Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

Daily Economic Briefing: February 24, 2010

Daily Economic Briefing: February 24, 2010

Click here for the full Research and

disclosures.

Page 1 of 3: Global data summary

• Bernanke’s prepared testimony reaffirmed

that an expected backdrop of low rates of resource

utilization, subdued inflation, and stable inflation

expectations is consistent with a low for long stance on

policy interest rates.

•

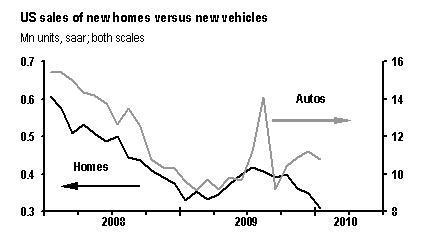

• The sales of US new

homes continued to slide in January, reaching just 309,000,

which is slightly below the lows from a year ago. This

negative surprise follows a similarly suprising drop in

February consumer confidence yesterday. It is interesting to

compare the underlying trends in the sales of new homes vs

new vehicles, both of which were the target of temporary

government subsidy schemes designed to boost sales (see page

3).

•

• Our global research has tended to focus

on the divergence between the recovery in domestic demand in

the US vs the lack of a recovery in domestic demand in

Europe. This point was on display again today in Germany’s

4Q GDP report. Domestic demand fell at an 8.5% annual rate

(3.1% for final demand, supposedly 5.4% for inventories,

although this may not be measured well). The lifeline for

the economy was net trade, which boosted GDP by 9% pts as

exports continued to rebound at a double-digit pace while

imports contracted in conjunction with final domestic

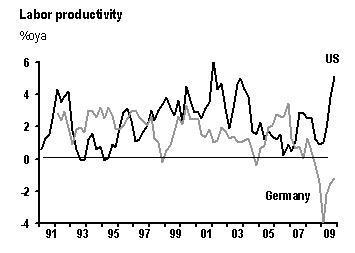

demand. One of the other notable features of the GDP report

was the decline in German labor productivity (-1.2%oya) vs

the US (+5.1%). This divergence makes for a strikingly

different foundation for corporate profits and, thus, future

spending.

•

• On the question of domestic demand,

Japan has fallen in between the US and Europe. Consumption

has expanded solidly in the recovery as in the US, but there

has yet to be a confirmed pickup in capex. As in Germany,

net trade has swung from being a drag on growth during the

recession to a major plus for growth in recent quarters.

Looking ahead, it will be important to see how much consumer

spending growth slows in 1H10 as fiscal stimulus wanes. Our

team expects real PCE growth of just 0.5% in these quarters.

The next update comes with the January reports on retail

sales (Fri) and household spending

(Tues).

•

• Notably, Japan delivered very good

reports on real exports (January) and the Shoko Chukin small

business survey (February). Export volume rose 1.5%m/m last

month, on the heels of 40% annualized growth in 4Q09, 53% in

3Q09 and 58% in 2Q09, and now stand 14% below their old

high. The small business survey rose another 1pt to 42.3,

largely recovering from the small pothole that developed in

December. But what really catches the eye are survey

respondents’ projections for March, which jumped an

additional 4pts to 46.4. It remains to be seen whether this

will materialize, but the March projection is the highest

since late 2007, which is impressive since this is a survey

of small businesses, which have lagged behind in the

recovery.

•

Page 2 of 3: Currency swings impacting goods prices

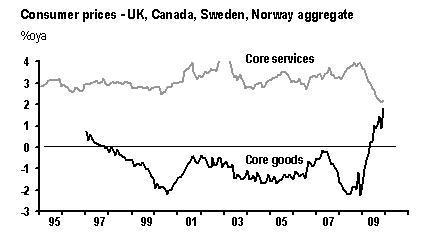

On Monday, we

highlighted the divergence of core goods prices relative to

services in developed countries. We argued that the

surprising increase in DM core goods prices was attributable

to tax hikes and resilient auto prices in the US and

UK—likely related to government auto incentives. In

contrast, in the Euro area and Japan, core goods inflation

has moved down as expected over the past year.

