Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Home loan affordability now worst since November 2010

Roost Home Loan Affordability report

For December 2011 – For immediate release

Home loan affordability now worst since November 2010 as regional differences build

--------------------

Home loan affordability continues to get worse nationally and ended 2012 at its worst level since November 2010.

Interest rates remain low and are virtually unchanged, and the slow rise in take-home pay continues in almost all regions. But it is house prices that are driving the index.

Median house prices reached a record $389,000 at December according to REINZ data, up $34,000 in a year. First quartile house prices reached $270,000, also a record, but only up $15,000 over the year.

In cities where there is a good balance between housing supply and demand, we are not seeing prices rise fiercely. But in those urban centers where supply is constrained, affordability is worsening markedly as the cost of buying a house rises.

Nationally, affordability deteriorated by 3.6% in the year to December 2012. That is, it took 3.6% more of take home pay to afford the mortgage payments for a median priced house, according to the Roost home loan affordability report released today.

This means it cost $39.01 more per week in December 2012 than in December 2011 to make home loan payments on a median priced house.

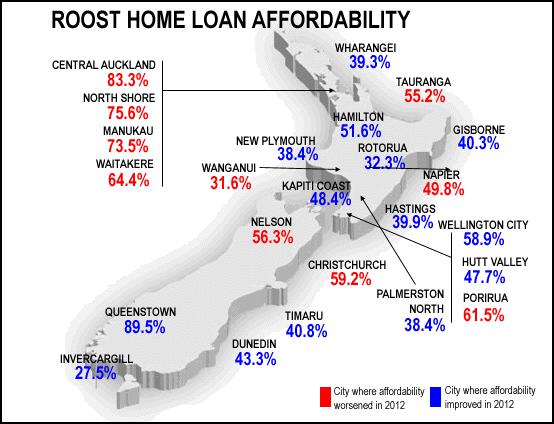

Central Auckland, Auckland’s North Shore, Waitakere, Porirua, Christchurch and Queenstown all deteriorated quickly over the year, with Porirua making the biggest move, getting worse by 9.5%.

Invercargill, the Kapiti Coast, Whangarei and Tauranga all improved their affordability over 2012.

Advertised floating mortgage rates have been unchanged since March last year, but average 6 month and 1 year mortgage rates edged lower by about half a percent over the year.

Median take-home pay for homebuyers in the 30-34 age group – which is after-tax pay – grew by $19.70 per week, almost $1,025 per year during 2012. It grew the most in Wellington City – by $25.07 per week – and the least in Gisborne of $18.63 per week.

For first home buyers – which in this Roost index are defined as a 25-29 year old who buys a first quartile home – the news is not as bad.

For these buyers outside of the ‘usual suspects’ in Auckland and Queenstown, there have been small improvements in affordability. However, Wanganui, Porirua and Nelson all found housing for first home buyers less affordable as 2012 ended. It was tough in Christchurch as well.

Any level over 40% is considered unaffordable, whereas any level closer to 30% has coincided with increased buyer demand in the past.

For working households, the situation is similar although bringing two incomes to the job of paying for a mortgage makes life considerably easier.

On this basis, 18 of 24 New Zealand cities have a household affordability index below 40% for couples in the 30-34 age group. This household is assumed to have one 5 year old child. Couples in central Auckland, Manukau and Porirua all found it more expensive to pay a mortgage at the end of 2012 than at the beginning, although in almost all other centers the change was minor over the year.

For households in the 25-29 age group (which is assumed to have no children), every city except Queenstown ended the year with the cost of a mortgage lower than 40% of their take-home pay. There was only a marked deterioration in central Auckland; couples in almost all other centers found it no harder to pay the mortgage at the end of the year than at the beginning.

Any level over 30% is considered unaffordable in the longer term for such a household, while any level closer to 20% is seen as attractive and coinciding with strong demand.

Of the 24 cities we monitor, 17 of them had an index below 30% as at December 2012, six were between 30-40% and one (Queenstown) was above 40%.

First home buyer household affordability is measured by calculating the proportion of after tax pay needed by two young median income earners to service an 80% home loan on a first quartile priced house.

Roost Home loan affordability for typical buyers

General/New Zealand Report: http://www.interest.co.nz/property/home-loan-affordability

Links

to individual reports for regions can be found here

Roost Home loan affordability for first-home buyers

General/New Zealand Report:

http://www.interest.co.nz/first-home-buyer

Links

to individual reports for regions can be found here

--

Question and

Answers about the report

How does interest.co.nz work

out these numbers?

Interest.co.nz gathers data from Statistics New Zealand and IRD on wages in each region, data from the Real Estate Institute from each region each month, and data from banks and non-banks on interest rates. It has calculated home loan affordability going back to the beginning of 2002.

How is this survey different from

the Massey University survey of affordability?

The Massey study is only done quarterly rather than monthly and uses an index of Home affordability rather than actually measuring home loan affordability. It uses an index rather than the actual measure of the proportion of after tax pay needed to service an 80% mortgage on a median home. The exact composition and meaning of the index is not detailed.

Why use a single median income rather than

household income?

It’s true that most homebuyers are using a combination of one or more full or part time incomes to service their mortgage. Each household is different and may be using incomes from different sources. The best measure of average national household income is calculated officially once in every three years by Statistics New Zealand. Interest.co.nz chose to use the median income data series from IRD and Statistics NZ because it can be measured monthly and can be drilled down by region and by age. We do include a chart showing how many median incomes are required to keep mortgage payments at 40% of take home pay. It is currently around 2 median incomes.

Why is home loan

affordability important?

It is a useful way to work out if a housing market is overvalued. It’s clear house prices stopped rising when the national affordability ratio rose above 80% or 2 median incomes to service the average home loan. It’s a way of comparing affordability of housing markets with a national average and comparing housing values from one year to the next. For example, the affordability ratio in 2002 before the housing boom really took off was around 41%.

About Roost

Roost is the sponsor of this Report, and the Reports must be referred to as the Roost home loan affordability reports. Roost, owned by AMP, is one of New Zealand’s largest independent home loan and investment property mortgage brokers with 16 franchisees nationwide. Roost offers to source the perfect loan for its customers from a panel of lenders and insurance advice from Roost insurance specialists. Roost was established in 1996. For more information please visit www.roost.co.nz

ENDS

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges?

Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges? Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction

Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts