Scoop has an Ethical Paywall

Scoop has an Ethical Paywall

ASB Housing Confidence Survey

1 May 2006

ASB Housing Confidence

Survey

Statement made by Anthony Byett, Chief Economist ASB

- Fewer people are expecting house

price increases,

- Or expect a rise in interest

rates

- On balance people don’t think now is a good time

to buy

A less frothy outlook appears to be prevailing amongst participants in the housing market, and is reflected in a variety of changed attitudes in the findings of the latest ASB Housing Confidence survey for the three months ending April 2006.

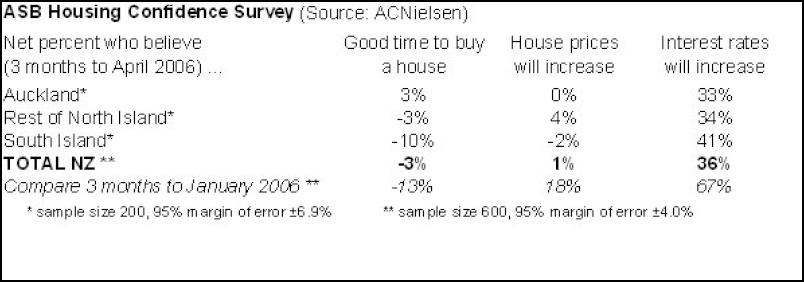

Overall people remain of the opinion that now is not a good time to buy, although the percentage did improve significantly to a net -3% (up from -13%). This may be due in part to a relatively positive March for the property market, and competitive activity amongst mortgage providers.

The less pessimistic sentiment around now being a good time to buy was countered by a sharp drop amongst people expecting house prices to increase, down from 18% to a net 1%. This is consistent with slower housing turnover since the end of 2005, and a more moderate increase in the median sale price in recent times.

A number of the underlying driving forces point to the slower housing market continuing throughout 2006. The general economic slowdown both reduces household income growth and hence the capacity to take on increased debt, and reduces the willingness of people to spend.

There is also a large supply of new and existing housing in the pipeline that will impact house prices. In addition, it is well documented that a large percentage of mortgages come off their fixed rates in 2006, typically at significantly higher interest rates.

Another big change in findings from the previous quarter was interest rate expectations, down from 67% to a net 36%. Those surveyed appear to have quickly interpreted news of the wider economic slowdown, as well as a cooling in the housing market, as a reduced need for higher interest rates. This outlook was confirmed by the Reserve Bank last Thursday. Contrary to market pricing, the household sector on balance – and also the Reserve Bank – do not anticipate lower interest rates this year.

Previous housing cycles tell us that even while average price rises and falls are limited, the impact on individual properties can be significant. It is clear we have entered a period when house price gains are less likely, certainly not at the levels seen in recent years, and it could be several years before average prices gain a strong upward momentum again.

As always, people should be reviewing their personal circumstances, including debt levels and commitments when buying a house; something in particular this year that people should be careful with is the sequencing of selling and buying when they want to change homes.

The Results:

Graphs:

The net result is the difference between those who believe it’s a good time to buy and those who do not believe it’s a good time to buy.

The net result is the difference between those who believe prices will increase in the next 12 months and those who do not believe prices will increase in the next 12 months.

The net result is the difference between those who believe interest rates will increase in the next 12 months and those who do not believe interest rates will increase in the next 12 months.

ENDS

ASB Bank

Helping you get one step ahead.

In 1847, ASB opened as the Auckland Savings Bank with the pledge: 'to serve the community; to grow and to help Kiwis grow'. And that is very much what ASB is about today.

ASB is a leading provider of integrated financial services in New Zealand including retail, business and rural banking, funds management and insurance.

ASB strives to consistently provide its customers with outstanding service and innovative financial solutions. They're dedicated to providing simple financial products that allow their customers to bank with them how and when they want.

We all have our own ways to measure progress, and our own stories about the things that matter to us. Whatever way you choose to measure progress, and whatever your goals, ASB is there to help you get one step ahead.

FSCL: Woman Scammed Out Of $25,000 After Job Offer On LinkedIn

FSCL: Woman Scammed Out Of $25,000 After Job Offer On LinkedIn NIWA: Cheers To Crustaceans - New Species Named After Welly Brewery

NIWA: Cheers To Crustaceans - New Species Named After Welly Brewery MBIE: Trans-Tasman Earth Observation Research Studies Confirmed

MBIE: Trans-Tasman Earth Observation Research Studies Confirmed NZ Association of Scientists: Royal Society Te Apārangi Governance Submissions Close - NZAS Submission

NZ Association of Scientists: Royal Society Te Apārangi Governance Submissions Close - NZAS Submission HortPlus: Project Aims To Improve Quality Of Weather Data In New Zealand

HortPlus: Project Aims To Improve Quality Of Weather Data In New Zealand Air New Zealand: Air New Zealand And Cathay Pacific Welcome New Zealand Ministerial Approval To Extend Partnership

Air New Zealand: Air New Zealand And Cathay Pacific Welcome New Zealand Ministerial Approval To Extend Partnership