Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Unsettled Conditions Create Slower Early Spring Rural Real

News Release 11 October

2012

Unsettled Conditions Create

Slower Early Spring

Rural Real Estate

Market

Summary

• Sales

up 5 per cent year on year

• Median $/ha price

rose 2 percent compared to September 2011

• REINZ All Farm Price Index and REINZ Dairy

Farm Price Index both rose in

September

• Shortage of listings emerging as a

serious constraint for buyers

Data released today by the Real Estate Institute of NZ (“REINZ”) shows there were 11 more farm sales (+4.7%) for the three months ended September 2012 than for the three months ended September 2011. Overall, there were 269 farm sales in the three months to end of September 2012, compared with 318 farm sales in the three months to August 2012, a decrease of 49 sales (-15.4%). 1,425 farms were sold in the year to September 2012, 35.3% more than were sold in the year to August 2011.

The median price per hectare for all farms sold in the three months to September 2012 was $18,041; a 2.0% increase on the $17,694 recorded for three months ended September 2011. The median price per hectare increased by 0.5% compared to August 2012.

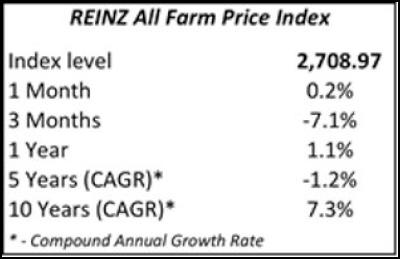

The REINZ All Farm Price Index rose by 0.2% in the three months to September compared to the three months to August, from 2,702.8 to 2,708.97. Compared to September 2011 the REINZ All Farm Price Index increased by 1.1%. Further details on the REINZ All Farm Price Index are set out below.

Six regions recorded increases in sales volumes for the three months ended September 2012 compared to the three months ended September 2011. Canterbury recorded the largest increase in sales (+22 sales), followed by Auckland (+21 sales) and Nelson (+12 sales). Wellington recorded 11 fewer sales followed by Southland and Manawatu/Wanganui (-10 sales) and Northland (-7 sales) in the three months to September 2012 compared to the three months to September 2011. Compared to the three months ended August 2012 only three regions recorded an increase in sales, lead by Auckland (+8 sales).

“Unsettled weather and market conditions have put a dampener on the early spring rural real estate market,” says REINZ Rural Market Spokesman Brian Peacocke. “Cold, wet conditions have impacted on feed supplies and production resulting in increased ‘on farm’ stress.”

“We are seeing strong demand for quality dairy and larger sheep and beef farms, but the shortage of listings is a serious constraint on buyers. Whilst we are expecting more properties to come to market during October and November, the anticipated increase is unlikely to be sufficient to meet the increasing demand.”

Grazing properties accounted for the largest number of sales with 52.0% share of all sales over the three months. Finishing properties accounted for 16.7%, with Horticulture properties accounting for 13.8% and Special properties 5.2% of all sales. These four property types accounted for 87.7% of all sales during the three months ended September 2012.

Dairy

Farms

For the three months ended September

the median sales price per hectare for dairy farms was

$19,604 (9 properties), compared to $24,492 for the three

months ended August 2012 (21 properties), and $29,668 (19

properties) for the three months ended September 2011. The

median dairy farm size for the three months ended August

2012 was 256 hectares.

Included in sales for the month of September were two dairy farms at a median sale value of $33,992 per hectare. The median farm size was 159 hectares with a range of 139 hectares in the Waikato to 178 hectares in Canterbury. The median production per hectare across all dairy farms sold in September 2012 was 1,026kgs of milk solids.

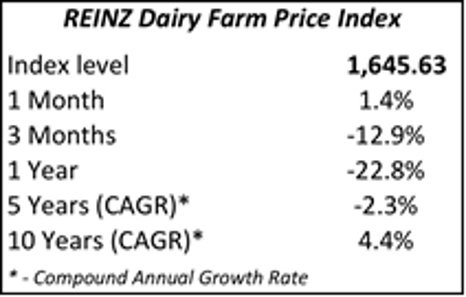

The REINZ Dairy Farm Price Index rose by 1.4% in the three months to September compared to the three months to August, from 1,622.87 to 1,645.63. Compared to September 2011 the REINZ Dairy Farm Price Index fell by 22.8%. Further details on the REINZ Dairy Farm Price Index are set out below.

Finishing

Farms

For the three months ended September

2012 the median sales price per hectare for finishing farms

was $22,468 (45 properties), compared to $20,941 for the

three months ended August (56 properties), and $18,735 (36

properties) for the three months ended September 2011. The

median finishing farm size for the three months ended

September 2012 was 53 hectares.

