covering 'confidence', 'desperation', 'awareness', 'cash flow' and 'business risk'.

Weighted and combined, these variables provide two scores of consumers' demand and capacity for credit. Together, these scores create a final index of consumer financial stress that is closely aligned with consumers' ability to meet future credit obligations, and indicative of future business and economic conditions.

About Dun & Bradstreet

Established in 1887, Dun & Bradstreet is Australia and New Zealand's oldest credit information bureau. Backed by its extensive financial database, D&B helps businesses to make informed credit decisions, and consumers to access personal credit information.

D&B works across the entire credit lifecycle to deliver data-driven solutions in sales and marketing, credit reporting and debt management.

Through analysis of financial and behavioural information, D&B also provides current and predictive assessments of the economy, business conditions and credit activity.

ends

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science

Ngā Pae o te Māramatanga: Māori Concerns About Misuse Of Facial Recognition Technology Highlighted In Science Retail NZ: Retailers Call For Flexibility On Easter Trading Hours

Retail NZ: Retailers Call For Flexibility On Easter Trading Hours WorkSafe NZ: Worker’s Six-Metre Fall Prompts Industry Call-Out

WorkSafe NZ: Worker’s Six-Metre Fall Prompts Industry Call-Out PSGR: Has MBIE Short-Circuited Good Process In Recent Government Reforms?

PSGR: Has MBIE Short-Circuited Good Process In Recent Government Reforms? The Reserve Bank of New Zealand: RBNZ’s Five Year Funding Agreement Published

The Reserve Bank of New Zealand: RBNZ’s Five Year Funding Agreement Published Lodg: Veteran Founders Disrupting Sole-Trader Accounting in NZ

Lodg: Veteran Founders Disrupting Sole-Trader Accounting in NZ