Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Share Split For Widespread Portfolios Limited

New Zealand Exchange Limited

P.O. Box

2959

Wellington

24 July

2012

Share Split For Widespread

Portfolios Limited

The board of Widespread

has resolved to split all ordinary shares on issue in the

ratio of 1 for 20.

The treatment on fractions of ordinary shares following the split will be that a fraction under 0.5 will be rounded down and a fraction of 0.5 or more will be rounded up.

The record date for the split is 5pm 7 August 2012 and the split will take effect as at the commencement of trading on 13 August 2012.

Rationale for Split

In June 2008, in response to unanimous

feedback from the many share-brokers we were presenting to

at the time, the Widespread directors decided to consolidate

our shares 50:1.

The results of this decision have been quite unsatisfactory and clearly not in the interests of you, our shareholders.

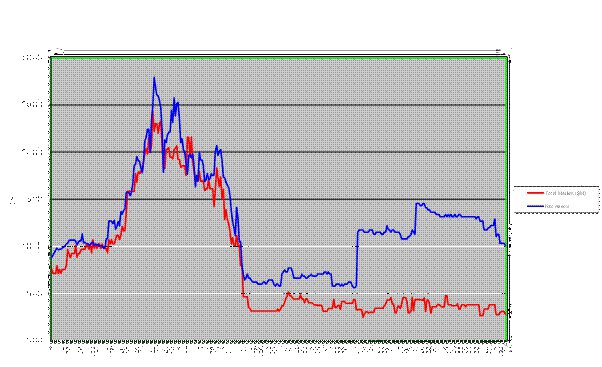

Until that point (week 131 in the chart below), the market value of the company (red line) had closely tracked the next asset backing (blue line).

Click for big version.

In the 212 weeks subsequent to the consolidation, the two lines have diverged and our shares have traded at an average discount to net assets per share of 55.7%, with an average in the last 26 weeks of 72%

In the 130 weeks prior to the consolidation our shares traded at an average discount to net assets per share of 9.8%.

Market conditions have varied during the entire 342 week period and so has the asset backing per share.

However, a significant recent renaissance in the intrinsic value of Widespread shares (measured in terms of net assets per share) has been totally disregarded in share-market terms. Our shares have gravitated to a ~ 12 cent level and refuse to move much above that, notwithstanding the doubling of our net assets per share (to around 40 cents) in the last two years.

Trading volumes have also dropped significantly since the consolidation – the average weekly turnover was $33,120 before the consolidation and has been $1,566 since.

Partially reversing the consolidation is the obvious solution and your directors have resolved to split the shares 20:1.

We acknowledge, this will transform our stock into a genuine penny stock but at 14 cents we can hardly be described as blue chip.

Our expectation is that post-split the market value of the company will better reflect the value of the assets held by the company, and that trading volumes will increase. These expectations are clearly advantageous for shareholders and more than offset the “penny dreadful” connotations of returning to trade at or below 1 cent (where we traded for several years).

The directors are undertaking this move to create tradeable shareholder wealth. This is our primary responsibility, not to have our shares trading at a perceived fashionable price level.

The last sale price of 14 cents should, post split, become 0.7 of a cent, and the terms of the 2017 warrants will similarly adjust (i.e. exercise price will be divided by 20 to just under 7.5 cents)

Given the history of share price behaviour after share splits it will be surprising if our shares do not move above their theoretical level.

A healthier share price will make assets cheaper to buy and this may become particularly relevant as we are presently evaluating various expansionary moves on the back of the ongoing growth of Chatham and the recovery of Asian Minerals.

Shareholders will be well aware that we actively communicate with them and with the market and this will continue.

Effect on Warrants

The terms

of issue of Widespread’s “WIDWA” warrants set out an

adjustment procedure to be applied following a split. Please

note this will only apply to the warrants that are extended

on or before this coming Friday. This adjustment has been

applied and results in the following:

§ The number of

shares into which a warrant may be exercised is increased

from 2 shares to 40 shares.

§ The exercise price per

underlying share is adjusted to $0.074525 for the period

from 10 August 2012 to 17 July 2017.

Warrants cannot be

exercised in part and accordingly to exercise one warrant

(and receive forty shares) on or before 17 July 2017 an

exercise price of $2.981 will be payable (being the same

exercise price as prior to the share split occurring).

An

illustrative table showing the effect of these changes

follows.

On behalf of the Board,

Chris

Castle

Managing Director

Example of how

Share Split Affects Widespread

Securityholders

The following table

illustrates the theoretical position of a securityholder

that holds 1,000 shares and 1,000 warrants pre-split and the

effect of the adjustments outlined above:

Pre-Split Post-Split

Shares Held 1,000 20,000

Warrants Held 1,000 1,000

All Warrants Exercised at $2.981 per

Warrant $2,981.00 $2,981.00

Shares

issued upon warrant exercise 2,000 40,000

New Shareholding 3,000

60,000

ENDS

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts 2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications

2Degrees: Stop The Pings - Half Of Kiwis Overwhelmed By Notifications Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change?

Electricity Networks Association: How Many More Trees Need To Fall On Power Lines Before The Rules Change? Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets?

Parrot Analytics: Netflix Earnings - Price Hikes With Minimal Churn | Will Netflix Be A Bright Spot For Markets? Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand

Canterbury Museum: Mystery Molars Lead To Discovery Of Giant Crayfish In Ancient Aotearoa New Zealand