Grazing Farms

For the three months ended September 2012

the median sales price per hectare for grazing farms was

$11,444 (140 properties) compared to $11,297 for the three

months ended August 2012 (159 properties), and $12,330 (144

properties) for the three months ended September 2011. The

median grazing farm size for the three months ended

September 2012 was 89 hectares.

Horticulture

Farms

For the three months ended September

2012 the median sales price per hectare for horticulture

farms was $141,968 (37 properties) compared to $130,000 (41

properties) for the three months ended August 2012, and

$82,000 (19 properties) for the three months ended September

2011. The median horticulture farm size for the three

months ended September 2012 was five

hectares.

Lifestyle Properties

The lifestyle property market saw a 6.2% increase in sales volume in the three months to September 2012 compared to September 2011. 1,339 sales were recorded in the three months to September 2012 compared to 1,261 sales in the three months to September 2011. 48 fewer sales were recorded compared to the three months to August 2012 (-3.5%).

Just two regions recorded increases in sales compared to August while 11 recorded decreases. Hawkes Bay recorded the largest increase (+3 sales), followed by Taranaki (+2 sales). Wellington recorded the largest fall in sales (-10 sales), followed Auckland and Bay of Plenty (both -9 sales). Compared to September 2011 eight regions recorded increases in sales with six regions recorded decreases.

The national median price for lifestyle blocks eased by $5,000 (-1.1%) from $455,000 for the three months to August 2012 to $450,000 for the three months to September 2012. Compared to three months to September 2011 the median price rose by $20,000 (+4.7%).

The number of days to sell for lifestyle properties improved by seven days, from 88 days for the three months to the end of August to 81 days for the three months to the end of September. Compared to the three months ended September 2011 the number of days to sell improved by 26 days from 107 days to 81 days. West Coast recorded the shortest number of days to sell in September at 48 days, followed by Canterbury at 49 days and Gisborne at 52 days. Otago recorded the longest number of days to sell at 178 days, followed by Hawkes Bay at 127 days and Nelson at 125 days.

Commenting on the lifestyle property market statistics Brian Peacocke said, “There has been a greater depth of localised activity near Auckland, and the steady market in the Waikato continues to benefit from buyer enquiry from outside the region. Marlborough is also benefitting from strong enquiry, and whilst there has been a slight increase in activity in Canterbury, slow insurance payouts are impacting on affordability and the pace of transactions.”

REINZ All Farm Price

Index – Additional Data

The table below

sets out the returns for the REINZ All Farm Price Index for

the three months ending September 2012.

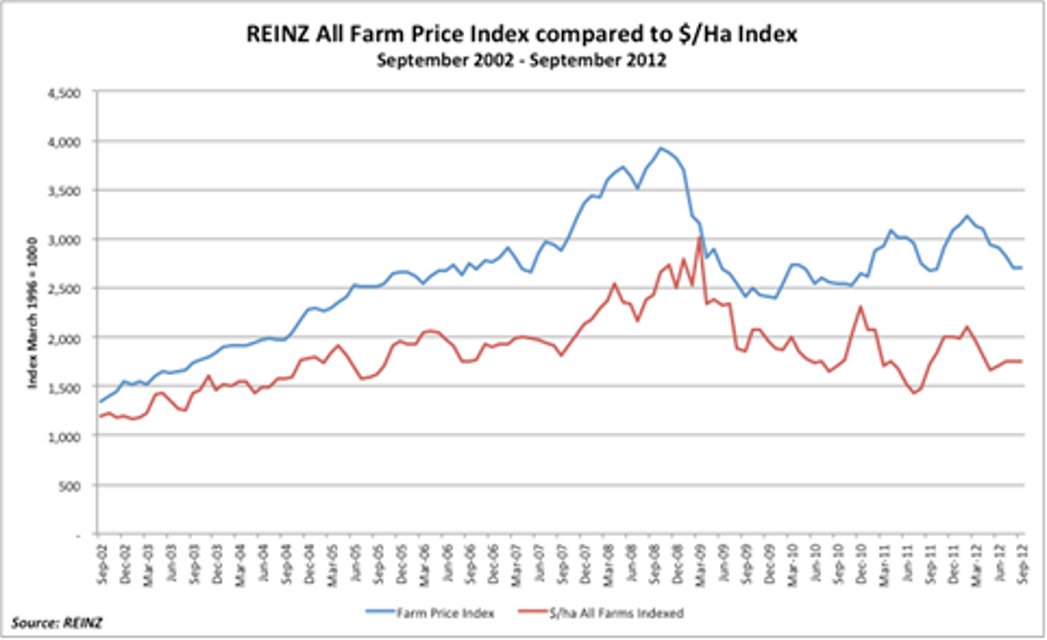

The graph below shows the trends in the REINZ All Farm Price Index compared to an index of movements in the $/hectare measure of farm prices.

Click for big version.