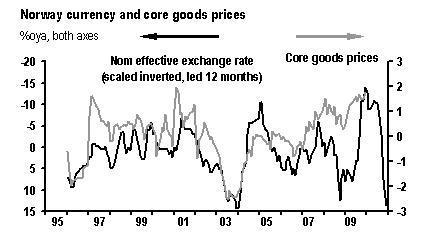

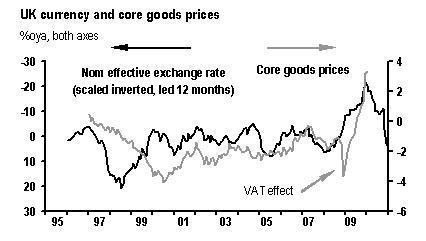

Currencies are also affecting consumer prices in some countries, especially the smaller, open economies. (Note that these effects cancel out on a global basis) Currency effects mostly affect the prices of goods, since they make up the majority of cross-country trade, whereas most services are consumed domestically.

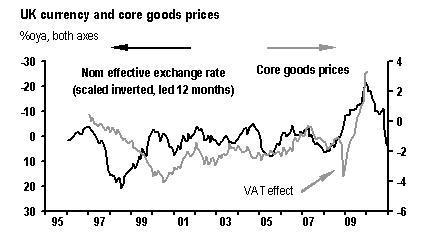

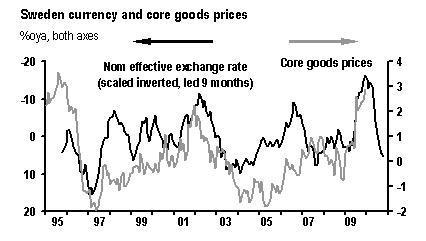

In Western Europe, the impact is evident in the UK and Scandinavia, where currencies declined considerably in the second half of 2008 and early 2009. Based on our quick analysis of the passthrough, there is about a 2-4 quarter lag for these currency effects to filter through to core consumer goods prices. As such, currency depreciation is still putting upward pressure on prices even as currencies have begun moving the opposite direction. By the same token, the subsequent firming (UK) or lift (Scandis) in currencies should have a stabilizing (UK) or disinflationary (Scandis) impact in coming months.

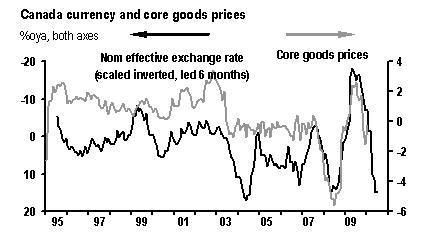

In Canada, where we find the passthrough from currency changes to consumer goods happens more quickly, it seems likely that the Looney is already exerting downward pressure on prices. Consumer goods prices are falling on an over-year-ago basis, though the sharp deceleration in 2H09 was likely largely due to changes in sales taxes.

Page 3 of 3: Differing "payback" from US government sales incentives

The sales of US new homes

continued to slide in January, reaching just 309,000, which

is slightly below the lows from a year ago. It is

interesting to compare the underlying trends in the sales of

new homes vs new vehicles. Both sectors were the target of

temporary government subsidy schemes designed to boost

sales. With hindsight, the cash for clunkers program gave a

lift to car sales after they already had started to recover,

and sales remained on this recovery path after the incentive

program ended. Thus, the “payback” for cash for clunkers

has been rather limited, as sales did not collapse to new

lows after the program ended, as some had feared. On the

other hand, new home sales had not shown any signs of

bottoming until the tax credit took effect. They peaked in

summer, then turned down decisively after the credit

expired. Indeed, new home sales are still falling even

though the credit has since been reinstated.

It will be interesting to see how existing home sales fare in Friday’s report. The resale market began to diverge from the new home market beginning in 2008, with resales recovering early and much more strongly This resilience has been maintained in recent months. Resales corrected downward after the tax credit expired, but to a level far above their first-half average, similar to the pattern in the car market. The evidence suggests that homebuyers have shifted to the resale market because of deeper price reductions, especially on foreclosed homes. This substitution effect limits the construction of new homes—which is a damper for current economic activity. But it is helping to absorb the glut of existing supply and put a floor under prices. This supports household net worth and consumer spending—which is an offsetting plus for current economic activity.

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

Click to enlarge

ENDS

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance

NZ Trucking Association: TruckSafe New Zealand Launches | A Game-Changer For Heavy Vehicle Safety And Compliance Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges?

Gaurav Mittal, IMI: How Can We Balance AI’s Potential And Ethical Challenges? Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction

Science Media Centre: Several US-based Environmental Science Databases To Be Taken Down – Expert Reaction Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills

Consumer NZ: Despite Low Confidence In Government Efforts, People Want Urgent Action To Lower Grocery Bills NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation

NZ Banking Association: Banks Step Up Customer Scam Protections And Compensation The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts

The Reserve Bank of New Zealand: CoFR Seeking Feedback On Access To Basic Transaction Accounts