Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Consumer Financial Stress Falls

MEDIA RELEASE

29 May 2013

CONSUMER FINANCIAL STRESS

FALLS

Kiwis more financially comfortable in

2013

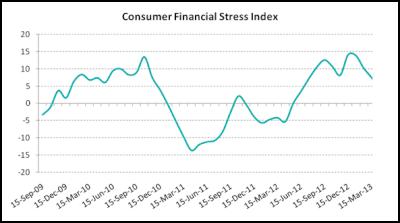

Levels of consumer financial stress have dropped markedly in New Zealand during 2013 as stronger economic conditions buoy the financial position of consumers, with Kiwis also increasing their appetite for credit.

A new

economic index released today shows that after peaking in

late 2012, the same time as the national unemployment rate

reached a 13-year high, consumer financial stress has fallen

for four consecutive months. Dun & Bradstreet’s

Consumer Financial Stress Index, which measures

consumer demand and capacity for credit, has fallen to 4.1

points in April, after previously rising to 14.1 in December

2012.

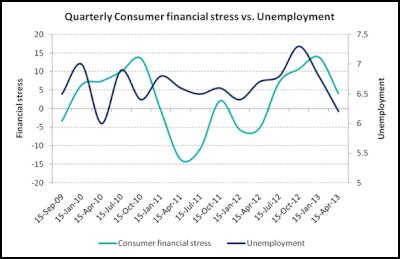

With three-and-a-half years of history, the new

index can be benchmarked against key macroeconomic

variables, including unemployment and personal credit

growth, and indicates consumers' ability to meet their

credit obligations.

The index shows that the level of consumer stress trended upwards in late 2009 and 2010 to reach 13.5 points in October 2010, reflecting the lagging effects of the global financial crisis. However in April 2011, an economic recovery brought financial stress sharply down to a record low of -13.7 points. Movements from mid-2011 onwards were irregular, although stress levels gradually lifted over the following months.

Conditions eased temporarily between November 2011 and January 2012, as the Rugby World Cup boosted tourism and retail spending, before the index continued its upward movement in April 2012. At this time, consumer sentiment was weak, particularly in Christchurch due to the series of earthquakes, and because of the broader concerns being expressed about the risks to the New Zealand from the problems in the Eurozone economies and a slowdown in China.

After peaking in late 2012, financial stress appears to be steadily easing, reflecting other positive measures of the national economy, including the unemployment rate.

The falling index reflects official statistics indicating a solid economic performance through the first quarter of 2013 and further positive news since, including increased trade growth with China. In addition, a pick-up in the housing market over the past few months, solid business activity and low interest rates have had a positive flow-on effect to consumer confidence.

“This year we are clearly seeing consumers benefit from a steady improvement in economic conditions,” said D&B New Zealand General Manager, Lance Crooks.

“The Consumer Financial Stress Index reflects this recent change in conditions and also matches what we’re finding in our other research. Kiwis are reporting that they are more comfortably meeting their financial obligations, like credit cards, loans and electricity bills, and that they expect to reduce their future levels of debt,” he said.

“As a result, financial stress is easing and consumers are regaining their appetite for new credit – although we expect that a cautious approach to spending is likely to continue for some time,” he added.

D&B’s most recent Consumer Credit Expectations Survey has found that New Zealanders are cautiously optimistic about their personal finances, opting to raise their credit limits over the coming months. In addition, 60 per cent of people expect to find it easy to pay their credit bills in the coming months and one-quarter expect to reduce their debt levels.

According to Stephen Koukoulas, Dun & Bradstreet’s Economic Advisor, the Consumer Financial Stress Index presents a unique and high-level view of the financial comfort and behaviour of consumers, thus providing useful insight into the near-term momentum of the economy.

“The three-and-a-half year history of the index has been distorted by the hangover from the global banking and financial crisis, however changes in the level of the index are closely correlated with growth in employment, house prices and to a lesser extent, retail trade,” Mr Koukoulas said.

"In late 2012 we saw a steady rise in the

index and rising unemployment levels which risked

off-setting the positive signs of coming out of the New

Zealand economy.

"The recent fall in consumer financial

stress, however, is a welcome sign and it is likely to

continue to benefit from the steady, low level of interest

rates, falling unemployment and strong house prices," Mr

Koukoulas added.

-------

About the index

Dun & Bradstreet's Consumer Financial Stress Index is an indicative measure of consumer financial stress in Australia.

First published in New Zealand in May 2013, the index uses information contained on D&B's extensive credit databases to measure consumer activity, demand, capacity and confidence.

Consumer stress and capacity for financial credit are highly correlated to the broader performance of national economies; with consumer confidence and spending a key driver for small and medium businesses.

The index score is an indicator of other external data trends including personal credit growth and employment rates, and will provide new insight to the consumer side of the economy.

The index is bound by 100 +100, with a score above 0 indicating increased stress, while a score below zero indicates lower stress.

Methodology

The index score is calculated each month from a series of data variables which are derived from information held on D&B's database of New Zealand consumers and companies. These variables are representative of consumer and business themes covering 'confidence', 'desperation', 'awareness', 'cash flow' and 'business risk'.

Weighted and combined, these variables provide two scores of consumers' demand and capacity for credit. Together, these scores create a final index of consumer financial stress that is closely aligned with consumers' ability to meet future credit obligations, and indicative of future business and economic conditions.

About Dun & Bradstreet

Established in 1887, Dun & Bradstreet is Australia and New Zealand's oldest credit information bureau. Backed by its extensive financial database, D&B helps businesses to make informed credit decisions, and consumers to access personal credit information.

D&B works across the entire credit lifecycle to deliver datadriven solutions in sales and marketing, credit reporting and debt management.

Through analysis of financial and behavioural information, D&B also provides current and predictive assessments of the economy, business conditions and credit activity.

ENDS

New Zealand Airports Association: Airports Welcome Tourism Marketing Turbocharge

New Zealand Airports Association: Airports Welcome Tourism Marketing Turbocharge Ipsos: New Zealanders Are Still Finding It Tough Financially; Little Reprieve Expected In The Next 12 Months

Ipsos: New Zealanders Are Still Finding It Tough Financially; Little Reprieve Expected In The Next 12 Months NZ Telecommunications Forum - TCF: Telecommunications Forum Warns Retailers About 3G Shutdown

NZ Telecommunications Forum - TCF: Telecommunications Forum Warns Retailers About 3G Shutdown PSA: Worker Involvement Critical In Developing AI For The Good Of Aotearoa

PSA: Worker Involvement Critical In Developing AI For The Good Of Aotearoa MBIE: Easter Trading Laws - Your Rights And Responsibilities

MBIE: Easter Trading Laws - Your Rights And Responsibilities The Conversation: As More Communities Have To Consider Relocation, We Explore What Happens To The Land After People Leave

The Conversation: As More Communities Have To Consider Relocation, We Explore What Happens To The Land After People Leave