REINZ

Dairy Farm Price Index – Additional

Data

The table below sets out the returns

for the REINZ Dairy Farm Price Index for the three months

ending September 2012.

Click for big version.

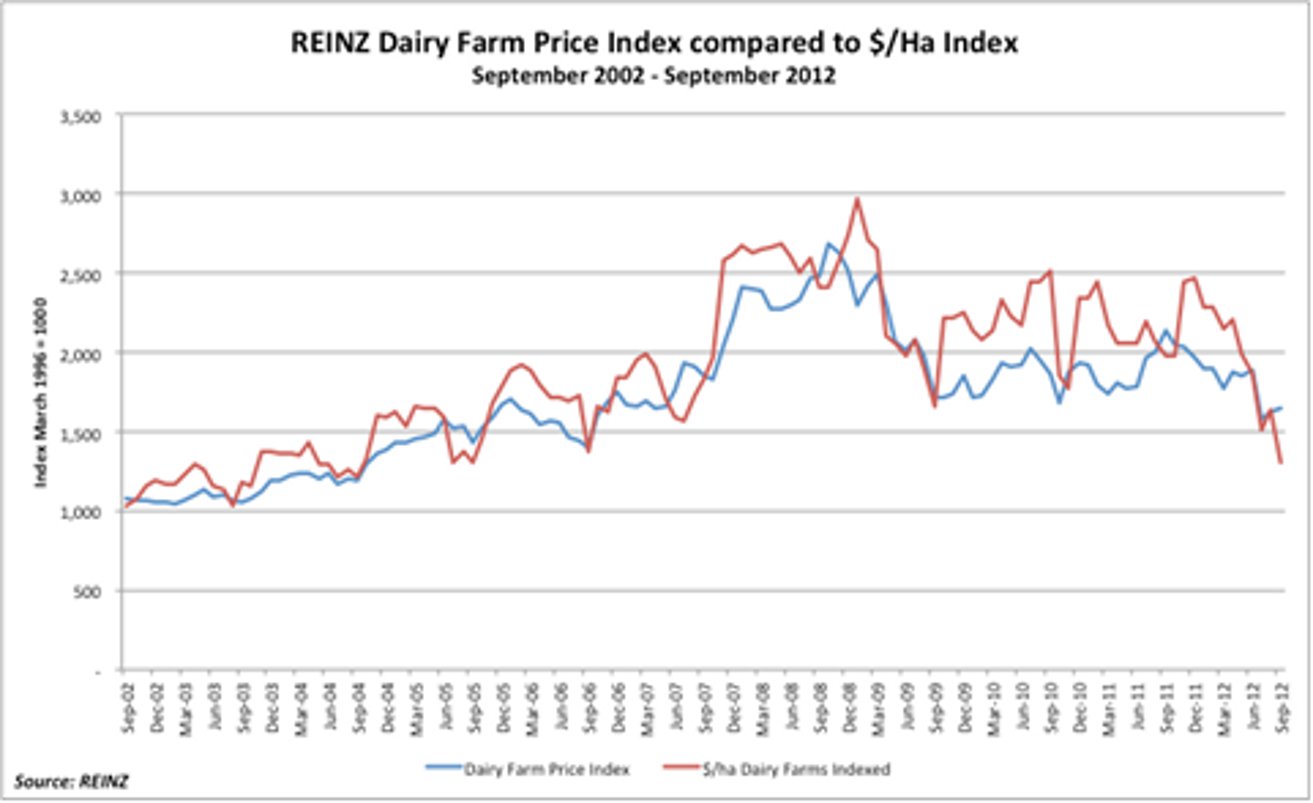

The graph below shows the trends in the REINZ Dairy Farm Price Index compared to an index of movements in the $/hectare measure of farm prices.

Click for big version.

----------

Real Estate Institute of New Zealand

For more real estate information and market

trends data, visit www.reinz.co.nz. For New Zealand's most

comprehensive range of listings for residential, lifestyle,

rural, commercial, investment and rental properties, visit

www.realestate.co.nz - REINZ's official

property directory website.

Editors

Note:

The information provided by REINZ

in relation to the rural real estate market covers the most

recently completed three month period; thus references to

July refer to the period from 1 July 2012 to 30 September

2012.

The REINZ Farm Price Indices have been

developed in conjunction with the Reserve Bank of New

Zealand. It adjusts sale prices for property specific

factors such as location, size and farm type which can

affect the median $/hectare calculations and provides a more

accurate measure of farm price movements. The REINZ Farm

Price Indices has been calculated with a base of 1,000 for

the three months ended March 1996. The REINZ Farm Price

Indices is best utilised in assessing percentage changes

over various time periods rather than trying to apply

changes in the REINZ Farm Price Index to specific property

transactions.

ENDS

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges?

Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges? Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction

Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts